- Domestic price hikes support exporter confidence

- Taiwan prices firm near multi-month highs

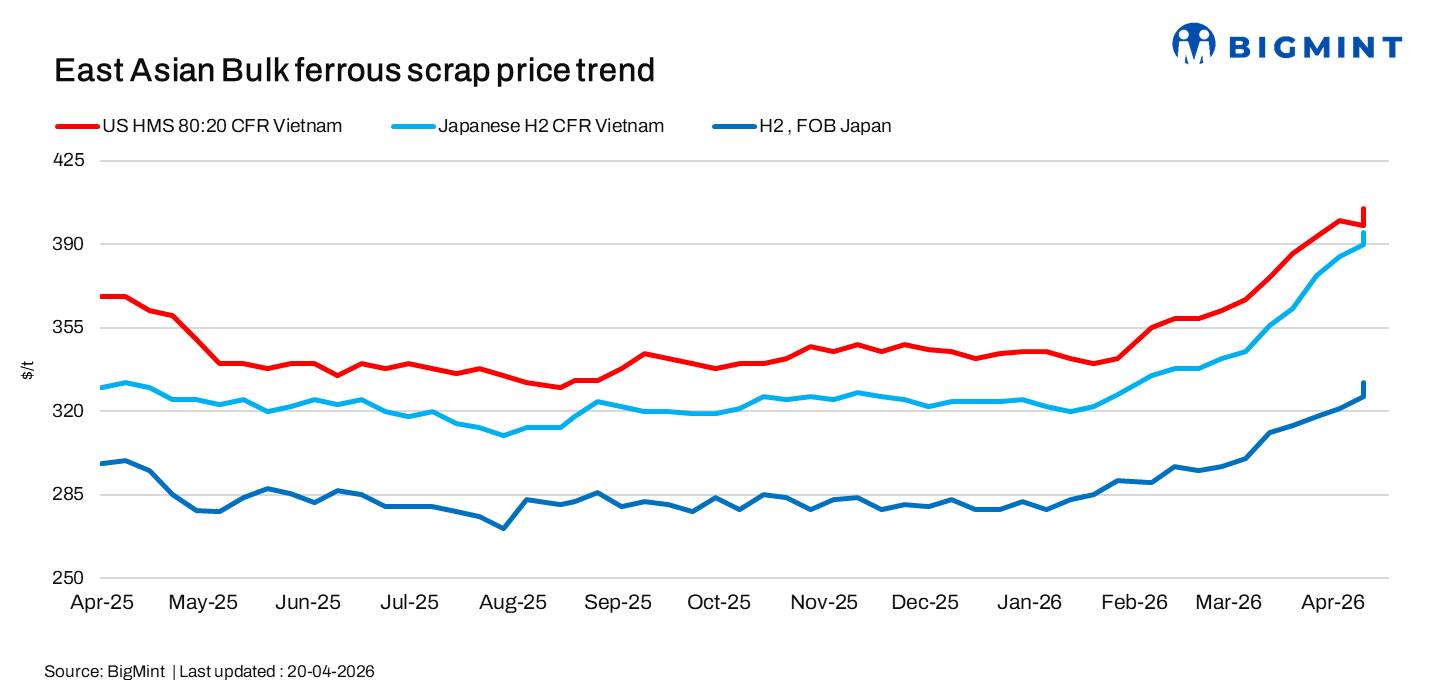

East Asian scrap markets strengthened in the week ended 20 April, supported by firm Japanese export offers and tight domestic supply. Strong domestic pricing boosted sentiment, though cautious buying in Vietnam and weak demand in Taiwan limited overall trading activity.

Weekly assessments

- Japanese H2 scrap was at $398/t CFR Vietnam, up by $8/t w-o-w.

- H2 scrap was at JPY 52,800/t ($332/t) FOB Tokyo Bay, up by JPY 800/t ($5/t) w-o-w.

- US-origin HMS 80:20 bulk stood at $408/t CFR Vietnam, up by $10/t w-o-w.

Japan: Export prices rise on firm domestic trends

H2 was assessed at JPY 52,800/t ($332/t) FOB Tokyo Bay, up JPY 800/t ($5/t) w-o-w. Limited scrap generation and ongoing commitments to fulfill contracts continued to tighten supply, supporting FAS levels. Japanese suppliers maintained strong price expectations, supported by higher domestic procurement rates. H2 export offers to Vietnam were heard above $390/t CFR, commonly in the $390-395/t range, up around $5/t w-o-w, with some higher-quality cargoes offered near $400/t CFR.

Tokyo Steel increased its scrap purchase prices by JPY 500/t ($3/t) across all plants, effective 16 April 2026, marking its third price hike this month. Prices now stand at JPY 53,000/t ($334/t), supported by strong domestic demand and firm global markets. Prices for the Takamatsu plant remain on hold.

Vietnam: Cautious buying amid rising prices

Vietnamese mills remained largely cautious, with indicative bids for H2 scrap heard around $380-390/t CFR. No fresh offers were reported, maintaining a widening gap with firm seller expectations and limiting deal activity.

Higher scrap prices have slowed buying interest as a result, mills continue to adopt a wait-and-watch approach. US-origin HMS 80:20 offers rising to around $405-410/t CFR Vietnam and bids improving to $390-400/t CFR, both up $10/t w-o-w.

However, April imports may slow due to higher global prices, rising freight costs, and tighter supply, with some mills shifting to domestic scrap.

Taiwan

Taiwan’s containerised scrap market remained firm, with HMS 80:20 prices near a 23-month high at $355-360/t CFR, supported by higher freight costs and tight supply. US-origin offers were at $360-365/t, with deals around $355/t amid limited activity. Japanese bulk offers (H1/H2) stood higher at $388-390/t, as strong domestic demand in Japan reduced export availability. Elevated scrap prices pushed some Taiwanese mills toward billet imports, while domestic scrap costs rose due to competition. However, weak construction demand kept rebar sales subdued, resulting in a cautious market sentiment.

Outlook

We expect prices to remain firm in the near term, supported by tight Japanese supply, higher domestic prices, and constrained export availability. However, cautious buying sentiment in Vietnam and the availability of alternative raw materials may continue to limit trading volumes despite upward price pressure.

Taiwan scrap prices likely to stay firm on tight supply and freight, but weak construction demand and billet substitution may limit further upside.

Leave a Reply