- Imported zinc prices remain elevated, limiting arbitrage opportunities

- Sellers struggle to offload material amid weak galvanising activity

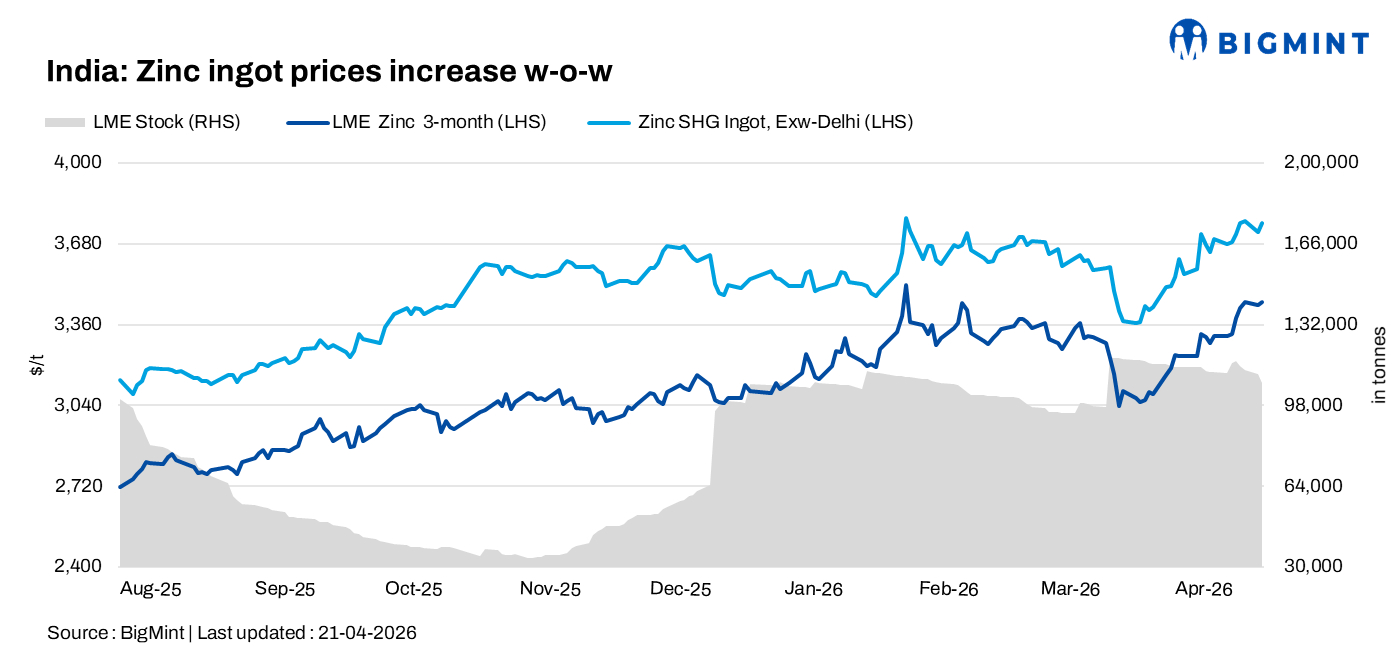

India’s zinc ingot (99.995%) prices increased by INR 7,000/t w-o-w to INR 350,000/t ex-Delhi on 21 April, compared with INR 343,000/t a week earlier, supported by producer price hikes and marginally firmer global cues.

The increase was largely driven by a price revision by Hindustan Zinc Limited (HZL), which raised offers by INR 15,900/t to INR 358,600/t ex-Chanderiya on 20 April, compared with INR 342,700/t on 13 April.

On the global front, London Metal Exchange (LME) three-month zinc futures showed an upward trend during the week, closing at $3,448/t on 21 April versus $3,324/t on 14 April. Meanwhile, LME stocks declined to 107,525 t from 115,925 t over the same period, indicating tightening exchange inventories and lending support to prices.

Trading activity slows amid price rise

Market activity remained subdued, with buyers largely restricting purchases to immediate requirements amid weak downstream demand, particularly from the galvanising segment.

Some market participants highlighted that galvanising activity has slowed, impacting overall zinc consumption. Sellers were reportedly facing difficulty in offloading material, while premiums remained under pressure. Additionally, MCX prices were heard trading at a discount to import parity, further dampening buying interest.

In the spot market, imported South Korea-origin SHG zinc (99.995%) was quoted at $3,700-3,710/t CFR Nhava Sheva, while Australian-origin material was heard at around INR 367,000-368,000/t ex-Delhi.

PMI deals were reported at around INR 313,000/t, reflecting continued price sensitivity and selective buying among consumers.

Downstream alloy prices tracked the broader uptrend in zinc. Zamak 3 prices were heard to be at around INR 364,000-365,000/t, while Zamak 5 stood at INR 371,000-372,000/t ex-works.

Coated steel prices show mixed trend

Meanwhile, India’s coated flat steel prices showed a mixed trend during the week, reflecting cautious market sentiment and uneven demand.

Galvanised plain (GP) coil prices edged down by INR 100/t w-o-w to INR 80,900/t ex-Mumbai, while pre-painted galvanised iron (PPGI) remained stable at INR 88,400/t. Galvalume prices declined by INR 800/t to INR 90,200/t. The trend was influenced by subdued demand conditions, selective buying, and adequate supply availability in certain segments. Mills largely maintained pricing discipline despite softer sentiment, while tradable ranges indicated cautious procurement strategies among buyers.

Export offers for hot-dip galvanised iron (HDGI) remained stable at around $770/t, reflecting a firm mill stance amid limited buying interest. Overall, demand remained need-based, with regional disparities continuing to weigh on market activity.

Outlook

Zinc prices are expected to remain supported in the near term, tracking firm LME trends and HZL’s price hikes, although subdued downstream demand and weak physical market sentiment may limit sharp upside.

Meanwhile, coated steel prices are likely to remain largely stable, with cautious demand and adequate supply conditions continuing to influence market direction.

Leave a Reply