- Reduced Xinjiang acreage and policy shifts tighten future supply outlook

- Stable consumption and import recovery keep global trade flows active

China’s cotton balance sheet for MY 2026/27 points to a modest tightening in supply, driven primarily by policy-led acreage reductions in Xinjiang, even as demand from the textile sector remains relatively stable. Production is forecast at 7.2 million tonnes, down 4.5% year-on-year, reflecting structural adjustments aimed at removing low-yield and water-stressed areas from cultivation.

For Indian traders and spinning millers, this signals a gradual shift rather than a sharp disruption, with China maintaining its position as a large but controlled buyer in the global cotton market.

Production shifts reshape supply dynamics

The decline in output is largely policy-driven rather than price-led. Xinjiang, which accounts for over 92% of China’s cotton production, continues to benefit from strong mechanisation and subsidies, but authorities are actively rationalising acreage to improve efficiency and sustainability.

Yields are expected to remain firm at around 2,424 kg/ha, supported by better farm practices and removal of marginal land. This limits the downside in production despite lower area. For Indian exporters, this implies China’s supply contraction will be gradual, reducing the likelihood of sudden import spikes.

Consumption steady but structurally constrained

Cotton consumption is projected at 8.4 million tonnes, supported by policy stimulus and gradual recovery in textile exports. However, structural challenges persist. Weak domestic demand, pressure on apparel exports, and rising substitution by polyester and viscose continue to cap growth.

China’s spinning sector, operating with excess capacity, is increasingly cost-sensitive. The widening price gap between cotton and synthetic fibres is pushing spinning millers to reduce cotton usage in blends, a trend closely watched by Indian yarn exporters.

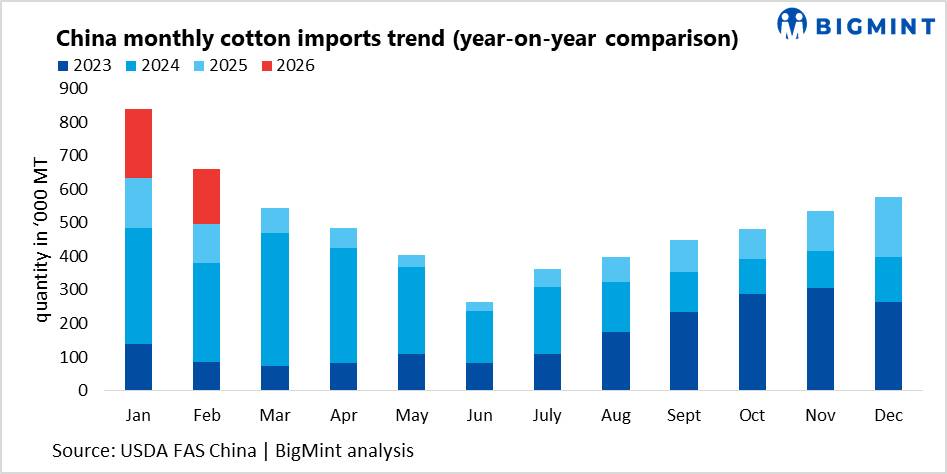

Trade flows and import outlook

Imports are expected to rise slightly to 1.5 million tonnes, supported by quota releases and favourable international price spreads. However, sourcing patterns remain shifted away from the U.S. due to tariffs, with Brazil and Australia dominating supply.

For India, this creates a mixed opportunity. While China’s import demand remains steady, competition from competitively priced Brazilian cotton and quality parity with Australian fibre limits India’s share unless pricing aligns.

Outlook for Indian market participants

China’s cotton policy direction suggests a controlled tightening of domestic supply alongside stable but efficiency-driven demand. For Indian traders, this means export opportunities will remain opportunistic rather than structural. Spinning millers should track China’s fibre substitution trends closely, as they influence global yarn demand and pricing benchmarks.

In the near term, China is unlikely to trigger a strong bullish cycle in global cotton, but its steady import requirement will continue to anchor trade flows and provide underlying support to international prices.

Leave a Reply