- Mills shift focus to cheaper billet imports

- Fresh bookings on hold amid weak rebar demand

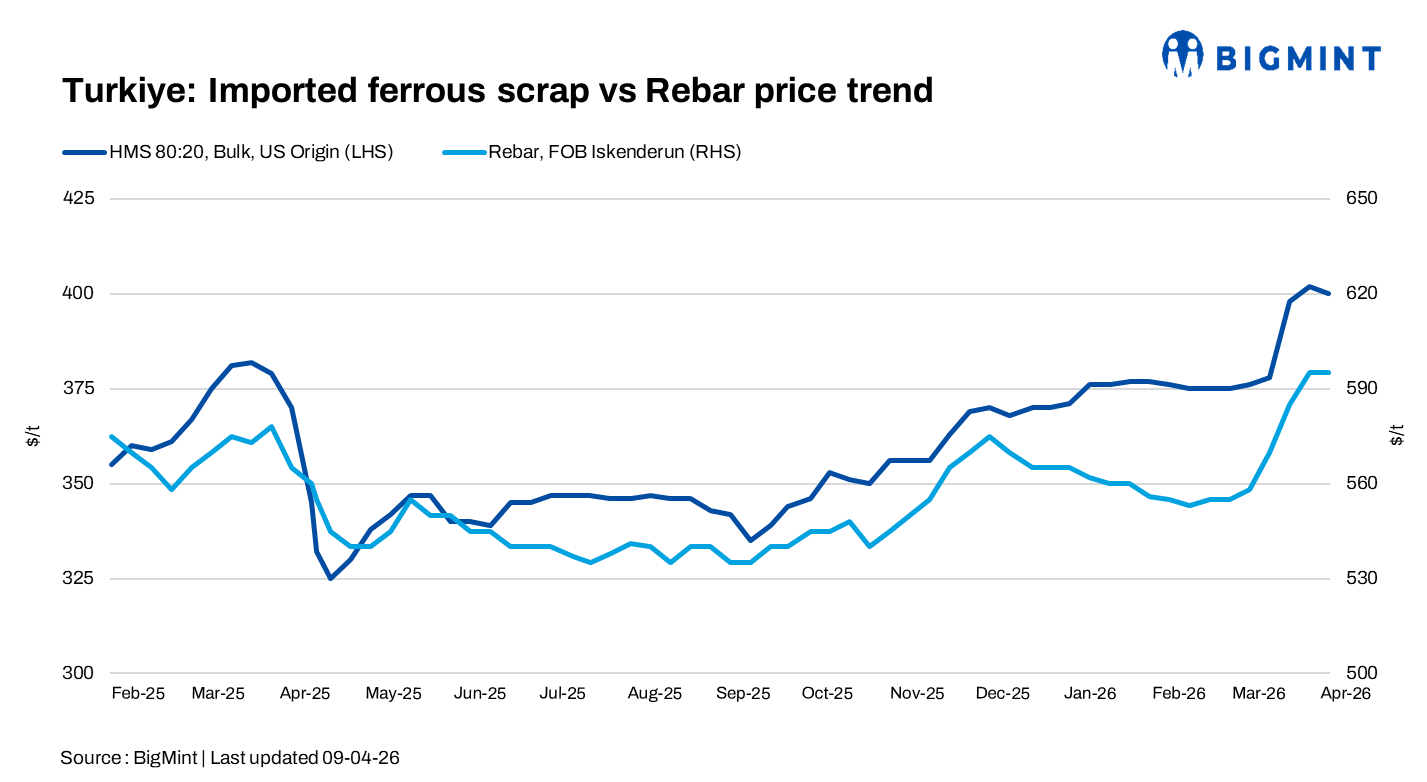

Turkish deep-sea scrap prices slightly decreased, with HMS 80:20 at around $400/t CFR on 9 April, as trading activity slowed amid uncertainty over the US-Iran conditional ceasefire. Overall activity stayed muted, as mills are largely covered for April-May and weak finished steel sales continue to weigh on buying interest.

Tradable levels for HMS 80:20 were heard between below $400/t and $405/t CFR, indicating a narrow workable range. While some expect prices to soften if the ceasefire holds-on the back of easing freight-others believe high energy costs and a stronger euro may limit downside.

Meanwhile, collection costs in the Benelux region stood at euro 290-300/t, implying breakeven export levels of $390-400/t CFR, which kept seller offers firm despite weak buying interest.

Market participants stated “the last US-origin HMS was offered at $405-425/t CFR, with no deals concluded, while Baltic/EU suppliers remained absent from the market with cautious sentiment. As a result, participants have adopted a wait-and-see approach, with no fresh deals or firm offers reported.”

Price assessments

- US-origin bulk HMS 80:20: $401/t CFR Turkiye, down by $1/t w-o-w

- US East Coast HMS 80:20: $372/t FOB, up $2/t w-o-w

The scrap-to-rebar spread widened to around $195-196/t, with rebar export offers at $595-605/t FOB, continuing to keep mill margins under pressure.

Market comments

Trading activity in Turkiye’s import scrap market came to a near standstill following active bookings in late March, when mills secured multiple cargoes. With inventories relatively comfortable, mills shifted focus toward evaluating finished steel sales before committing to fresh scrap purchases.

A Baltic origin trader source reported “European offers around $395/t, with limited buying interest amid weak activity. Mills, already covered for April-May after booking 35-40 cargoes, are pressuring scrap prices and shifting toward cheaper Chinese billets, while domestic rebar prices softened by $5-10/t w-o-w.”

A Turkiye based mill source stated “Producers are currently testing rebar export markets and monitoring order flows to determine raw material requirements. This cautious approach, combined with geopolitical uncertainty, has kept both buyers and sellers largely inactive.”

Another market participant stated that most participants are reluctant to take positions at current levels, preferring clearer direction on freight, energy costs, and geopolitical developments before re-entering the market.

Mills continued to offer rebar at around $595-605/t FOB but struggled to secure sufficient orders due to cautious buyer sentiment.

Domestic steel market

Turkiye’s domestic steel market remained subdued, with rebar demand staying weak both locally and in export channels. Producers prioritised finished steel sales over raw material procurement, aiming to improve margins amid high input costs.

As per market insiders, although a potential easing in geopolitical tensions could support downstream demand, current market conditions remain fragile, with limited visibility on near-term recovery.

Outlook

Turkish scrap prices are likely to remain muted in the coming days, with mills covered for till April end and some for early- May and focused on finished steel sales. Market direction will depend on renewed geopolitical developments like how-long the ceisefire is sustaining, trends in freight changes and recovery in rebar demand, while cheaper billet options may cap upside.

Leave a Reply