- Rising production in key origins increases supply

- Weak import demand, rising stocks limit price upside

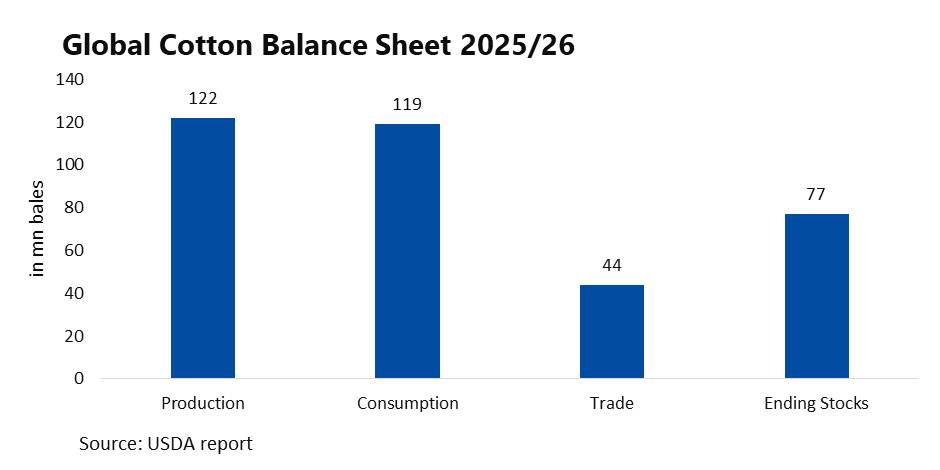

The global cotton market is entering a phase of balance in the 2025/26 marketing year, as higher production across major origins offsets a modest recovery in demand. According to the latest USDA assessment, global cotton output is projected to increase by nearly 900,000 bales to 121.9 million bales, led by larger crops in China, India, and Pakistan.

While global consumption is also expected to rise to 119.1 million bales, the increase remains uneven. Higher mill use in China and India is being partially offset by weaker demand in Bangladesh and Vietnam, indicating that downstream textile demand remains inconsistent. For spinning millers, this reflects continued pressure on yarn margins and cautious procurement behaviour.

Trade flows weaken amid cautious buying

Global cotton trade is forecast to decline marginally to 43.7 million bales, primarily due to reduced imports by Bangladesh, Pakistan, and Vietnam. The slowdown in buying from these key importing regions suggests that spinning millers are largely operating on hand-to-mouth purchases, avoiding large inventory build-ups amid uncertain demand visibility.

On the export side, lower shipments from India are expected to weigh on global trade volumes, even as some increase from Kazakhstan offers limited support. At the same time, Australia’s export outlook remains firm, supported by strong beginning stocks and improved shipments to China and India, highlighting shifting trade flows across origins.

Stock build-up caps bullish sentiment

Global ending stocks are projected to rise by around 700,000 bales to 77 million bales, with higher inventories concentrated in China and India. This stock accumulation signals comfortable supply availability in the global market and reduces urgency for aggressive buying.

For traders and ginners, rising stocks act as a key overhang, limiting sustained price rallies unless supported by stronger offtake. The current balance sheet suggests that supply is outpacing effective demand, keeping the market structurally capped.

Price trend supported by sentiment, not fundamentals

Cotton futures on ICE have increased by around 7 cents to approximately 71 cents per pound since the previous WASDE update. However, this recovery appears to be sentiment-driven rather than backed by strong physical demand.

The divergence between futures strength and weak physical trade indicates that rallies may face resistance at higher levels, particularly in the absence of strong export demand or yarn market recovery.

Market outlook remains range-bound

The global cotton market is expected to trade within a narrow range in the near term, with a slight negative bias. Higher production and rising stocks are likely to weigh on prices, while demand recovery remains gradual and uneven.

For market participants, ginners may face resistance in passing higher prices, while spinning millers are expected to continue need-based buying. Traders are likely to adopt a cautious approach, with selling interest emerging on price upticks unless supported by a clear improvement in global demand or supply disruptions.

Leave a Reply