- Market to see more deals ahead of Labour Day

- Rising supply post lifting of BHP ban may weigh on prices

India’s iron ore fines export market witnessed firm activity during the week ended 23 April, supported by active restocking demand from Chinese buyers, although prices softened marginally towards the end of the assessment period amid rising supply.

Prices, deals

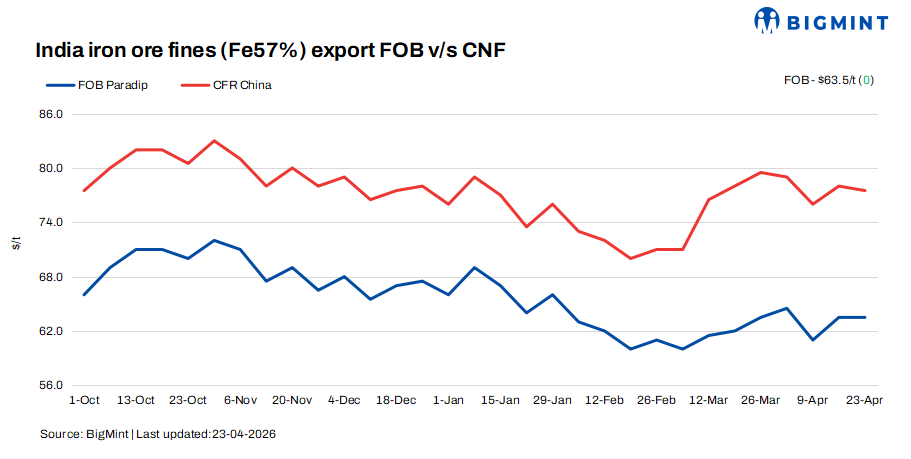

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index remained stable w-o-w at $63.5/t FOB east coast on Thursday, 23 April 2026. Meanwhile, CFR China prices for Indian-origin iron ore softened w-o-w to $77.5/t, with vessel freight rates remaining largely stable.

Deal activity remained healthy, with transactions for around 280,000 tonnes (t) recorded from east coast-based exporters during the assessment window. Most deals were concluded for Fe 55-57% fines, while demand for lower-grade Fe 54-55% cargoes remained weak, with offers receiving limited acceptance.

Separately, deals for around 240,000 t were concluded by Karnataka-based players, reflecting active participation beyond the east coast market.

BigMint recorded transactions for a total of around 520,000 t.

According to sources, Fe 57% fines were transacted at firm discounts of around 19-20% to the global fines index. In contrast, lower-grade Fe 54-55% fines saw thinner participation, with discounts largely in the range of 22-23%, with indications that miners may need to widen discounts further to 23-24% to clear volumes.

However, exporters continued to quote similar levels, with a few more deals expected to be concluded ahead of the Labour Day holidays.

Market scenario

Market activity in the iron ore export segment remained robust, supported by active restocking demand from Chinese mills. Buying interest stayed firm through the week, with multiple deals concluded, reflecting improved liquidity and stronger near-term demand fundamentals. However, the market softened slightly today. An international trader noted that, “Supply has increased following the lifting of restrictions on BHP cargoes, which is set to weigh on prices in the near term.”

Other international traders echoed these sentiments, highlighting that while deal flow remained healthy due to restocking requirements, rising availability has started to weigh on sentiment at the margins. Participants expect a few more deals to be concluded ahead of the Labour Day holidays, after which market activity is likely to turn subdued.

Sources further indicated that monthly offtake volumes have trended higher, supported by multiple deals concluded earlier in the month, reflecting sustained demand in the seaborne market despite intermittent price corrections.

Domestic prices exceeded export realisations by around INR 250/t ($3/t), with the gap shrinking by INR 50/t ($0.5/t) w-o-w. Iron ore fines (Fe 57%) prices in Odisha were recorded at INR 3,750/t ($40/t) ex-mines, down by INR 100/t ($1/t) w-o-w on 23 April. Meanwhile, the ex-mines realisation in exports from the Barbil region was recorded at INR 3,500/t ($37/t).

Chinese iron ore fines prices rise w-o-w: The benchmark iron ore fines Fe 61% index rose w-o-w by $2/dmt to $108/dmt CFR China on 22 April. Prices rose as eased import curbs on Australian ore lifted inquiries, while buyers increasingly avoided high-phosphorus fines. Import margins narrowed as discounts adjusted, though some advantage persisted. The market was supported by improved ferrous sentiment and pre-holiday restocking ahead of Labour Day, though tight mill margins continued to cap demand for higher-grade products.

DCE iron ore futures rise: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2026 contract closed higher at RMB 785/t ($115/t) against RMB 775.5/t ($112/t) on 23 April, increasing by RMB 10/t ($1.5/t) w-o-w.

Rationale

- Three deals for Fe 57% were recorded, out of which two were taken during this publishing window. Therefore, T1 trade was given 50% weightage in the index calculation. For the detailed methodology, click here.

- BigMint received fifteen (15) indicative prices in the current publishing window, and eleven (11) were considered for price calculation as T2 inputs and given the rest 50% weightage.

Outlook

Iron ore export prices are expected to remain rangebound. A few more deals are expected to close ahead of the Labour Day holidays, keeping the market active next week.

Leave a Reply