- Q1 output remains weak due to mine preparation, overburden removal

- HVO’s output up amid limited weather disruptions, higher fleet utilisation

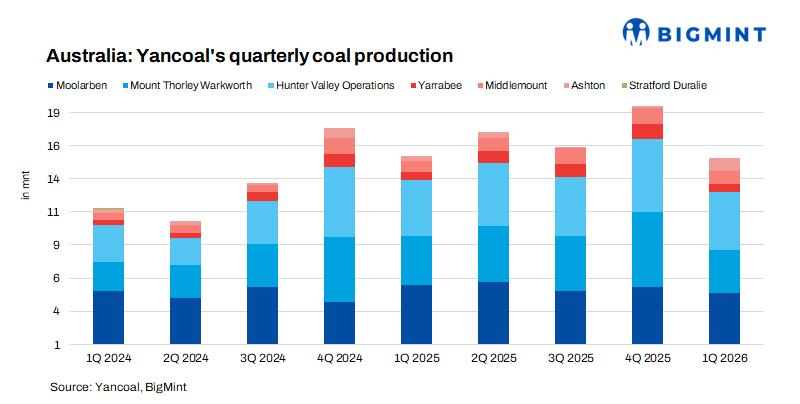

Yancoal reported a stable operational performance in the January-March quarter of CY’26, though with slightly lower coal production and sales y-o-y. Run-of-mine (ROM) coal production stood at 15 million tonnes (mnt), while saleable coal production reached 11.9 mnt and coal sales volume totalled 8.2 mnt.

The decline in production, including a 1% y-o-y drop in ROM coal and a 5% fall in saleable output, was largely anticipated. The first quarter typically reflects lower output due to mine preparation and overburden removal activities.

Operational performance by assets

Moolarben resumed underground operations in March following a longwall move, with most quarterly output driven by open-cut mining and stockpile drawdown. Performance improved significantly in March due to favourable weather and strong productivity.

Mount Thorley Warkworth (MTW) operated in line with plans and slightly exceeded targets in March, supported by early coal extraction, with a continued focus on maintaining equipment reliability.

Hunter Valley Operations (HVO) delivered a slightly stronger performance y-o-y, exceeding both ROM and saleable coal targets, driven by minimal weather disruptions and improved fleet utilisation.

Yarrabee recovered quickly from cyclone impacts and returned to planned levels, although unplanned coal handling and processing plant (CHPP) maintenance and lower yields in March affected saleable output; improvements are expected in the following period.

Middlemount also faced cyclone-related disruptions but maintained ROM production above budget despite challenges such as diesel delays, water management issues, and adjustments to meet specific coal quality requirements.

Ashton’s longwall operations continued steadily throughout the quarter, supported by supplementary lower-quality coal from development mining, with careful management of geotechnical and water conditions ensuring smooth progress without major interruptions.

Demand and supply dynamics

Demand remained mixed across regions. Major importers such as China and India reduced coal imports due to high domestic production and elevated stockpiles, while demand improved in countries such as Japan and South Korea.

Supply dynamics were also uneven, with Indonesian exports declining amid policy uncertainties, while Russian and US exports increased. In metallurgical coal markets, conditions shifted towards cost-based pricing, suggesting that rising input costs, particularly diesel, may be passed through to customers.

Project developments and exploration update

MTW’s underground mine pre-feasibility studies are ongoing, with a feasibility study expected to begin in the first half of CY’26. If approved, the project could extend the mine’s production life without increasing annual output.

At HVO, a revised mine plan for a life extension within existing leases was submitted to the NSW Department of Planning, Housing, and Infrastructure (DPHI) in August 2025 and is under review by NSW and Federal authorities. A decision is expected before the temporary extension expires in December 2026, with operations currently unaffected.

At Moolarben, the OC3 Extension Project was amended and resubmitted on 10 April 2026. If approved, it would add 30 mnt to life-of-mine ROM production without changing annual output. A decision could be received in the second quarter of CY’26.

The Stratford Renewable Energy Project remains under commercial and regulatory evaluation.

Yancoal spent $1.45 million on exploration at HVO and Moolarben, drilling 14 boreholes (2,397 metres) to assess structure, coal quality, and samples.

Yancoal advanced its strategic position with the announcement of acquiring an 80% stake in the Kestrel Coal Mine for $1.85 billion. This move is set to enhance the company’s portfolio by adding a high-margin, long-life metallurgical coal asset while increasing its exposure to premium coal segments.

Outlook

Production is expected to improve in the coming quarters as operations normalise following planned activities and fewer weather disruptions. Demand trends may remain mixed, with subdued imports from China and India but steady requirements from Japan and South Korea.

Yancoal’s planned acquisition of an 80% stake in the Kestrel Coal Mine is set to strengthen its portfolio with premium met coal exposure and support long-term growth. However, rising input costs, particularly diesel, may continue to pose margin pressures.

Leave a Reply