- Stronger enquiries and limited vessel supply support rates

- Pacific strength offsets Atlantic softness amid volatile fuel trends

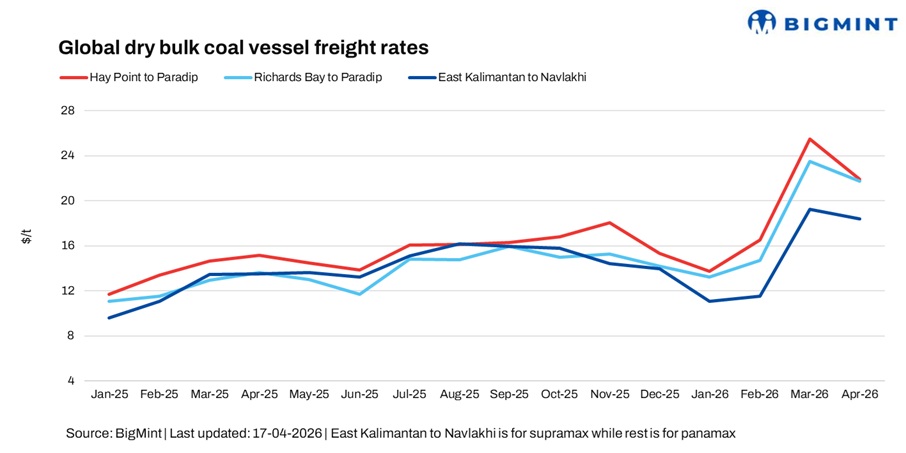

Dry bulk coal freight rates to India showed a firmer trend in the week ended 17 April, supported by improved enquiries and tightening vessel availability across key loading regions, even as pockets of oversupply continued to cap gains on select routes. Strength in the broader dry bulk market, led by Panamax and Supramax segments, also lent support to sentiment.

Market participants noted a gradual improvement in sentiment, though fixing activity remained uneven. A shipbroker source said, “Sentiment is positive, though bunker prices continue to fluctuate.”

Another shipbroker noted, “Cape, Panamax and Supramax segments are firming up, while Handysize remains relatively flat with early signs of improvement. Fixture volumes are lower than before, with stronger activity seen in the Pacific.”

However, challenges persist on certain routes. A ship-chartering source said, “Shipments are facing delays due to elevated freight rates to China, with fixtures still awaited.”

Overall, the market reflected firm demand in the Pacific and improving fundamentals, while the Atlantic basin remained relatively subdued due to ample tonnage.

Route-wise updates

Market highlights

- Bunker prices decline w-o-w: Bunker prices fell by $26.5/t week-on-week to $739/t as of 17 April, amid softer crude trends and improved availability across key bunkering hubs.

- Baltic index rises w-o-w: The Baltic Index climbed by 362 points week-on-week to 2,523 as of 16 April, driven by gains in the Panamax segment, up 128 points to 1,970, and the Supramax segment, up 105 points to 1,398, indicating improved momentum in dry bulk activity.

- DCE coke futures rise w-o-w: Coke futures on the Dalian Commodity Exchange increased by RMB 138/t ($20.23/t) week-on-week to RMB 1,778/t ($260.64/t) on 17 April, supported by firmer buying interest and improved steel sector sentiment.

- Brent crude futures remain volatile: Brent crude oil (June 2026 contract) was last assessed at $96.16/bbl on 17 April, up marginally from $96.02/bbl last week, amid evolving macroeconomic and supply-side cues.

Outlook

Coal freight rates to India are expected to remain firm with a slight upside bias, supported by tightening vessel availability and steady demand in the Pacific. However, ample tonnage in the Atlantic and elevated freight levels on select routes may keep fixing activity uneven.

While softer bunker prices could offer some relief, volatile fuel trends and regional imbalances are likely to keep the market cautious in the near term.

Leave a Reply