- Slab imports continue replacing finished flats

- Imports remain limited to need-based buying

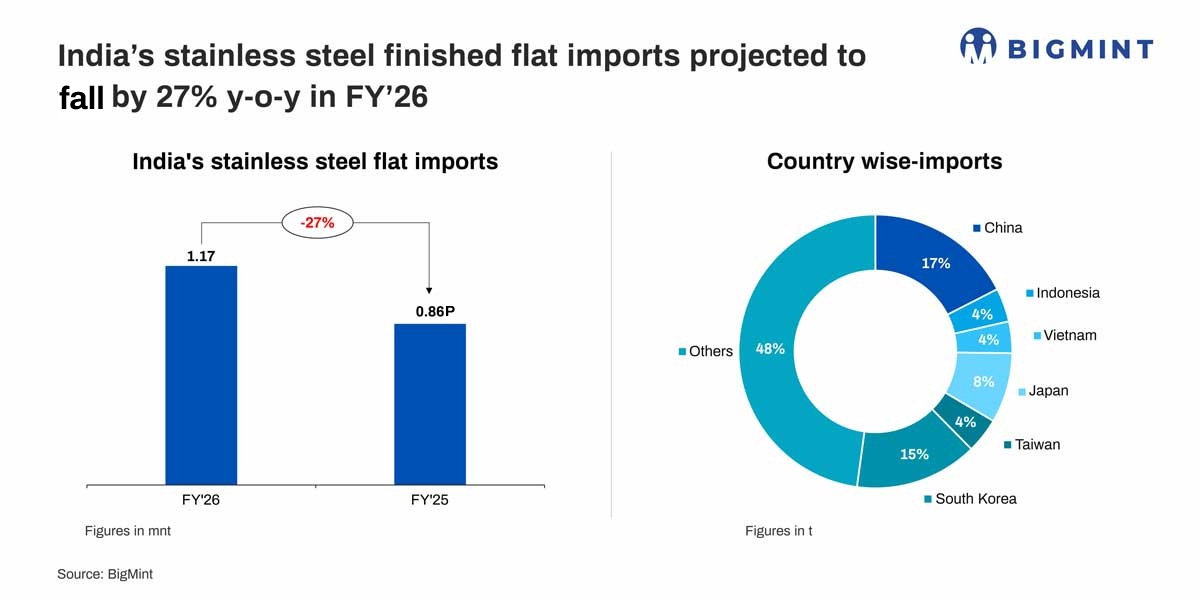

India’s stainless finished flat steel imports are estimated to decline by 27% y-o-y to around 0.85 mnt in FY’26, compared with 1.17 mnt in FY’25, reflecting a shift in sourcing dynamics and stronger domestic supply.

The drop was largely driven by the collapse in shipment from major importing countries such as Indonesia, Vietnam and China.

Import trends and country-wise decline

The decline was largely driven by a sharp drop in shipments from key suppliers. Imports from China are projected to decline by 56% y-o-y to 0.15 mnt, while Indonesia’s volumes may fall steeply by 88% to 29,000 t. Vietnam also saw a 76% decline to 32,000 t amid weaker buying interest and regulatory tightening.

Series-wise, 300-series imports are expected to drop the most, down 39% y-o-y from 0.55 mnt in FY’25. Meanwhile, 400-series imports may decline by 8%.

China loses dominance as sourcing patterns change

China, traditionally India’s largest supplier of stainless steel flats, is projected to witness shipments plunge by around 56% y-o-y, compared with 0.34 mnt in FY’25. This decline accounted for a major share of the overall reduction in India’s finished flat imports.

Similarly, Indonesia’s shipments are estimated to sharply drop by nearly 88%, to 29,000 t from 0.24 mnt a year earlier. Imports from Vietnam also may decline significantly by around 76%, to 32,000 t from 0.13 mnt, reflecting weaker buying interest and regulatory tightening.

Key factors behind import slowdown

Regulatory impact and BIS extension

Stricter enforcement of quality control norms and customs vigilance weighed on import volumes. However, the government has extended the exemption from mandatory BIS certification (IS 6911, IS 5522, IS 15997) for stainless flat steel imports until 30 September 2026, from the earlier deadline of 31 March. This temporary relief is expected to ease supply constraints and support import flows in the near term.

Rising slab imports from Indonesia

India’s stainless steel slab imports are expected to reach around 0.72 mnt in FY’26, compared with 0.40 mnt in the previous year. For domestic flat producers, importing slabs has remained commercially viable amid firm nickel prices and elevated alloy surcharges.

Instead of expanding domestic melting-which exposes mills to volatile ferro alloy prices and higher power costs-many producers opted to import slabs and convert them into finished flats, helping optimise rolling margins and working capital cycles.

Imported slab prices were heard at around $1,575–1,630/t CFR Paradip and Dhamra during the period.

China’s export discipline and pricing strategy

China’s tighter control over steel exports also contributed to the drop in shipments to India. From January 2026, Chinese authorities introduced export licensing requirements for several steel products, including stainless steel flats, aimed at strengthening export monitoring and discouraging aggressive low-priced shipments.

The additional documentation and approval procedures created uncertainty and shipment delays in the early phase, prompting Chinese mills and traders to adopt a more cautious export strategy and prioritise domestic market stability.

Dollar strength and shift in sourcing strategy

A stronger US dollar, which rose nearly 5% in FY’26 to 88.71 compared to 84.60 in FY’25, significantly increased the landed cost of stainless steel imports. The currency uptrend, along with volatility, discouraged forward import bookings and pressured importer margins. Coupled with elevated freight and alloy-linked costs, this pushed buyers toward domestic procurement and slab imports to better manage cost efficiency and supply risks.

Higher domestic production

India’s domestic stainless flat steel production is projected to increase to around 3.1 mnt in FY’26, up 15% y-o-y from 2.6 mnt in the same period last year. The rise in domestic output helped partially offset lower imports, supported by steady capacity utilisation among major producers.

Outlook

India’s stainless flat steel imports are expected to remain under pressure in the near term despite the BIS exemption extension until September 2026. While the temporary relief may support selective import inflows, structural factors including higher domestic production, elevated dollar levels, and a continued shift toward slab imports are likely to limit a sharp rebound.

Market participants indicated that import volumes will remain need-based, with buyers cautiously monitoring price spreads and currency movements. The US dollar ruling at around 92-93 is further reducing the incentive for imports, as higher landed costs continue to weigh on buyer interest. At the same time, improved domestic capacities are increasingly fulfilling demand, reducing reliance on overseas material.

Any sustained recovery in imports will depend on stronger downstream demand, easing freight costs, and greater clarity on future regulatory direction.

Leave a Reply