- Muted construction demand weighs on steel consumption

- Market eyes May-June recovery for import activity

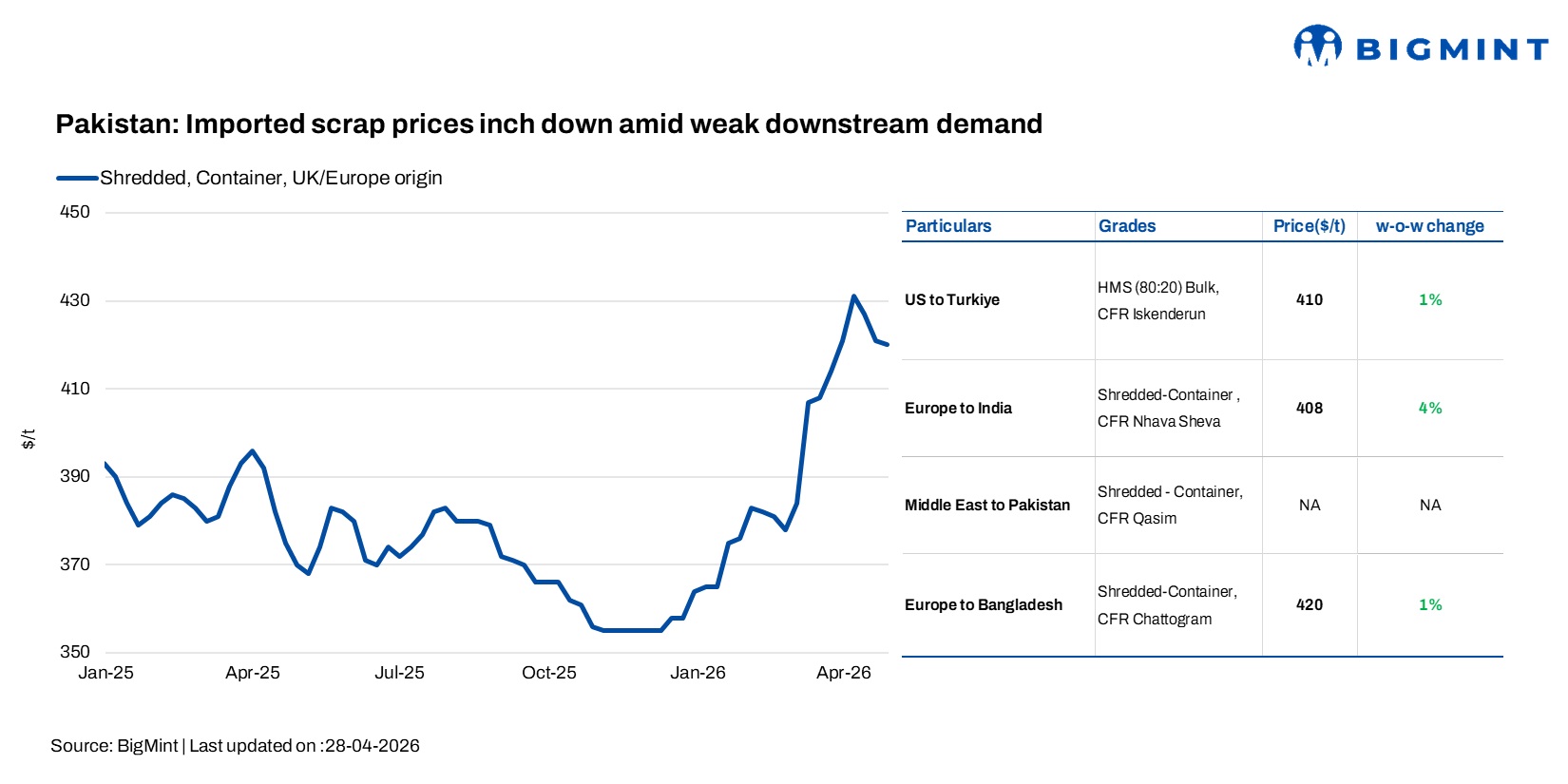

Pakistan’s imported ferrous scrap market remained largely steady, though sentiment stayed weak as mills continued to push back on higher offer levels. BigMint assessed Europe-origin shredded scrap at around $420/t CFR, down $1/t w-o-w, while bids were heard lower at $415-418/t CFR amid slow buying interest.

Weak demand keeps mills cautious

A Peshawar-based steel mill said, “Offers are now at $422-425/t, but we are quoting $415-418/t this week. Local sales are already low as customers are not active due to weak construction activity.” The mill added that domestic scrap procurement stands at PKR 154,000-155,000/t ($553-556/t), with some supply tightness, while capacity utilisation remains at 45-50%.

Two Malaysia-origin deals for 500 t busheling and 1,000 t shredded were heard at $435/t CFR Qasim.

A Karachi-based mill echoed similar concerns, noting, “Shredded offers are now at $418-420/t. The market may see some improvement in May-June as local scrap shortages might emerge.” The source added that developments around Hormuz have not impacted offers in the short term, as suppliers remain firm due to committed shipments and delivery timelines. Steel sales across major cities were reported at 40-50%, reflecting subdued downstream demand.

Finished steel prices remain under pressure

According to a steel trader, rebar prices were at PKR 255,000-260,000/t ($915-933/t), billets at PKR 215,000-220,000/t ($772-790/t), and bala at PKR 200,000-205,000/t ($718-736/t).

Local scrap prices were stable at PKR 155,000-158,000/t ($556-567/t). The trader noted that company sales and capacity utilisation levels remain around 40% with continued pressure on the demand side.

Outlook

BigMint believes that the market will remain under pressure in the coming week, with mills continuing cautious, need-based procurement amid weak downstream demand. A gradual improvement may be seen once high-priced inventories are cleared and construction activity gains some traction, potentially supporting better import activity around May-June. However, the State Bank of Pakistan’s recent policy rate hike to 11.5% is expected to keep liquidity tight, which could further delay a meaningful recovery in steel demand.

Leave a Reply