- Ample supply keeps prices soft

- Morbi ceramic restart may support demand

Indian portside prices of Indonesian-origin thermal coal declined marginally w-o-w as on 10 April, primarily due to steady cargo arrivals, comfortable inventory levels at ports, and cautious procurement by buyers.

The overall market remained relatively balanced, with adequate supply availability limiting any significant upward price movement despite ongoing consumption from key non-power sectors.

Ceramic sector demand remains uncertain

Demand from the ceramic sector, a major consumer of imported Indonesian coal, remains somewhat uncertain due to operational constraints and rising energy cost pressures.

Market participants indicated that India’s ceramic exports continue to remain strong, necessitating the operation of manufacturing units. However, earlier regulatory measures had encouraged ceramic units to shift from coal to gas-based systems through the installation of gasifiers. With natural gas prices currently nearly double that of coal, any further increase in gas prices could significantly impact production economics and threaten the sector’s operational viability.

Additionally, industry participants highlighted that ceramic units in Morbi, Gujarat – India’s largest ceramic manufacturing hub – are expected to gradually resume operations between 15-20 April. At present, only limited capacity has been permitted, with some plants operating at around 65% utilisation and others at approximately 85%. As restrictions ease and capacity utilisation improves, demand for imported coal from the ceramic sector may gradually recover.

Portside prices soften across key Indonesian grades

Portside prices across most Indonesian coal grades recorded slight corrections during the week, reflecting balanced supply-demand dynamics and sufficient stock availability in the market.

According to the latest assessment by BigMint, prices of 5,000 GAR Indonesian coal declined by around INR 100/t w-o-w to approximately INR 9,300/t at Kandla and INR 9,200/t at Visakhapatnam.

Similarly, prices of 4,200 GAR coal dropped by about INR 150/t to around INR 7,450/t at Kandla and INR 7,350/t at Visakhapatnam. Lower-grade 3,400 GAR coal prices also edged down slightly by around INR 50/t w-o-w to nearly INR 5,400/t at Navlakhi Port. The modest decline reflects subdued spot buying activity amid adequate cargo availability.

Port inventories increase on continued cargo inflows

Thermal coal inventories at Indian ports witnessed a moderate rise during the week, supported by fresh cargo arrivals across several major ports. Total portside stocks increased by approximately 3.3% w-o-w to 13.53 million tonnes (mnt) in week 14, compared with 13.10 mnt in week 13.

Notable inventory build-ups were observed at key ports such as Paradip, Mundra, and Magdalla, indicating steady import inflows along both the eastern and western coasts. The rise in inventories suggests that near-term supply availability in the import market remains comfortable.

Power sector coal stocks remain comfortable

Coal inventories at Indian thermal power plants also improved slightly during the week, reinforcing the comfortable supply position within the domestic power sector. As of 9 April 2026, total coal stocks at thermal power plants stood at approximately 59.6 mnt, equivalent to nearly 19 days of consumption.

However, stock distribution across plants continues to remain uneven. Around 21 thermal power plants are currently operating with critical coal inventory levels, including 11 plants dependent on domestic coal supply, seven reliant on imported coal, and three operating on washery rejects. This highlights ongoing logistical and supply chain challenges in certain regions despite the overall healthy national stock position.

Mixed trends in international coal benchmarks and freight

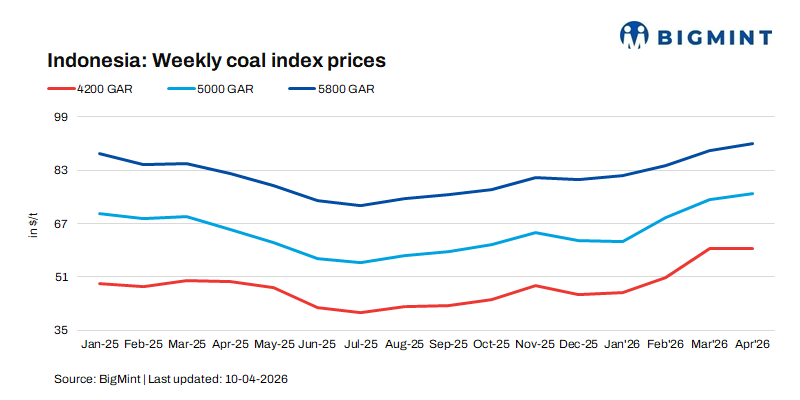

Global market indicators presented mixed signals during the week. Indonesian benchmark prices for higher-calorific coal grades recorded marginal increases, with 5,800 GAR coal rising by around $0.2-0.3/t w-o-w. In contrast, prices of 4,200 GAR coal declined slightly by approximately $0.1-0.12/t, while 3,400 GAR coal prices registered a modest increase of about $0.4-0.5/t.

Freight rates for shipments to India remained largely stable, with Supramax freight from East Kalimantan to Navlakhi stable around $0.3/t w-o-w to approximately $18.3/t, indicating relatively steady shipping conditions.

Outlook

Indian portside prices of Indonesian thermal coal are expected to remain stable to slightly soft in the near term, supported by comfortable inventories and steady cargo arrivals. However, demand may improve with the gradual resumption of Morbi ceramic units, while mixed global cues and stable freight rates are likely to keep prices range-bound.

Leave a Reply