- Pre-auction caution keeps activity low, buyers hesitant

- Chinese prices slips on weak stainless steel demand

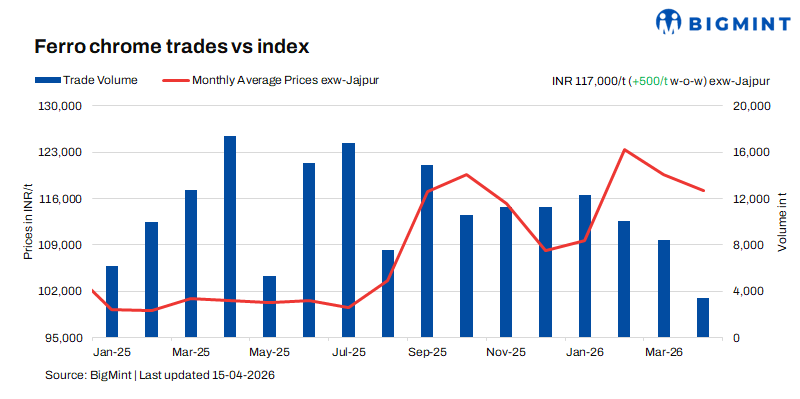

Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices stayed largely stable last week, inching up slightly by INR 500/t ($5/t) as compared to the assessment on 8 April. Market witnessed minimal movement in last week and with upcoming OMC’s auction, prices didn’t fluctuate much.

As per BigMint’s assessment on 15 April, high-carbon ferro chrome (HC 60%, Si: 4%) prices in India were INR 117,500/t ($1,259/t) exw-Jajpur. Around 2,400 t of material was traded last week within the price bracket of INR 116,000-121,000/t ($1,243-1,297/t) exw.

Meanwhile, low-silicon high-carbon ferro chrome (HC 60%, Si: 2%) prices edged up by INR 600/t ($6/t) w-o-w to INR 122,600/t ($1,314/t) exw-Jajpur. Low-carbon ferro chrome (C: 0.1%) prices witnessed an increase of INR 4,000/t ($43/t) w-o-w to INR 237,000/t ($2,540/t) exw-Durgapur. The increase was likely due to rise in raw material costs.

Market summary (9-15 April)

Lesser activity as OMC auction approaches: With OMC’s chrome ore auction scheduled for the 18th of this month, market activity remained largely subdued last week, as participants typically adopt a cautious approach ahead of it. While some sellers continued to hold firm offers at around INR 122,000/t ($1,307/t) exw, market sentiment was influenced by reports of a bulk deal concluded near INR 116,000/t ($1,243/t) exw levels. Although this transaction could not be independently verified at the time of reporting, it created uncertainty among buyers. As a result, most buyers stayed on the sidelines, hesitant to commit to significant purchases, anticipating clearer price direction post-auction and preferring to avoid potential downside risks in the near term.

Stainless steel market firm, longs outperform flats: Stainless steel prices for 304 grade HRC stayed unchanged w-o-w at INR 217,000/t ($2,325/t) exw-Mumbai. Market stayed firm this week, supported by better sentiment and tighter raw material supply. Long products performed better than flats due to supply constraints and steady demand from industrial buyers. Limited availability of key inputs and gas shortages continued to affect mill operations, supporting prices.

Flat products remained largely stable as demand stayed weak and buyers resisted higher offers. Most preferred small, need-based purchases, expecting a possible correction after the recent nickel-driven rise.

In contrast, long products saw improved movement due to selective bookings and tighter supply. Prices of some grades increased, supported by higher replacement costs.

Scrap shortages, especially for higher grades, remained a concern, forcing some producers to adjust raw material mixes. Overall, the market is expected to stay firm, but cautious buying may continue due to demand uncertainty as stainless steel production curbs continue.

China’s market trends: Ferro chrome (HC60%) prices in China fell slightly by RMB 250/t ($37/t) w-o-w to RMB 8,750/t ($1,283/t) exw-Inner Mongolia. Overall, the ferro chrome market showed stability with mild downward pressure. Strong chrome ore costs continued to support prices, even as demand from the stainless steel sector stayed weak.

Chrome ore prices remained firm due to high mining and logistics costs, with suppliers maintaining steady offers. However, concerns over possible production cuts affected sentiment.

On the demand side, stainless steel mills showed limited buying interest, relying on existing inventories and making only need-based purchases.

Outlook

Prices are largely expected to stay at current levels in the coming days. OMC’s chrome ore auction on 18 April will further shed light on the price trends.

Leave a Reply