- Scrap prices rise on improved demand, tight supply

- Weak rebar demand limits aggressive mill buying

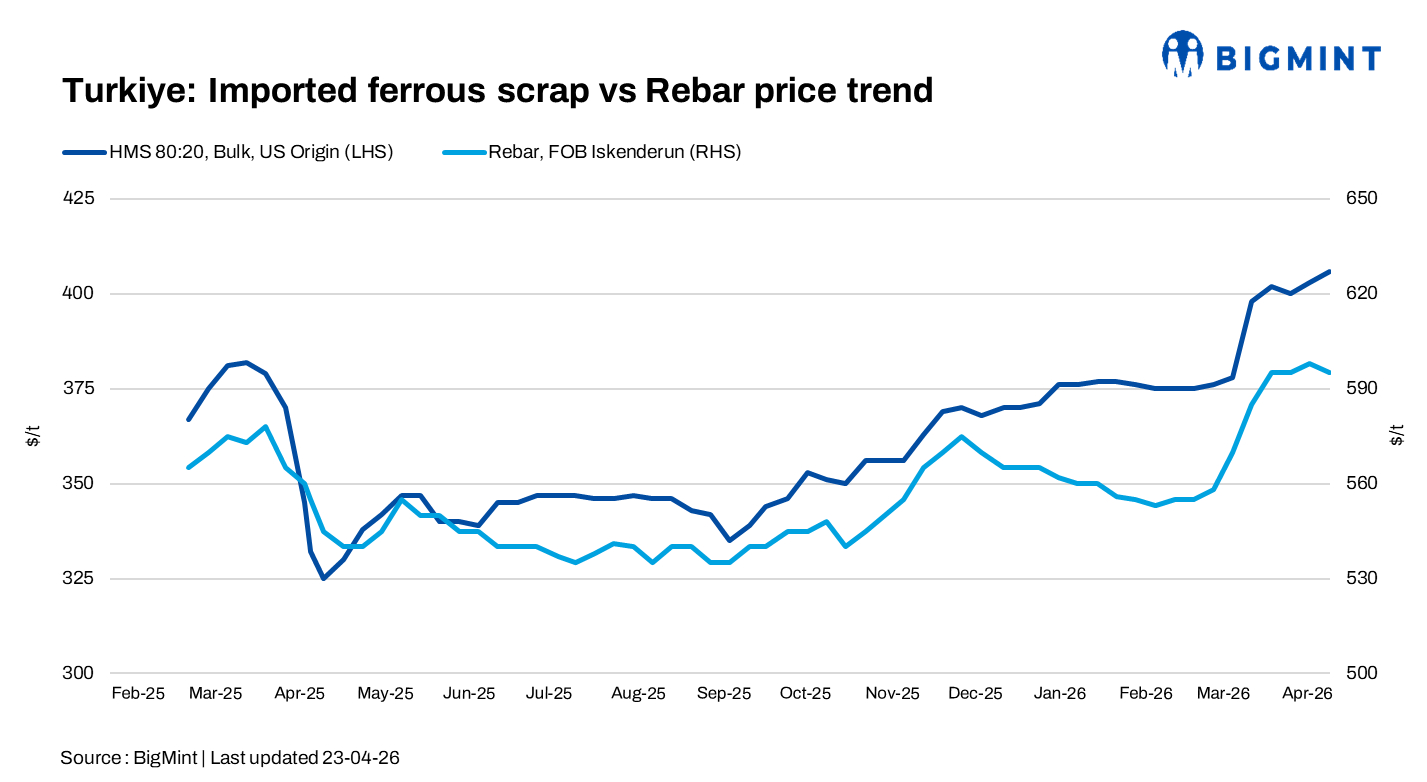

Turkish deep-sea scrap prices showed slight strength during the week ending on 23 April, supported by a slight improvement in finished long steel demand and relatively lower raw material inventories at mills. While the overall market remained quiet, this marginal pickup in demand encouraged mills to re-enter the market, leading to a few deals at slightly higher levels.

Price assessments

- US-origin bulk HMS 80:20: $406/t CFR Turkiye, up by $3/t w-o-w

- US East Coast HMS 80:20: $377/t FOB, up $3/t w-o-w

The scrap-to-rebar spread widened to around $188-190/t, with rebar export offers at $595-600/t FOB. Meanwhile, 8 to 9 deals were concluded from Europe at around $397-404/t CFR.

Market comments

The price increase was mainly driven by a gradual pickup in finished steel demand, along with declining inventories at trader levels, which supported restocking activity. At the same time, firm freight rates and limited availability of scrap continued to strengthen seller positions.

A Baltic-origin supplier indicated that available cargoes have been largely cleared, with no fresh offers currently in the market. The supplier noted that any new sales are likely to be targeted at $400/t and above.

On the buy-side, Turkish mills are yet to fully cover their May shipment requirements, with market participants expecting increased deal activity toward the end of the month.

A Turkish market participant commented, “Market activity remained limited, with both buyers and sellers waiting for clearer price direction, as uncertainty over workable levels persisted, with sellers continuing to target around $408-410/t CFR.”

In the downstream market, despite the firming scrap prices, downstream conditions remained weak. Export rebar activity stayed subdued, with prices observed around $595/t FOB, limiting mills’ ability to absorb higher raw material costs. This continued to create resistance among mills toward further price increases.

A trader noted that “finished long steel demand saw a slight improvement during the week, supported by declining trader inventories” and added that mills may attempt to raise finished steel prices in response.

Outlook

BigMint understands from market participants that imported scrap prices are expected to remain firm in the coming days, with a modest upside of around $5/t as mills continue to secure bookings for May shipments. However, subdued downstream demand, ongoing geopolitical uncertainty, and cautious buying behaviour are likely to keep the market largely range-bound, with price movements expected to be gradual rather than sharp.

Leave a Reply