- Indian mills slow production, schedule maintenance to curb met coal consumption

- Indonesian coke prices edge up on tight supply, Indian buyers show resistance

Asia’s metallurgical coal and coke markets entered a period of sideways trading in late April (week ending 27 April 2026), as cautious buying from major consumers — India and China — offset lingering supply-side disruptions stemming from the Middle East conflict.

While prices have found a degree of stability, underlying market dynamics remain tense. Elevated freight costs, concerns over diesel availability for Australian mining operations, and ongoing uncertainty about cargo deliveries are preventing any significant downward move — even as spot liquidity dries up.

Premium hard coking coal steadies

The premium hard coking coal segment showed little directional movement through the final week of April. After a modest decline mid-week, prices stabilised as market participants digested recent transactions and reassessed near-term demand prospects.

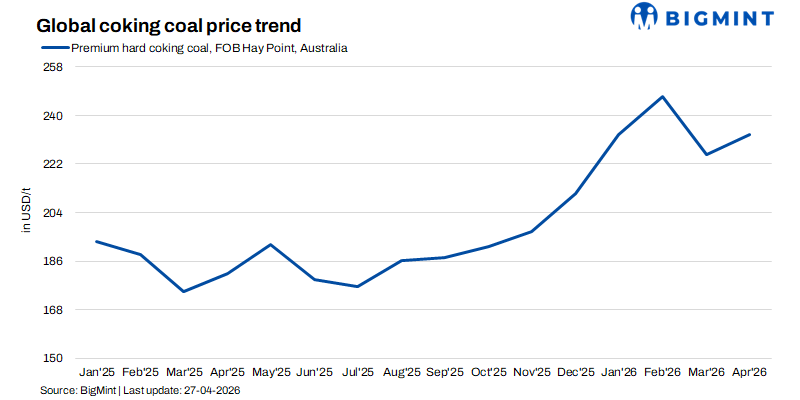

As of 24 April, premium low-volatility hard coking coal was assessed at $230.8/t FOB Australia, unchanged from the previous session and down just 50 cents over the week. On a CFR China basis, prices held at $218/t, flat both d-o-d and w-o-w.

Earlier in the week, a transaction for 30,000 t of Australian Peak Downs coal was heard concluded at $231/t FOB Australia with a May 21-30 loading window. The cargo was sold by a producer to an Asian trader.

Market response to the deal was mixed. Some participants viewed it as evidence that prices have found a floor, while others pointed to continued hesitancy among Indian buyers, who have been slowing production or scheduling maintenance to manage coking coal consumption.

Tradable levels for Australian Saraji and Peak Downs were broadly heard between $230-231/t FOB Australia, with buyers refusing to chase higher levels.

China enquiry remains selective

In China, seaborne premium coal activity remained slow, with steel mills largely covered through term contracts for both Australian and Canadian supplies. Fresh spot demand is expected to remain limited unless domestic coking coal futures show a sustained rally.

However, interest in low-volatility hard coking coal cargoes stayed active. Tradable levels for Australian Rangel grades were heard between $178-184/t FOB Australia, supported by steady enquiries from Chinese end-users.

By 24 April, low-volatility HCC FOB Australia was assessed at $180/t — up $2 from earlier in the week — while CFR China prices stood at $200/t, also $2 higher over the same period.

Met coke strengthens on tight Indonesian supply

The seaborne met coke market presented a notably stronger picture than raw coal, underpinned by tight supply from Indonesia and sustained demand in key markets.

Chinese 65/63 coke strength ratio (CSR) coke was assessed at $251/t FOB North China, up $2/t d-o-d and $2/t higher w-o-w. The price gap between Indonesian and Chinese coke has widened, creating opportunities for Chinese material in certain destination markets.

On a CFR India basis, as per BigMint’s assessment, Indonesian-origin 65/63 CSR met coke was assessed at $289/t, up by $1/t w-o-w. Indonesian FOB offers for 65/63 CSR remained unchanged d-o-d, reflecting a firm pricing environment. Suppliers maintained offers, capitalising on limited spot availability, while buyers in Vietnam and other Southeast Asian markets showed willingness to accept higher prices to secure tonnage.

However, buyer resistance is emerging at current levels. One trader source estimated that for Indian mills to actively consider importing Indonesian coke, prices would need to fall below $250/t FOB — a level that remains distant given present supply constraints.

PCI market range-bound, Russian material dominates

The pulverised coal injection (PCI) market remained subdued, with price movements contained as buyers and sellers assessed the outlook for steel margins.

Low-volatility PCI FOB Australia was assessed at $154.9/t as of 24 April, flat d-o-d, while CFR China prices stood at $138/t, up 30 cents from the previous session. Mid-volatility PCI similarly saw modest d-o-d gains of 30 cents on a CFR China basis.

A notable feature of the current market is the dominance of Russian PCI in China-bound trade flows, with reduced deliveries of Australian material opening space for Russian grades.

Freight and supply risks persist

The most direct impact of the Middle East conflict continues to be felt through freight markets. Panamax rates from Australia’s east coast to India averaged $25.18/t in March — a 50% increase from February and 73% higher y-o-y. Australia-China freights rose 46% m-o-m to $22.38/t in March.

Even with a fragile ceasefire in place, market participants see little near-term relief given significant damage to energy infrastructure in the region and persistent concerns about diesel availability for Australian mining operations.

Outlook

The immediate outlook for metallurgical coal suggests continued range-bound trading. Buyers in both India and China hold significant bargaining power, with Indian mills particularly cautious as domestic steel margins remain under pressure.

Yet the downside appears constrained. Freight costs, while showing modest declines, remain historically elevated. And concerns about supply chain reliability have not dissipated. For met coke, tight Indonesian supply suggests current prices have a firm footing, though further upside may be limited by buyer resistance.

Leave a Reply