- Freight disruptions, rising energy costs tighten supply

- Active mill buying offsets higher global cotton stocks

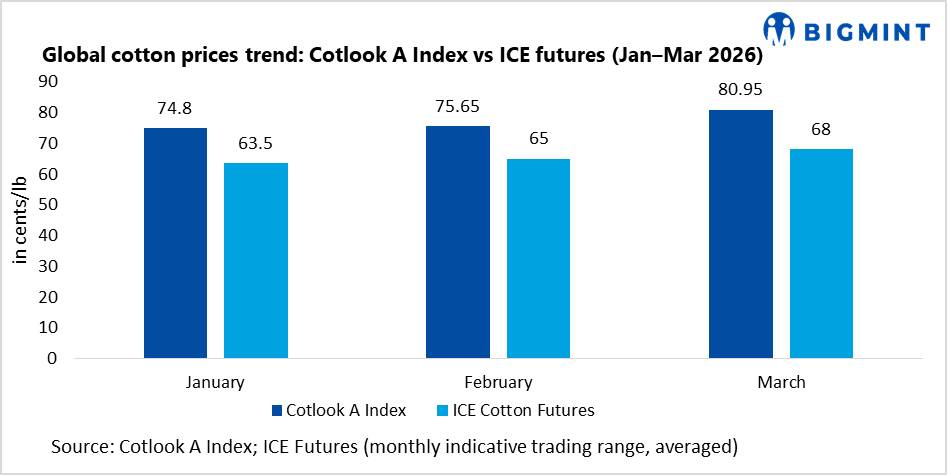

Global cotton prices strengthened in March 2026, with the Cotlook A Index rising 5.30 cents/lb m-o-m to 80.95 cents/lb, the highest since December 2024, while the May futures on the Intercontinental Exchange (ICE) settled at 70 cents per lb. The rally was largely driven by external disruptions rather than a structural tightening of supply.

The escalation of conflict in the Middle East and the effective closure of the Strait of Hormuz disrupted global shipping flows, leading to a sharp increase in crude oil prices and freight costs. For cotton traders and exporters, this resulted in delayed shipments, higher logistics costs, or tighter prompt availability. Consequently, basis levels firmed across key origins, reflecting supply chain constraints rather than underlying production shortages.

Mill demand remains steady despite rising costs

Global mill demand remained resilient, with spinners continuing to book cotton to meet near-term yarn commitments. Improved yarn offtake and better realisations supported procurement, although concerns around rising energy costs and logistics disruptions persisted.

Vietnamese spinning mills showed a strong preference for US cotton, driven by retail-linked demand. Bangladeshi mills continued sourcing Brazilian and West African lint, while Pakistan buyers focused on lower-priced recaps, with some mills delaying purchases due to elevated prices. Turkish spinners remained active amid improving downstream demand, supporting overall trade flows.

China contributed to demand sentiment by allocating 300,000 tonnes (t) of sliding-scale import quotas for processing trade, enabling mills to secure cotton for export-oriented production.

Higher supply outlook limits upside potential

On the supply side, global fundamentals remained relatively comfortable. The United States Department of Agriculture (USDA) raised global ending stocks for 2025/26 to 76.39 million bales (+1.28%), reflecting higher production and slightly lower consumption estimates. This continues to cap sharp upside in prices despite current support from disruptions.

In the US, export commitments at 9.9 million bales remain below last year’s pace, though recent weekly sales improved, particularly to Vietnam, Turkiye, and China. The Prospective Plantings report indicated a 4% increase in acreage to 9.64 million acres, suggesting higher output potential, although drought conditions in Texas remain a key risk.

Globally, favourable crop progress in Brazil and increased sowing in Pakistan support supply expectations, while India’s production estimate was revised higher to 32.05 million bales.

The market is expected to remain volatile in the near term. For ginners, spinning millers, and traders, a buy-on-dips approach is likely, as supply chain disruptions provide support while higher global stocks limit sustained upside.

Leave a Reply