- Billet, sponge iron prices decline w-o-w on subdued demand

- South African coal softens, met coke prices remain steady

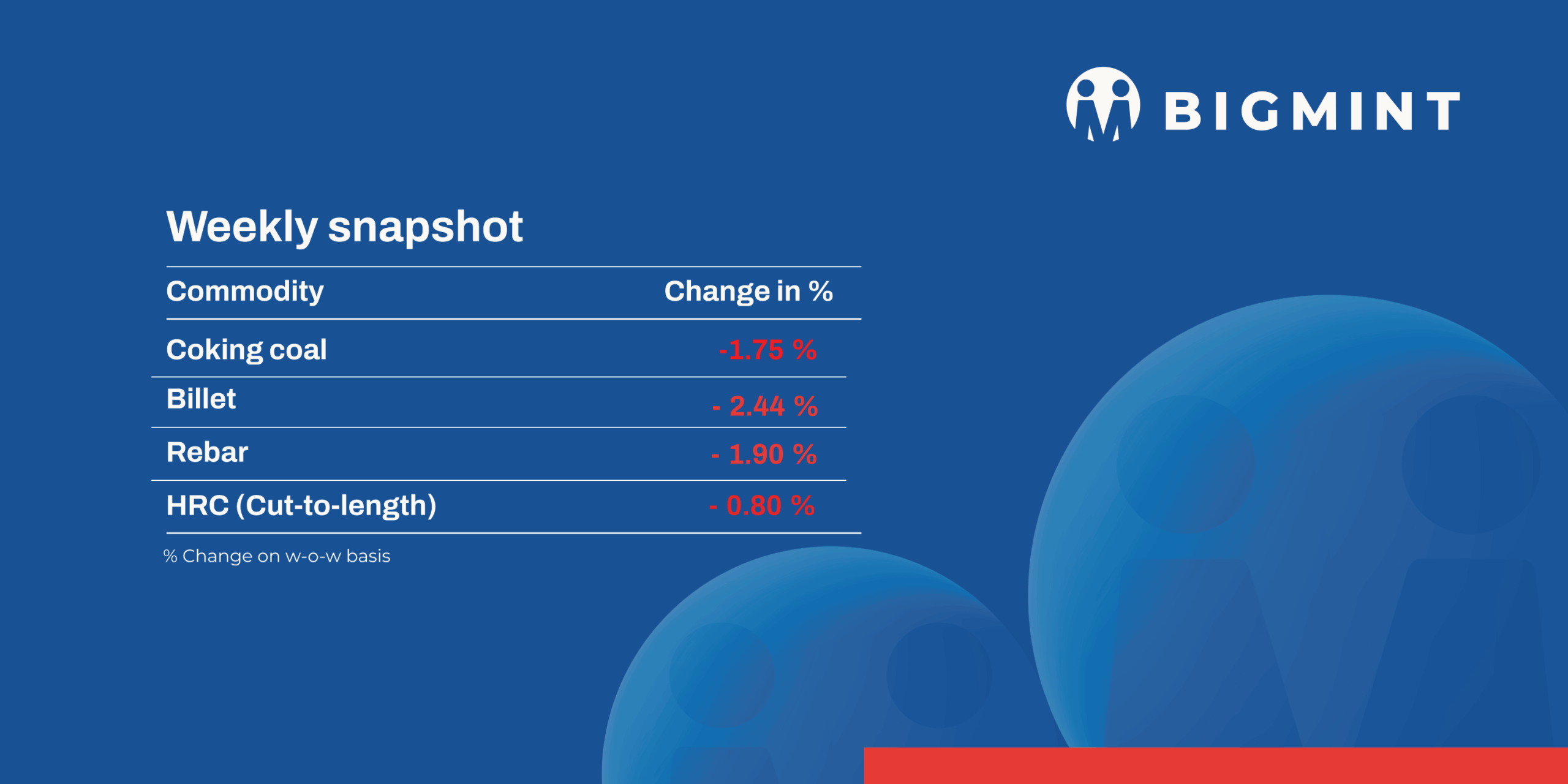

The domestic steel and raw materials market weakened in the week ended 18 April 2026, amid subdued downstream demand and cautious buying sentiment. Prices of semis, sponge iron, and finished steel declined, while raw material trends remained mixed, with softer seaborne coal, stable coke, and limited scrap activity due to weak trade conditions and logistical uncertainties.

Iron ore & pellet

OMC is set to auction 3.412 mnt of iron ore, comprising 1.44 mnt of lumps and 1.972 mnt of fines, on 18 April 2026. Ahead of the sale, the miner raised base prices of lumps by INR 500/t and fines by up to INR 250/t m-o-m, in line with recent hikes by NMDC Limited and Lloyds Metals and Energy Limited, which increased prices by INR 450-550/t, reflecting improved market sentiment. Notably, OMC has restricted trader participation in the upcoming e-auction.

