- Buyers diversify sourcing amid Middle East supply disruptions

- Higher domestic pellet prices push steelmakers towards imports

Around 350,000 tonnes (t) of imported iron ore lumps have been booked over the past week, sourced from South Africa at around $118-120/t CFR, as per data maintained by BigMint. As per sources, the material, largely Fe 65% grade lumps (Al2O3<1%, SiO2- 6-6.5%)%, was imported from Kumba and Assmang mines located in South Africa. This marks the first imported cargo in Kandla since August 2025. One shipment has arrived, while another vessel is expected to dock in a couple of days.

While domestic supply continues to dominate procurement, the recent South African imports indicate a tactical shift towards higher-grade imports amid shifting supply dynamics. Sources indicated that due to elevated domestic lump prices and disruptions in pellet supply from the Middle East, steelmakers turned to procuring South African lumps, driven by their competitive pricing. A buyer stated that domestic ex-yard prices for this material hovered around INR 11,500-12,000/tonne (t) for local buyers at Kandla Port.

A steelmaker added that offers and sales were limited from Jindal Saw’s pellet plant in March, so raw material had to be sourced from alternative regions such as Karnataka pellets and NMDC/Lloyds Metals iron ore. However, with a subsequent increase in domestic offers, imported material has become more economical, particularly considering its higher grade.

Market scenario

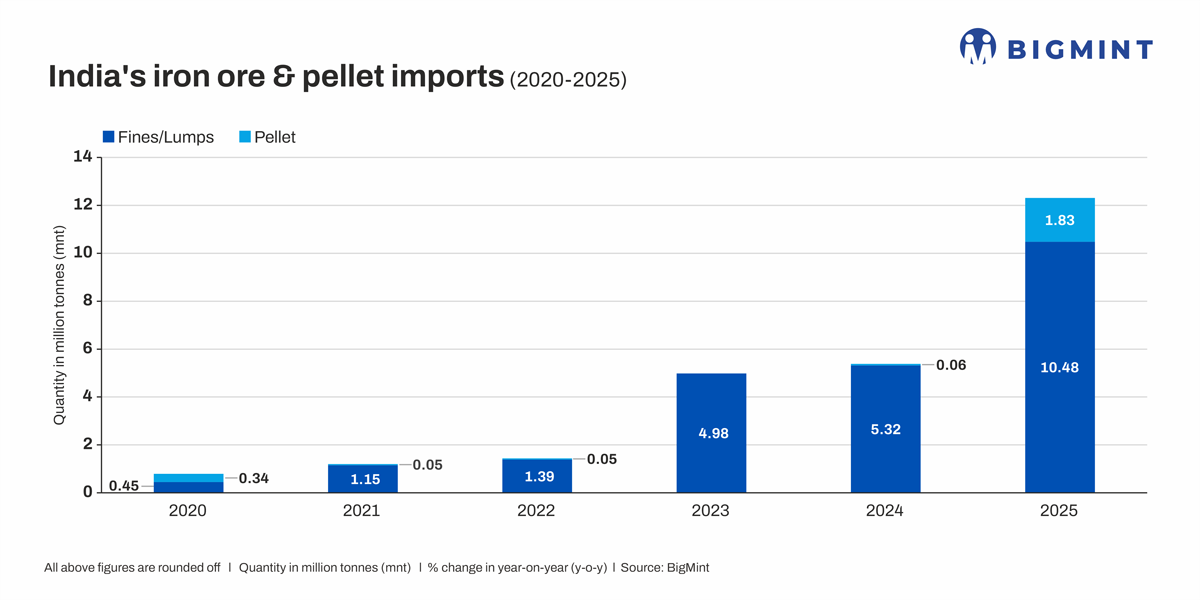

Geopolitical disruptions reshape supply flows: Supply from the Middle East has been impacted due to heightened US-Iran tensions and disruptions around the Strait of Hormuz, restricting cargo flows. This is reflected in recent trends, with India’s imports of pellets at nil in March 2026 due to supply disruptions. Previously, imports were at 1.85 mnt in FY’26 compared to 0.31 mnt in FY’25. At Kandla, imports stood at 0.99 mnt in FY26 against 0.31 mnt in the last financial year, indicating reduced Middle East inflows and prompting diversification towards origins such as South Africa.

Domestic prices elevated; imports offer grade advantage: Domestic pellet (Fe 62-63%) prices at Kandla were at around INR 12,200/t DAP, remaining on the higher side compared to portside prices of INR 11,500-12,000/t for imported material (Fe 65%). Thus, imported pellets were much more attractive in terms of cost and grade.

Previously, NMDC announced its list prices of iron ore CLO (calibrated lump ore) and fines on 5 April 2026, with prices of DR CLO (10-40 mm, Fe 67%) at INR 5,900/t ($63/t) and of iron ore fines (-10 mm, Fe 64%) at INR 4,500/t ($48/t). Prices are on FOR basis from the miner’s Bacheli complex and exclude royalty, DMF, and NMEDT. Prices of all grades were raised by INR 450-550/t. Lloyds Metals and Energy has raised its prices for iron ore fines, lumps, and pellets in Chandrapur by INR 400-500/t.

Rising sponge iron capacity supports import demand: Sponge iron capacity in Gujarat has expanded to around 9.94 mnt in FY’26 compared to 9.7 mnt in FY’25. Meanwhile, Gujarat’s crude steel capacity recorded at 15.6 mnt in FY’26 (15 mnt in FY’25) while production increased to 12 mnt in FY’26 compared to 11 mnt in FY’25, which significantly increased the requirement for consistent and higher-grade raw material.

Lack of domestic pellet tenders: Kandla-based buyers stated that the lack of bulk pellet tenders in the domestic market pushed plants to secure imported material. Odisha and Karnataka-based pellet material is not viable for buyers due to higher prices.

Outlook

Imports are likely to strengthen in the near term, supported by constrained domestic supply and disruptions in Middle Eastern pellet flows. Sustained demand for high-grade material will keep import interest firm, although procurement will remain sensitive to pricing and freight dynamics.

Leave a Reply