- US domestic scrap prices drop on improved supply

- In Europe, some yards operating 20% lower than last year

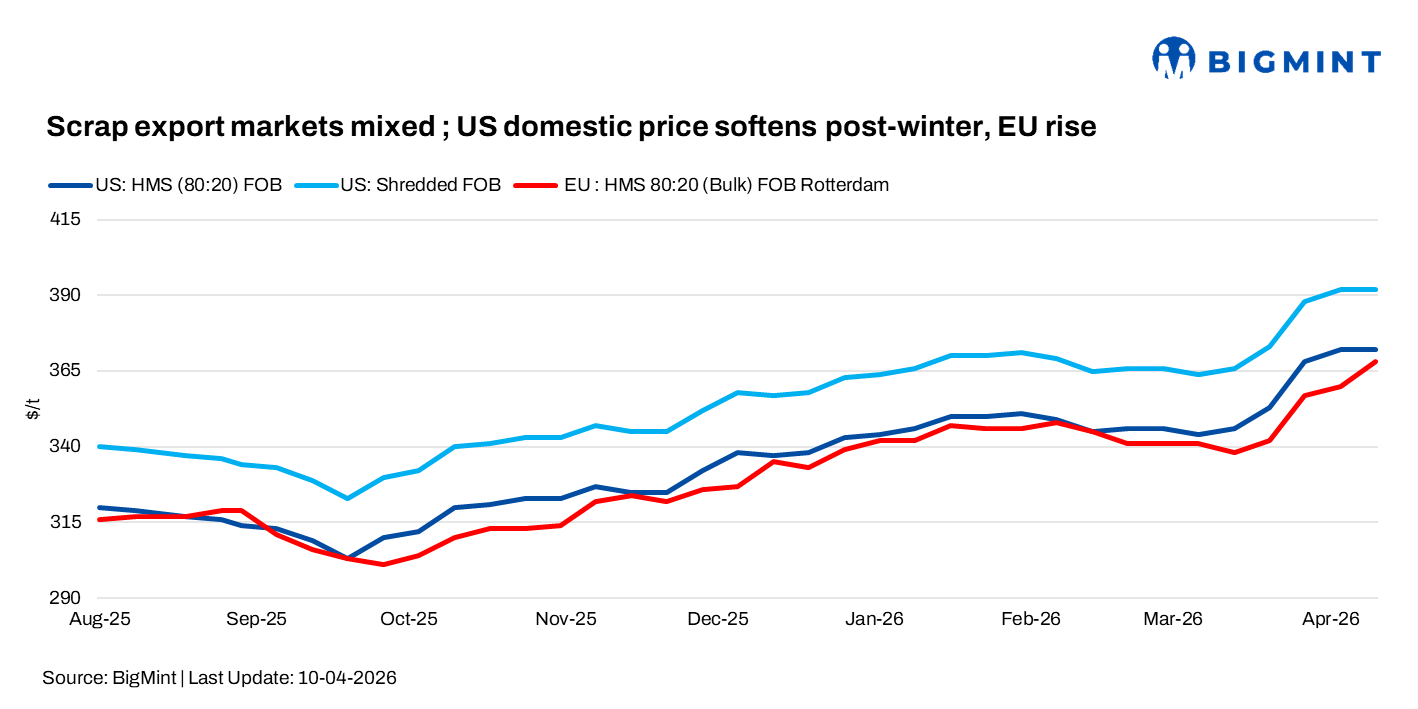

The global ferrous scrap export market remained stable this week, with both the US and EU markets holding steady. Brazil stayed quiet ahead of tax clarity, while supply dynamics and regional demand continued to shape overall sentiment.

US

US ferrous scrap prices as on 10 April 2026 remained stable w-o-w, with HMS 80:20 at $372/t FOB and shredded scrap at $392/t FOB, showing no change compared to the previous week.

Domestic ferrous scrap prices for obsolete grades declined in early April, pressured by improved supply after the winter slowdown. Shredded scrap fell to $430-440/t (down $10-20/t), while P&S dropped to $410-420/t and HMS to $380-390/t across key regions. Overall, the market settled in line with expectations, with obsolete grades weakening while tighter supply and steady demand kept prime scrap prices stable.

Improved weather conditions boosted scrap flows, leading to surplus supply and weighing on prices. Market sentiment remained weak for obsolete grades, with mills securing lower-priced deals amid ample availability.

Regional trends varied, with the Southeast more influenced by export dynamics, while the Midwest saw relatively sharper domestic corrections. Despite stronger Turkish buying lifting export shredded prices to around $390+/t FOB US East Coast, export activity had limited impact on the domestic market.

Europe

The UK/EU scrap market remained largely stable, with bulk scrap prices rising w-o-w amid slower collection activity. Some yards continued to operate at around 20% lower levels y-o-y.

HMS 80:20 (bulk) FOB Rotterdam increased to $368/t, up by $8/t from $360/t w-o-w.

Higher collection costs and a stronger euro continued to pressure seller margins, limiting aggressive selling despite stable price trends.

India buying interest weakened with slightly lower workable levels, while Pakistan Port Qasim and Bangladesh demand supported the market.

Export price indications stood at EUR 330-345/t FOB ($386-403/t) for shredded (E8) and EUR 290-310/t FOB ($339-362/t) for HMS (E3). DAP dock levels were around EUR 300/t ($351/t) for HMS and EUR 310/t ($362/t) for shredded. Overall, offers to India remained broadly stable despite weak sentiment, while Pakistan and Bangladesh demand provided some support to export pricing.

The EU has set CBAM at euro 75/t CO₂ ($81/t), which is expected to push steelmakers toward EAF production and increase domestic scrap demand. Higher carbon costs on primary steel will raise scrap usage in Europe, likely reducing export availability. This tightening of EU scrap exports may support global prices and strengthen scrap’s role in decarbonisation.

Brazil

Scrap prices saw slight support due to rising diesel costs and tax-related adjustments, with some increases reported in mixed grades. Domestic HMS 80:20 prices stood at BRL 840-850/t ($166-168/t), turnings stood at BRL 760-770/t ($150-152/t), and clean scrap at BRL 920-930/t ($182-184/t).

Brazil’s ferrous scrap market remained subdued in early April, as uncertainty over upcoming PIS/Cofins tax rule changes kept trading activity limited. Market participants expect clarity within the next two weeks, while pricing remained inconsistent with no official mill cuts.

Export prices were largely stable, with HMS at $290-300/t FOB and shredded scrap up $5-6/t to $310-315/t, supported by shipments to India, Pakistan, and Bangladesh. Brazil-origin shredded offering at $419/t for April loading (550 t, 2-3% impurities for 50-55 days transit) CFR Qasim.

Outlook

Global scrap export markets are expected to remain range-bound in the upcoming days. In the US, ample supply may continue to pressure obsolete grades, though downside could be limited if flows stabilise. Europe is likely to see steady-to-firm conditions, in long-term supported by CBAM-driven domestic demand and tighter export availability.

Leave a Reply