- China remains stable as global output edges higher

- Asia-led gains offset declines in Europe and North America

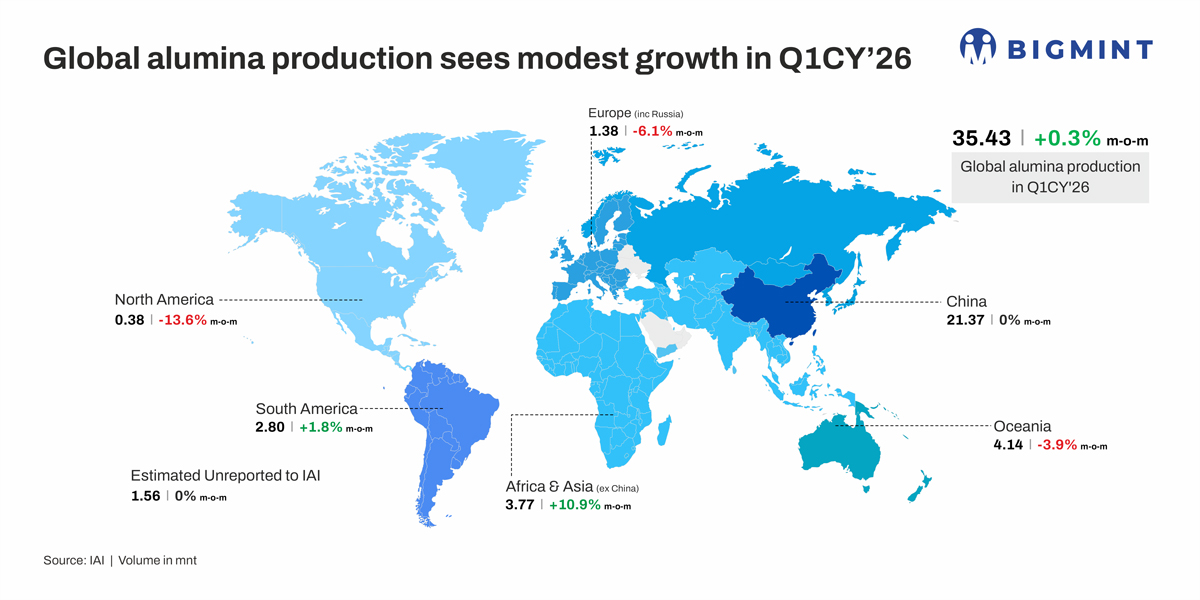

Global metallurgical alumina production stood at 35.43 mnt in Q1CY’26, marking a 0.3% y-o-y increase from 35.33 mnt in Q1CY’25, indicating a steady expansion in global output levels. The uptick was driven by additional supply from emerging producing regions, supported by new capacity commissioning and improved operating efficiencies at refineries. Healthy downstream aluminium demand, together with smoother supply chain conditions and broader geographic supply growth, contributed to a stable production environment during the quarter.

Regional drivers shaping global metallurgical alumina output

Global metallurgical alumina production in Q1CY’26 witnessed mixed regional trends, reflecting a combination of capacity expansions in emerging markets and production pressures across mature refining regions.

China, the world’s largest alumina producer, reported estimated output of 21.37 mnt, remaining flat on a y-o-y basis. Stable production was supported by high refinery utilisation rates, balanced domestic demand, and steady operating conditions across key producing provinces.

In Africa & Asia (excluding China), production rose sharply to 3.77 mnt, up 10.9% y-o-y from 3.40 mnt. The increase was driven by capacity additions in Indonesia, improved refinery operations in India, and rising output across the Middle East and Africa, supported by better feedstock availability and operating efficiencies.

South America recorded production of 2.80 mnt, increasing 1.8% y-o-y from 2.75 mnt. Growth was supported by stable refinery operations in Brazil, although gains remained moderate amid logistics constraints and cost pressures.

Conversely, Oceania witnessed production of 4.14 mnt, declining 3.9% y-o-y from 4.31 mnt. The fall was primarily attributed to maintenance shutdowns and operational disruptions at major Australian refineries.

Europe (including Russia) produced 1.38 mnt, down 6.1% y-o-y from 1.47 mnt, as elevated energy costs, softer industrial demand, and trade-related uncertainties continued to impact refinery operations.

North America recorded the sharpest decline, with production at 0.38 mnt, down 13.6% y-o-y from 0.44 mnt. The decrease reflected structural capacity limitations, lower refinery utilisation, and higher production costs.

Meanwhile, estimated unreported production to IAI remained stable at 1.56 mnt, unchanged on a y-o-y basis, indicating consistent output from non-reporting regions.

Overall, the global alumina market remained largely balanced during Q1CY’26, with production gains in emerging regions and steady Chinese output countering declines across higher-cost and operationally challenged markets, resulting in only a marginal increase in total output.

Factors influencing production trends

Production trends in Q1CY’26 were supported by ongoing capacity ramp-ups in emerging regions, particularly Southeast Asia and the Middle East, where newly commissioned refineries continued to raise output gradually. However, gains remained measured as several projects were still in early stabilization phases.

Raw material availability remained a key factor, with bauxite supply discipline, mining approvals, and feedstock logistics influencing refinery run rates, especially for import-dependent producers.

Geopolitical disruptions in the Gulf region also impacted sentiment, as vessel diversions through the Strait of Hormuz created uncertainty over alumina shipments to Middle East smelters and tightened regional spot availability.

Meanwhile, stable refinery utilisation across major producing regions and easing input cost pressures supported consistent operations. However, disruptions at established producers continued to cap gains, with Alcoa reporting Q1 CY’26 alumina output of 2.35 mnt, down 8% q-o-q, due to lower production at Kwinana, Australia, and constraints at San Ciprián, Spain.

Going forward, refinery expansions in Indonesia, downstream investments in the Middle East, and new projects in Africa and North America are expected to support medium-term supply growth, while near-term output gains are likely to remain gradual.

Outlook

Global metallurgical alumina production is expected to remain stable with modest growth in the near term, supported by ongoing capacity additions in emerging regions, steady downstream aluminium demand, and stable refinery utilisation across major producing markets. Output gains are likely to be led by Southeast Asia, the Middle East, and selected African regions as new projects continue ramping up gradually.

However, growth may remain measured due to bauxite supply constraints, mining approval delays, elevated operating costs in mature markets, and periodic maintenance disruptions. While steady production in China is expected to provide overall market balance, regional disparities and phased commissioning of new capacities are likely to keep global production growth gradual and uneven in the coming quarters.

Leave a Reply