Anandam Minerals Pvt. Ltd. won the Cudnem Mineral Block XIV in Goa’s 16 April auction, quoting a 115.25% premium. The 41.97-ha block holds 17.19 mnt of resources, including 7.47 mnt in-situ ore (Fe 54%) and 9.71 mnt dump material (Fe 51%).

SAIL auctioned a total of 31,980 t of iron ore from its Odisha mines, with the entire quantity successfully booked by 16 April 2026. This included 12,000 t of CLO (Fe 63%) from Bolani at INR 6,375/t, and 19,980 t of tailings (Fe 58.86%) from Barsua at INR 4,450/t, slightly above the base price of INR 4,375/t. All prices were on an ex-mines basis via road transport, inclusive of royalty, DMF, NMET, and applicable premiums.

Meanwhile, in Karnataka, NMDC conducted an auction for 48,000 t lumps from its Donimalai mines on 15 April, in which 16,000 t lumps (10-40 mm, Fe 55%) were booked at a base price of INR 2,539/t and 24,000 t lumps (10-40 mm, Fe 54%) were booked at INR 2,295/t. Prices exclude royalty, DMF, and NMET.

Coal

South African thermal coal prices at Indian ports declined by INR 200-300/t w-o-w, with ex-Paradip RB2 (5,500 NAR) at INR 10,900/t and RB3 (4,800 NAR) at INR 9,800/t. The decline was driven by weak buying interest, ample domestic coal availability, and continued preference for local sourcing. Market sentiment remained subdued with persistent bid-offer gaps, fluctuating seaborne offers, and cautious procurement keeping overall activity limited.

Domestic thermal coal prices increased by INR 100/t w-o-w, with 5,000 GCV at INR 6,700/t and 4,500 GCV at INR 5,300/t, supported by strong SECL auction premiums. However, buying remained limited due to weak sponge demand, and with higher auction volumes expected, prices may face pressure going forward.

US-origin high-CV coal prices remained stable in the range of INR 14,500-15,600/t at Indian ports, while over 2.5 mnt of cargo is en route to India. Strong inflows and cement and industrial players’ shift away from petcoke continued to support US coal consumption despite subdued spot activity.

Petcoke prices remained elevated, with delivered offers at $168-170/t and bids near $155/t, keeping trade unviable. Benchmark CFR India levels were around $158/t, but high prices and supply disruptions pushed buyers toward coal alternatives, significantly reducing demand.

Domestic BF-grade coke prices remained stable, with eastern India at INR 36,400/t ex-Jajpur and western India at INR 33,500/t ex-Gandhidham. Import parity remained firm with Indonesian coke at $288/t CFR India, while Australian coking coal prices eased to $231/t FOB, keeping the market balanced with a slight firm bias.

Ferrous scrap

The imported scrap market remained soft through the week, with slow finished steel demand and poor mill margins keeping buying interest subdued. HMS 80:20 offers from the UK/Europe/Africa/Australia were largely at $380-390/t CFR, while lower levels from Congo/Brazil/Latin America were heard at $360-375/t. Bids lagged at $370-378/t. A few deals were heard towards the weekend, while shredded offers stayed at $400-410/t with bids near $390/t, leading to a wide gap.

Market activity remained limited as mills preferred domestic scrap and adopted a wait-and-watch approach. Select deals were heard at $372-385/t for HMS and $340-345/t for LMS CFR, with prices easing slightly towards week’s end.

BigMint heard that around 8,000-8,500 t of imported scrap booked this week, primarily comprising 6,500-7,000 t of HMS (80:20 and variants) from multiple origins, with the balance including bundles, sub-grade scrap, turnings, and skull material.

Ferro alloys

Silico manganese

Indian silico manganese (60-14) prices moved down by INR 1,800/t ($19/t) w-o-w to INR 82,800-84,000/t ($891-$905/t) across key markets. The decline was driven by rising domestic supply and subdued export demand, as limited overseas bookings led producers to divert material into the local market, increasing availability and competitive pressure.

Meanwhile, HC 65-16 silico manganese export prices dipped by $18/t to $967/t FOB Vizag/Haldia.

Ferro manganese

Indian ferro manganese (70%) prices fell w-o-w by INR 2,000/t ($22/t) to INR 84,800/t ($913/t) in Raipur and by INR 1,800/t ($19/t) to INR 84,700/t ($912/t) in Durgapur. The earlier upward momentum was not sustained as demand weakened and buyers resisted higher offers. Meanwhile, export prices for 75% grade dropped sharply by $24/t w-o-w to $982/t FOB Vizag/Haldia amid limited fresh inquiries.

