- Prices in key eastern markets rise around 5% m-o-m

- Surge in imported scrap prices triggers uptick in exports

In March 2026, India’s sponge iron market witnessed a notable uptick, supported by expectations of tighter raw material availability. Escalating geopolitical tensions in the Middle East intensified concerns over rising imported coal and freight costs, prompting producers to raise offers to safeguard margins. As a result, pan-India sponge iron prices increased by INR 150-1,800/t ($1-19/t) m-o-m, reflecting a cost-driven uptrend with regional variations in demand and supply dynamics.

Regional market dynamics

Eastern region

Sponge iron prices in key eastern Indian markets such as Durgapur and Rourkela increased by approximately 5% m-o-m, reflecting a moderately positive trend in March. The uptrend was supported by firm input costs, particularly pellets and non-coking coal, along with improving export activity and substitution demand.

In Durgapur, prices rose from around INR 25,600/t to INR 27,200/t (up INR 1,600/t), driven by strong export bookings to Nepal and limited seller availability, which kept offers firm. Meanwhile, Rourkela witnessed a more volatile trend, with prices fluctuating in the range of INR 27,000-28,300/t, marking an increase of around INR 1,300/t, influenced by firm coal costs and intermittent corrections.

Coal dynamics remained a key factor, with most producers relying on domestic sources such as MCL and Raniganj, while imported coal remained largely unviable. Additionally, higher imported scrap prices and limited availability supported sponge iron demand. Logistics challenges, including elevated freight rates and intermittent rake availability, also impacted trade flows. Overall, the eastern region maintained a firm-to-stable tone, supported by cost pressures, export demand, and steady consumption.

Northern region

On a m-o-m basis, sponge iron prices in Mandi Gobindgarh increased by approximately INR 900/t in March. The primary driver was tightening scrap availability, as imports declined amid geopolitical tensions.

Induction furnace (IF) manufacturers adjusted their scrap-to-sponge consumption ratio from 75:25 to around 70:30, increasing reliance on sponge iron. Supply constraints were further aggravated by limited transportation availability. Since sponge iron in this region is largely sourced from Odisha, freight costs of around INR 4,000-4,200/t significantly increased landed costs, thereby supporting the upward price movement.

Southern region

Sponge iron prices in the south increased by around INR 1,500/t (~5%) m-o-m, primarily driven by rising raw material costs linked to the ongoing West Asia conflict.

Key inputs such as coal and melting scrap became more expensive due to logistical disruptions and tight supply conditions. The shortage of melting scrap, a key substitute, further supported sponge iron demand as buyers shifted partially toward DRI.

During mid-March, the market faced competitive pressure as eastern-based mills offered material at relatively lower prices in south India. Despite this, firm input costs, including iron ore, pellets, and coal, sustained upward pressure on prices.

On the raw material front, non-coking coal prices surged by ~18% (~INR 2,000/t) to around INR 11,750/t ex-port, significantly impacting production costs, while pellet prices remained relatively stable. Notably, conversion margins improved by 20-25% m-o-m, allowing producers to offset earlier losses.

Central region

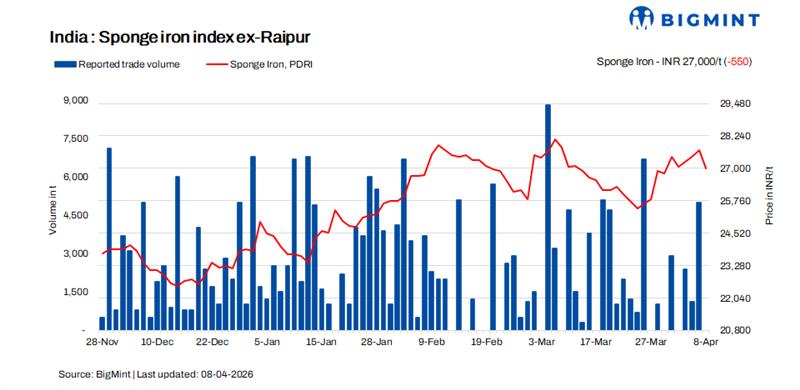

Pellet-based sponge iron prices in Raipur and Raigarh (Chhattisgarh) surged sharply by INR 1,800-2,000/t exw following escalating geopolitical tensions.

Prices in Raipur increased from INR 25,600-25,700/t to INR 27,500/t exw, while in Raigarh prices rose from INR 25,200-25,300/t to INR 27,200/t exw in early March. The spike was driven by panic buying and stockpiling, as buyers anticipated supply disruptions and further cost escalation.

However, as the month progressed, price volatility and inconsistent buying patterns emerged. With the financial year-end approaching, procurement slowed, resulting in a price correction of around INR 700/t exw by month-end.

From a cost perspective, producers in Chhattisgarh primarily rely on domestic coal, which cushions them from global shocks. However, the use of a blended coal mix (60-70% domestic and 30-40% imported) means rising imported coal prices still had a moderate impact on production costs.

DRI exports

Amid volatile global sentiments and tightening scrap availability, a sharp rise in imported scrap prices encouraged overseas buyers to shift toward Indian sponge iron (DRI). Export bookings surged by approximately 63% m-o-m, reaching around 45,000 t for Nepal and Bangladesh. This was primarily driven by cost competitiveness of DRI compared to scrap.

Although export offers fluctuated in line with market trends, the overall price trajectory remained positive. DRI export prices increased by around $8/t m-o-m, settling at $346/t CPT Raxaul (Nepal) and $359/t CPT Benapole (Bangladesh).

Outlook

The Indian sponge iron market is expected to remain firm in the near term, supported by elevated input costs, geopolitical uncertainties, and sustained export interest. Rising coal prices and freight volatility are likely to keep cost pressures intact, limiting any sharp downside in prices.

However, demand from the finished steel segment and financial liquidity conditions will play a crucial role in determining buying momentum.

Leave a Reply