- Pilbara recovery lifts volumes; Brazil sustains momentum

- Improved throughput offset by persistent logistical bottlenecks

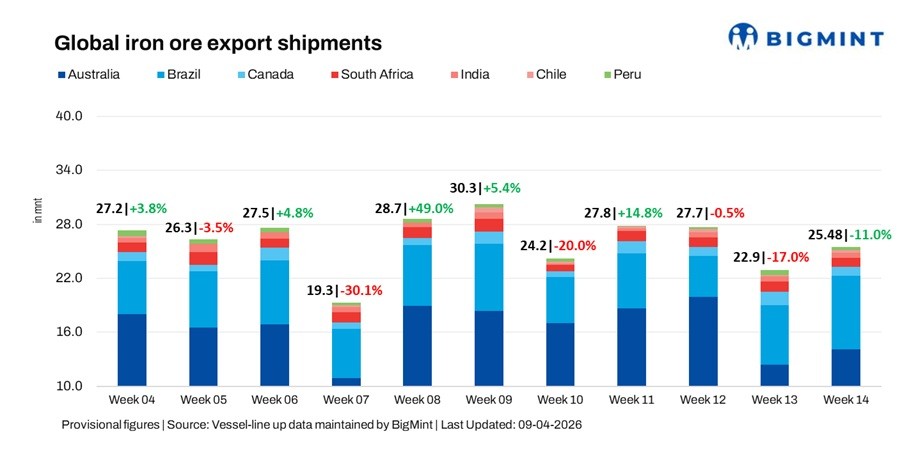

Global iron ore export shipments rose 11% w-o-w to 25.48 million tonnes (mnt) in the week ended 3 April, from 22.95 mnt a week earlier, according to BigMint data. The recovery was led by Australia as cyclone disruptions eased and port operations normalised, while Brazil maintained steady loading momentum. However, flows from Canada, South Africa and Peru remained constrained, with India and Chile showing stable to improved activity.

Country-wise trends

Port & shipper-wise trends

- Australia: Port Hedland handled 9.38 mnt, Walcott 2.35 mnt, and Dampier 1.97 mnt. BHP exported 5.73 mnt, Rio Tinto 4.32 mnt, and FMG 3.14 mnt, with China absorbing 11.62 mnt.

- Brazil: Ponta da Madeira shipped 3.27 mnt and Itaguai 2.09 mnt. Vale exported 4.30 mnt, while CSN shipped 2.84 mnt, with China importing 4.37 mnt.

- Canada: Sept-Iles shipped 0.62 mnt and Port Cartier 0.38 mnt, with IOC exporting 0.42 mnt and AMNS 0.38 mnt, while the Netherlands received 0.36 mnt.

- South Africa: Saldanha handled 1.02 mnt, with Slovenia and India each receiving 0.18 mnt.

- India: Dhamra shipped 0.31 mnt and Paradip 0.12 mnt, with Rungta Sons exporting 0.24 mnt and China importing 0.24 mnt.

- Chile: Totoralillo shipped 0.25 mnt, with China importing 0.25 mnt.

- Peru: San Nicolas shipped 0.36 mnt, with Shougang Hierro exporting 0.36 mnt and South Korea importing 0.18 mnt.

Bulk iron ore freights show mixed trend

Dry bulk iron ore freight rates showed a mixed trend w-o-w, with gains on select routes supported by improved cargo availability from Australia and Brazil. The Pacific saw some recovery as Australian volumes picked up, while the Atlantic remained balanced on steady Brazil loadings. However, sentiment stayed cautious amid muted fixtures, ample vessel supply and bunker volatility.

Outlook

Iron ore shipments are likely to remain supported as operations normalise in Australia and steady Brazil throughput aids flows. However, persistent rail and logistical constraints in regions like South Africa and Canada may keep movements uneven. Freight sentiment is expected to stay mixed, with cargo support offset by vessel oversupply and bunker volatility.

Leave a Reply