- Dhamra, Gangavaram record sharp rise in arrivals

- Over 2.5 mnt of US coal currently en route to India

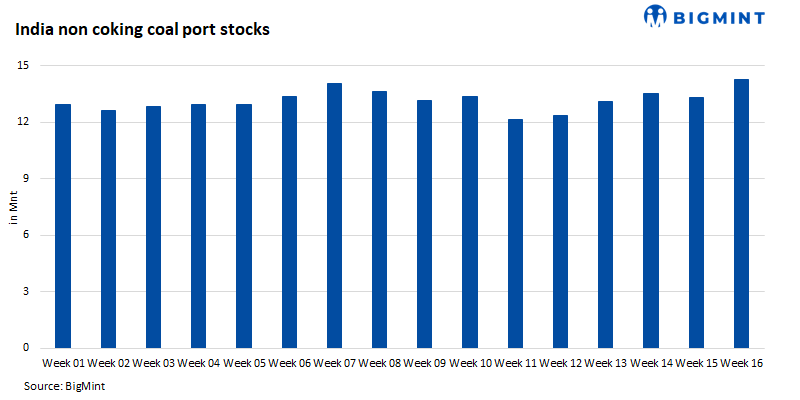

India’s non-coking coal inventories at major ports surged during Week 16 (12-18 April 2026), reflecting improved arrivals and inventory accumulation by traders and industrial consumers. Total non-coking coal stocks stood at approximately 14.3 million tonnes (mnt), marking a 7.24% increase from 13.3 mnt in Week 15.

The rise in stocks was largely driven by higher inflows at key ports such as Dhamra, Gangavaram, and Tuna, along with increased stocking by major industrial consumers, including cement, steel, and trading companies.

Port-wise trends driving w-o-w increase

Several key ports recorded substantial increases in non-coking coal inventories in Week 16:

- Dhamra Port saw one of the most significant rises, with stocks increasing 44.2% w-o-w to about 1.27 mnt, largely due to fresh arrivals for trading houses and industrial consumers.

- Gangavaram Port recorded a sharp 110.48% increase to 442,000 t, reflecting bulk shipments received by trading companies and cement manufacturers.

- Tuna Port posted a 139.43% jump to 381,170 t, driven by increased cargo positioning by traders and cement sector buyers.

Across other ports, trends were mixed, indicating a dynamic flow of cargo depending on regional demand patterns and logistical movements.

In terms of corporate holdings, trading firms such as Adani Enterprises and Agarwal Coal, along with industrial consumers including Tata Steel, UltraTech Cement, and JSW Steel, were among the key stockholders. The presence of large trading inventories indicates continued distribution of imported coal to inland industrial consumers.

Market scenario

A number of shipments arrived during the week, particularly at east coast ports such as Dhamra and Gangavaram. This led to a temporary build-up of inventories before dispatch to end users.

Seaborne South African non-coking coal offers remained weak, with FOB at $92-94/t and CFR India at $112-113/t, while freights stayed firm. Buying remained cautious amid weak demand, bid-offer gaps, and increasing preference for domestic coal.

Additionally, over 2.5 mnt of US coal is currently en route to India across more than two dozen vessels, with arrivals scheduled between April and May 2026. This reflects a deliberate build-up of coal inventories by cement manufacturers and industrial buyers.

Market implications

The rise in non-coking coal stocks suggests adequate supply availability in the near term, which could moderate short-term import demand if dispatch rates remain steady. Higher inventories at ports also indicate that traders and industrial consumers are maintaining buffer stocks to manage supply chain uncertainties and seasonal demand fluctuations.

Leave a Reply