Ferro silicon

Indian ferro silicon (Si 70%) prices edged up by INR 1,000/t ($11/t) w-o-w to INR 107,000/t ($1,152/t) exw Guwahati, while Bhutan prices also rose slightly by INR 1,000/t ($11/t) to INR 108,000/t ($1,163/t). Prices rose as limited material was offered in the market, with key sellers focused on fulfilling previous bookings.

Ferro chrome

Indian high-carbon ferro chrome (HC 60%, Si 4%) prices held steady at INR 117,500/t ($1,25/t) ex-works Jajpur, with limited market movements. Odisha Mining Corporation scheduled a chrome ore auction of 124,400 t on 18 April, with the offered volume up 20,100 t m-o-m. Base prices were largely stable, slipping marginally by 0.5% (INR 96-131/t), while sub-40% grade fell 2% (INR 214/t), supporting overall ferro chrome price stability.

Semi-finished steel

India’s semi-finished steel market witnessed a sharp downturn this week, with billet prices across all key regions declining by INR 600-1,700/t ($6-18/t) w-o-w, as per BigMint’s assessment. Prices declined due to persistent weakness in finished steel offtake, which significantly curtailed buying interest in the semis segment. Market sentiment remained bearish throughout the week, as subdued downstream demand forced sellers to reduce spot offers aggressively to stimulate bookings.

Sponge iron prices mirrored the weakness in the semi-finished segment, declining by INR 300-1,100/t ($3-12/t) w-o-w across major regions. The downtrend was due to weak offtake from IF-based producers and cautious buying sentiment. Limited enquiries and subdued trade volumes kept market activity restricted, with most participants opting to secure material only for immediate requirements amid ongoing market volatility.

On the export front, Indian DRI offers reflected mixed sentiment. Export offers to Nepal decreased by $5/t w-o-w to $345/t CPT Raxaul, while offers to Bangladesh increased by $5/t to $366/t CPT Benapole. The rise in Bangladesh offers was driven by sellers attempting to align prices with volatile domestic trends, despite limited buying interest from overseas markets.

NMDC’s Nagarnar Steel Plant auctioned 7,000 t of steel-grade pig iron on 15 April, with the entire quantity booked at a base price of INR 38,000/t. Bids decreased by INR 200/t from the 9 April auction, when the entire 7,000-t quantity was sold at INR 38,200/t. The outcome reflects slightly subdued demand conditions and a mild downward price correction.

Finished long steel

IF-rebar: IF rebar trade prices fell w-o-w amid volatility across major markets this week. Trading activity remained subdued across regions. Demand stayed weak, particularly in finished and semi-finished steel, as buyers restricted purchases to immediate needs and adopted a cautious stance. Manufacturers reduced offers or provided discounts to liquidate material. Mills had inventory levels of around 8-12 days. In the near term, market participants expect continued price volatility due to weak booking orders in the finished segment.

On a w-o-w basis, rebar prices decreased by INR 500-2800/t across key regions as per BigMint’s assessment.

Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 51,700-52,300/t exw Jalna and INR 46,300-46,700/t exw Raipur.

Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 48,000-48,500/t exw-Raipur.

Trade reference prices of wire rod stood at INR 46,300-47,000/t ex-Raipur.

BF-rebar: Trade-level BF-rebar prices (distributor to dealer) edged down by INR 100/t ($1/t) w-o-w to INR 60,400/t ($650/t) exy-Mumbai, as per BigMint’s assessment on 17 April 2026. Prices have fell slightly in Mumbai, while in other markets, prices remained stable. Buying activity slowed down this week in the trade channel as buyers adopted a cautious approach and opted for need-based buying. Rebar project prices were in the range of INR 58,500-59,500/t ($630-641/t) on a landed basis, as per sources.

Flat steel

BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) declined by INR 600/t ($6/t) w-o-w to INR 59,300/t ($637/t) as of 14 April, compared to INR 59,900/t ($643/t) on 7 April.

Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) prices were assessed at INR 66,900/t ($719/t) on 14 April, marking a w-o-w decrease of INR 600/t ($6/t) from INR 67,500/t ($725/t) on 7 April.

India HRC prices edged lower this week amid subdued demand and cautious sentiment. Furthermore, trading activity remained sluggish across regions, with buyers limiting purchases strictly to immediate needs.

India’s bulk imports of HRCs touched 171,332 t as on 10 April. Around 129,851 t of additional cargoes are expected by early May.

India’s bulk exports of HRCs touched 14,378 t as on 10 April. Around 35,500 t of additional cargoes are expected.

Indian HRC export activity remained subdued during the week 7-14 April 2026, as re-escalating geopolitical tensions and persistent disruptions across key maritime routes continued to weigh on trade flows.

Leave a Reply