- China’s coal restocking begins and Asia is feeling the pull

- Tight Indonesian supply is reinforcing the price uptrend

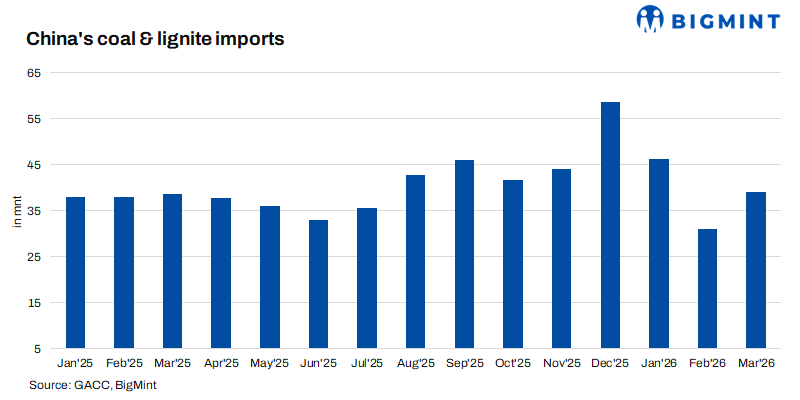

After a sluggish start to the year, China’s coal import market has come back to life. The catalyst is not just market forces – it is a direct government mandate. Chinese authorities have instructed power plants to raise their coal inventories from about 17 days to 20 days of consumption. That policy is now rippling across Asia, tightening supply and pushing prices higher.

At the same time, Indonesian production remains constrained, freight rates are volatile, and other Asian buyers – South Korea, Vietnam, and even pockets of India – are adding to demand. The result is a market that has turned firmly bullish in a matter of days.

The Chinese restocking: Policy-driven and real

The government’s 20-day inventory target is not a suggestion. It is an instruction. And Chinese power plants are scrambling to comply.

Rising temperatures in South China are also playing a role. Utilities are becoming more willing to accept higher offer prices because they know summer demand is coming. The March power data provides the context: thermal generation rose 4.2% year-on-year, while wind fell 17.3%. Coal’s share of China’s power mix jumped to 66% – its highest level in months.

The restocking is already visible in tender activity. Guangdong Yuedian Group, one of China’s largest utilities, received import offers for 3,800 kcal/kg coal for May-June delivery at CFR 554-572 yuan per tonne ($71.57-73.90). Datang Group received offers for 4,600 kcal/kg at CFR 700 yuan ($90.30) and 5,500 kcal/kg at CFR 888 yuan ($114.55).

But the most active demand is for ultra-low-CV coal 3,200-3,400 kcal/kg from Indonesia. Traders report that NAR3,200 is trading at index plus $6=6.5 per tonne for May-loading Panamax cargoes. This grade is being used for blending with domestic coal, and the economics work despite high freight rates.

Indonesian supply: Tight and Getting Tighter

Just as Chinese demand is rising, Indonesian supply is struggling to keep pace.

The root cause is RKAB – the annual coal production approval system. Many Indonesian miners have not yet received their approvals for 2026, leaving them unable to commit to spot cargoes. Those who have approvals are increasingly selling into the domestic market, where smelter demand is strong and pricing is profitable.

The numbers tell the story. Indonesian daily thermal coal exports averaged just 970,000 tonnes over the past five days – down 5.5% w-o-w and well below the 2025 average of 1.31 million tonnes.

The tightness is most acute in Sumatra, where supply of 3,400 GAR coal is particularly constrained. Traders note that there is now roughly a $20 per tonne gap between 3,400 GAR and 4,200 GAR, leaving room for lower grades to rise further.

APBI-ICMA, Indonesia’s coal mining association, has confirmed that the government has approved about 580 million tonnes of production for the first half of 2026, with more approvals expected in the second half. But for now, the market is tight.

And Chinese buyers are competing for a shrinking pool of available cargoes.

Broader Asian demand: Not just China

China is the main driver, but it is not alone.

South Korea continues to show steady interest in Indonesian mid-CV coal. Importers are using Indonesian coal to manage ash content when blending with higher-CV cargoes from Australia and Russia. March imports rose 36.5% year-on-year, and Q1 imports were up 19%.

Vietnam is also in the market for mid-CV grades. While not a giant buyer, Vietnamese demand is consistent and helps absorb supply that might otherwise pressure prices.

India is the wildcard. So far, Indian buyers have been selective, mostly purchasing Russian and South African cargoes rather than Indonesian. A major power plant recently booked Russian cargoes, and an industrial house has been consistently enquiring. But full-scale summer restocking has not yet begun. When it does – and with El Niño threatening hydro output, it almost certainly will – Indian demand could add another layer of tightness.

Freight: A persistent headwind

One factor complicating the market is freight. Rates from Australia to China have been volatile, with Panamax vessels at $19.4-21 per tonne and Capesize at $16.3-20. The wide ranges reflect uncertainty among shipowners and charterers about where prices are headed.

Higher freight costs eat into delivered economics. For Chinese buyers, every dollar increase in freight makes domestic coal more attractive relative to imports. But with domestic prices also firm, the arbitrage remains workable – especially for lower grades.

The price picture

Prices have responded across the board. Platts assessed FOB Kalimantan 4,200 GAR at $60.7 per tonne on April 22, up 15 cents. FOB Kalimantan 5,000 GAR rose 35 cents to $78.00. CFR China 5,500 NAR gained 40 cents to $109.00.

Northern Chinese port prices are stable but firm. The 5,500 kcal/kg benchmark is at 770-775 yuan per tonne, while 5,000 kcal/kg is at 688-700 yuan. These are not dramatic moves, but they are holding – which, in a volatile market, is a sign of underlying strength.

The outlook

The restocking is expected to continue through April and into May. Chinese power plants are preparing for summer demand, and with wind underperforming, coal is the reliable backstop.

Indonesian supply may loosen in the second half of the year as more RKAB approvals come through. But for now, the market is tight. And if Indian demand arrives earlier than expected, prices could move higher still.

One risk to watch: if Chinese utilities complete their restocking quickly – reaching the 20-day target ahead of schedule – the urgency could fade. But with summer still ahead and inventories still below target, that risk feels distant.

For now, Asia’s thermal coal market is being pulled by a powerful force: China’s policy-driven restocking. And with Indonesian supply constrained, every tonne China buys is a tonne that someone else does not get.

Leave a Reply