- Pacific stays firm with strong demand and limited vessel supply

- Atlantic stays weak with more vessels and low cargo demand

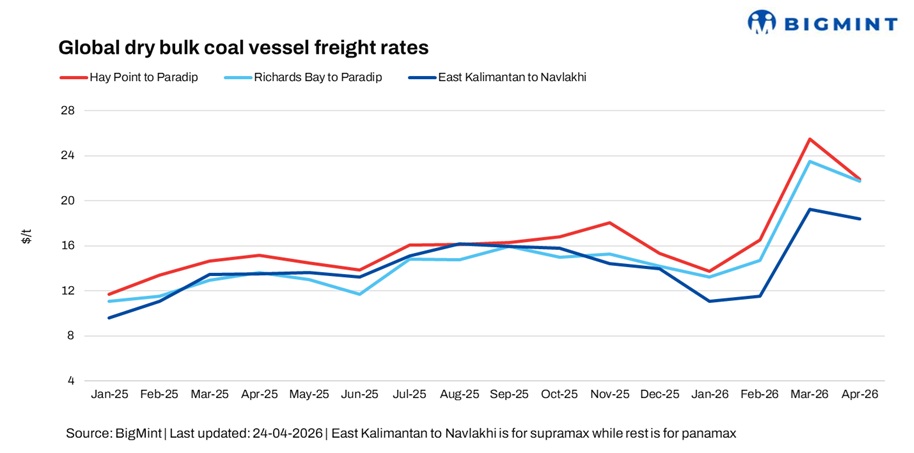

Dry bulk coal freight to India reflected a mixed trend in the week ended 24 April, with firm Supramax activity in the Pacific supporting overall sentiment, even as Panamax routes faced pressure amid softer enquiry and steady vessel availability.

Market sentiment remained uneven, with fixing activity limited across certain regions. A shipbroker source said, “market is slightly negative, fixtures are very few,” highlighting the cautious tone in parts of the market.

In the Pacific, Supramax outperformed, supported by firm regional coal demand and tighter prompt supply, with India-bound cargoes anchoring sentiment, while brokers noted that the “Asia market is booming,” reflecting sustained regional momentum. Panamax activity, however, showed signs of softening. Softer Pacific cues and steady tonnage capped fresh fixing appetite, with uneven China coal enquiry limiting upside across key routes.

In contrast, the Atlantic basin remained subdued, with higher vessel availability and weak fronthaul demand keeping activity slow and enquiry limited. A lengthening tonnage list further weighed on sentiment, restricting fresh fixtures.

Segment-wise, Supramax maintained its strength, while Panamax showed early signs of easing and Capesize edged lower. A broker commented, “Cape is a bit down, Panamax is largely steady but easing, while Supra is still going strong, with the difference between Supra and Ultra widening. Handy is also looking better.”

Route-wise updates

Market highlights

- Bunker prices firm w-o-w: Bunker prices increased by $24/t week-on-week to $763/t as of 24 April, from $739/t a week earlier, tracking firmer crude trends and steady demand across key bunkering hubs.

- Baltic index gains w-o-w: The Baltic Index climbed by 150 points week-on-week to 2,673 as of 23 April, supported by gains in the Supramax segment, up 124 points to 1,522, while the Panamax segment edged lower by 5 points to 1,965, indicating mixed momentum across vessel classes.

- DCE coke futures edge higher w-o-w: Coke futures on the Dalian Commodity Exchange gained RMB 55/t ($8.06/t) week-on-week to RMB 1,833/t ($268.51/t) on 24 April, supported by stable buying interest and steady steel sector sentiment.

- Brent crude futures rally w-o-w: Brent crude oil (June 2026 contract) was last assessed at $104.53/bbl on 24 April, up by $8.37/bbl from $96.16/bbl a week earlier, supported by stronger macroeconomic cues and supply-side developments.

Outlook

Coal freight to India is expected to remain mixed in the near term, with Supramax likely to stay supported by firm regional demand and tighter vessel availability in the Pacific. However, ample tonnage in the Atlantic and easing trends in the Panamax segment may continue to weigh on overall sentiment. Rising bunker prices and firm crude trends could add cost-side support, while uneven enquiry across regions is likely to keep fixing activity selective.

Leave a Reply