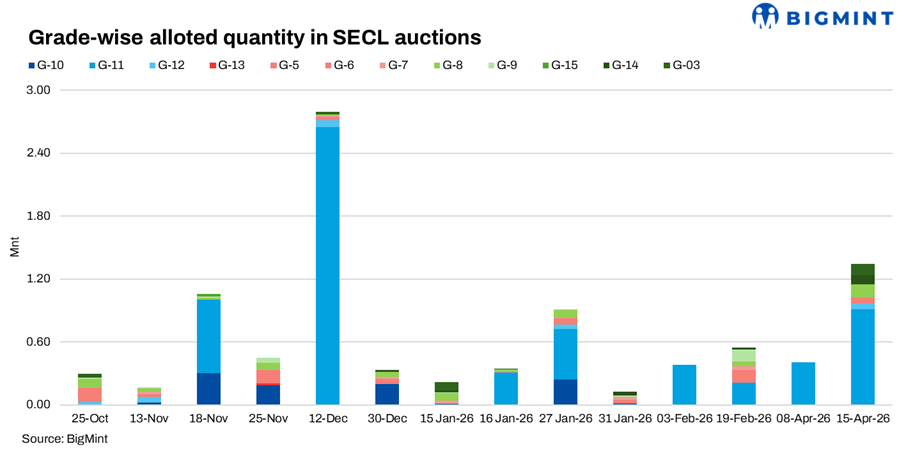

- Offered volumes surged sharply in 15 April auction across multiple grades

- Cement and sponge players participated actively in auction

South Eastern Coalfields Limited conducted two e-auctions on 8 April and 15 April 2026. The 8 April auction was limited to G11 grade with 404,000 t offered and fully allocated, while the 15 April auction saw a significant jump in offered volumes to 1,406,000 t across multiple grades including G3, G5, G6 to G9, G11, G12, and G14, reflecting a sharp rise in participation and volumes.

Total allocations increased substantially to around 1,341,850 t on 15 April, indicating broader participation and improved demand visibility across grades. The wider grade basket also attracted diverse buyers compared to the earlier auction.

G11 premiums stable, wider grade basket drives mixed pricing

In the 8 April auction, G11 coal recorded strong premiums, with the average final bid price at INR 2,491/t against a notified price of INR 1,184/t, translating to a premium of around 110 percent. Kusmunda OC dominated allocations with 400,000 t at around INR 2,496/t, while Gevra Road Siding saw smaller allocations at slightly lower levels.

In the 15 April auction, G11 premiums remained relatively firm, with Dipka OC (500,000 t) achieving around INR 2,501/t and Chhal OC (400,000 t) at INR 2,127/t. However, pricing trends varied across grades.

Higher grades such as G3 recorded strong premiums, with Churcha Siding reaching around INR 5,382/t, reflecting robust demand from sponge iron players. Similarly, G12 at Jampali OC saw strong realisations near INR 4,572/t.

In contrast, lower grades such as G14 at Baroud OC saw relatively modest premiums, with prices around INR 1,116/t, indicating selective demand and grade-specific buying strategies.

Mine-wise allocations reflect diversified sourcing

The 8 April auction was heavily concentrated, with Kusmunda OC accounting for nearly the entire allocation, indicating focused demand for G11 material.

In contrast, the 15 April auction saw diversified allocations across multiple mines. Key contributors included Dipka OC and Chhal OC in G11, while Baroud OC contributed significantly in G14. Churcha Siding and Churcha mines saw strong allocations in G3, while Amlai OC and Khairaha UG contributed to G8 volumes.

Other notable allocations were seen at Jampali OC for G12, Kurja UG for G6, and Rajgamar UG for G5, indicating balanced demand across mid and lower grades. This diversification reflects improved buyer flexibility and broader sourcing strategies.

Buyer participation expands significantly

Buyer participation expanded significantly in the 15 April auction compared to 8 April, indicating a broadening of demand across end-use segments. In the 8 April auction, participation was concentrated, with UltraTech Cement emerging as the largest buyer at 115,400 t, followed by Param Mitter Ventures and Mohit Minerals. Demand was largely driven by cement producers and trading players, reflecting a narrower buyer base.

By contrast, the 15 April auction saw participation extend across power, cement, and sponge iron sectors. Jindal Power Limited led purchases with 182,300 t across G11 and G12, while UltraTech Cement remained active with 85,000 t across G11 and G3. Sponge iron players, including B.S. Sponge and Sarda Energy, showed increased participation, particularly in higher grades such as G3.

Additional buying interest from players such as Indermani Mineral India, Phil Coal Benefication, Agarwal Coal Corporation, and Bharat Aluminium further indicates that demand was not only stronger but also more diversified across sectors.

Shift from imports to domestic reflected in auction demand

The strong participation and higher allocations in the 15 April auction also reflected a broader shift in buyer preference towards domestic coal. Amid elevated imported coal prices, volatile freight, and ongoing geopolitical uncertainty, many industrial users continued to move away from imported sourcing. Weak demand in imported markets, declining sponge iron prices, and persistent bid-offer gaps further discouraged purchases of seaborne coal.

As a result, buyers increasingly relied on domestic auctions to secure volumes at relatively stable and competitive prices. This trend was clearly visible in the wider participation across grades, particularly from sponge iron and power sector players, indicating that domestic coal is regaining share in the fuel mix.

Market insight

Stronger participation and higher allocations in the 15 April auction indicate a clear shift in buyer preference toward domestic coal. Cement players remained active and secured meaningful volumes, reflecting a move away from imported sourcing. Elevated imported coal prices, volatile freight, and geopolitical uncertainty continued to weaken the attractiveness of imports, driving this transition.

This shift was also reflected in broader participation across grades, particularly from sponge iron and power sector players, indicating that domestic coal is regaining share in the fuel mix.

Grade-wise trends further reinforce this. Stable premiums in G11 suggest steady baseline demand, while stronger realisations in G3 and G12 point to firm offtake from sponge iron and industrial users. In contrast, relatively lower premiums in G14 and select mid grades indicate more selective buying, with demand concentrated in specific segments rather than broad-based.

Leave a Reply