- Cautious sentiment, shipowners adopt wait-and-watch approach

- Volatile bunker prices keep freight sentiment uncertain

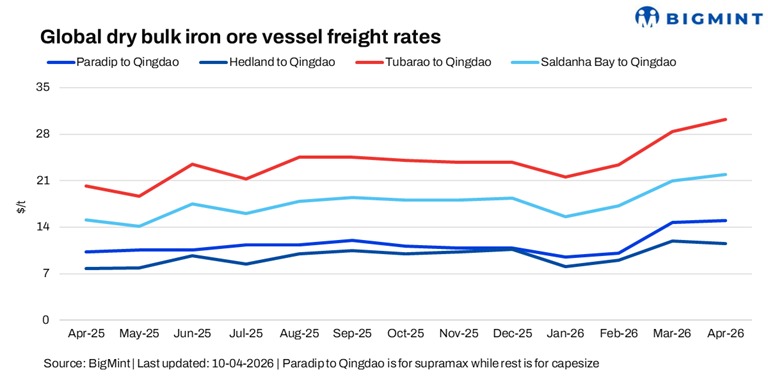

The dry bulk iron ore freight market is showing a mixed sentiment w-o-w, with clear divergence between the Pacific and Atlantic basins. In the Pacific, sentiment has strengthened notably, supported by a pickup in cargo volumes from Western Australia and increased spot fixtures. Active participation from major miners and tighter prompt vessel availability have lent support to rates, keeping the momentum slightly positive.

In contrast, the Atlantic basin remains relatively subdued. The Brazil-China route continues to see limited fresh fixtures, with a noticeable gap between bid and offer levels reflecting cautious sentiment among charterers and owners. The South Africa-origin routes remained quiet with minimal trading activity and no significant fresh fixtures, further reinforcing the soft tone in the Atlantic segment.

“The freight market remains uncertain amid geopolitical tensions and volatile bunker prices. Although a temporary pause in the conflict offers some relief, cargo movement is expected to stay limited. With the market still unstable due to fuel price fluctuations, fixture activity remains thin as many charterers adopt a wait-and-watch approach,” a source informed BigMint.

- Baltic index gains w-o-w: The Baltic Dry Index gained 95 points w-o-w to 2,161 on 9 April, supported by improved cargo demand, stronger Pacific iron ore shipments, and increased chartering activity post-holiday. Additionally, Capesize surged 149 points to 3,235, while Supramax hiked by 69 points to 1,293.

- Bunker prices drop w-o-w: Bunker prices dropped by $124.5/t w-o-w to $765.5/t on 10 April, pressured by a sharp decline in crude oil prices and easing geopolitical risk premium following temporary de-escalation in conflict.

- DCE iron ore futures decline w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) declined by around RMB 24.5/t ($3.5/t) w-o-w to RMB 775/t ($113.4/t) on 10 April, weighed by softer steel demand outlook and cautious sentiment amid macroeconomic uncertainty in China.

- Brent crude futures drop w-o-w: Brent crude oil (June 2026 contract) was last assessed at $96.02/bbl on 10 April, dropping by $13.01/bbl w-o-w, amid easing supply concerns, reduced geopolitical tensions, and expectations of stable global oil supply.

Outlook

Freight market outlook remains uncertain amid geopolitical tensions and volatile bunker prices. However, with easing war concerns, sentiment may gradually improve, though limited cargo visibility could keep rates under pressure in the near term.

Leave a Reply