- Sellers soften offers to keep inventory moving

- Southern markets slow further on election activity

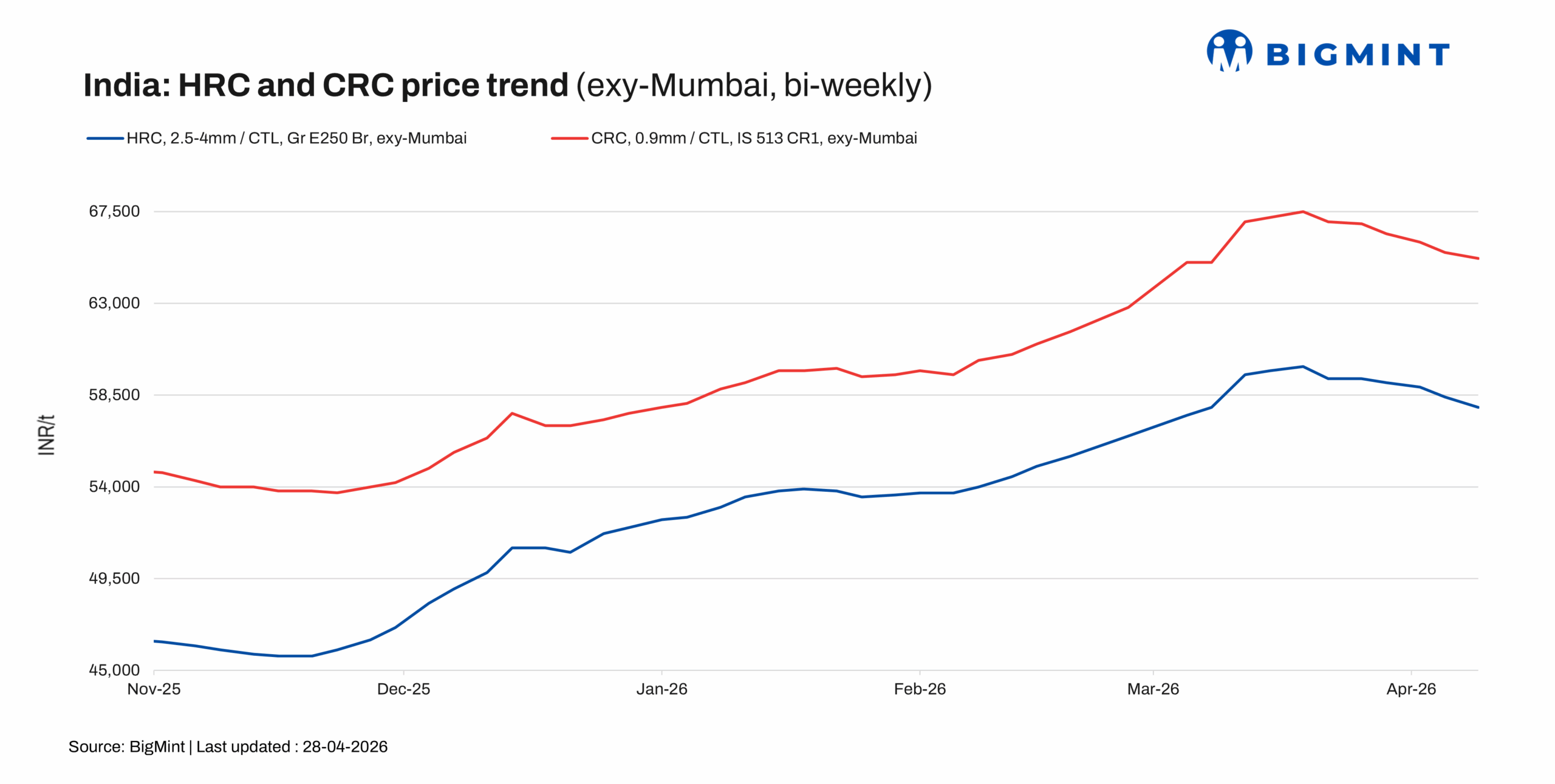

Trade-level prices of hot-rolled coils (HRC) across Indian markets fell w-o-w on 28 April 2026 to INR 57,300-59,500/t ($605-628/t), while cold-rolled coil (CRC) prices were assessed at INR 62,000-68,200/t ($655-720/t). Subdued demand and cautious market sentiment continued to weigh on prices.

BigMint’s bi-weekly benchmark assessment for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) declined by INR 1,000/t ($11/t), w-o-w to INR 57,900/t ($611/t) as of 28 April compared to INR 58,900/t ($622/t) on 21 April.

Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) prices were assessed at INR 65,200/t ($689/t) on 28 April, a w-o-w decrease of INR 800/t ($8/t) from INR 66,000/t ($697/t), a week ago. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market update

Market participants remained guarded this week. Buyers stayed firmly on the sidelines, while sellers had little choice but to soften their offers to keep material moving and avoid inventory pile-ups. A market participant informed BigMint, “Transaction activity stayed muted, with buyers showing no urgency to pick up volumes beyond what was immediately needed.” The mood across the supply chain was one of wait-and-watch, with neither side showing much appetite for fresh commitments.

Availability remained stable across most regions with no significant production or logistics disruptions, but that did little to lift activity. End-user demand stayed tepid, and the appetite for restocking remained limited.

The pressure was felt more acutely in certain pockets. In the north, a market participant informed BigMint that “sluggish inventory offtake and reduced mill lifting were a growing concern among market players.” In the south, a market participant stated, “Election-related activity has added to the slowdown.” This further weakened sentiment.

Additional updates

Import volumes: India’s bulk imports of HRCs touched 343,475 t as on 27 April. Around 103,840 t of additional cargoes are expected by mid-May.

Export volumes: India’s bulk exports of HRCs touched 122,721 t on 27 April. Around 8,800 t of additional cargoes are expected.

Outlook

In the near term, BigMint expects conditions to remain subdued. Buying is expected to remain cautious, with seasonal constraints and thin demand signals giving the market little reason to shift gears. Participants are broadly looking to May for stronger demand cues and clearer direction before committing to any fresh volumes.

Leave a Reply