- Improved inflows weigh on domestic prices

- Finished steel weakness adds pressure

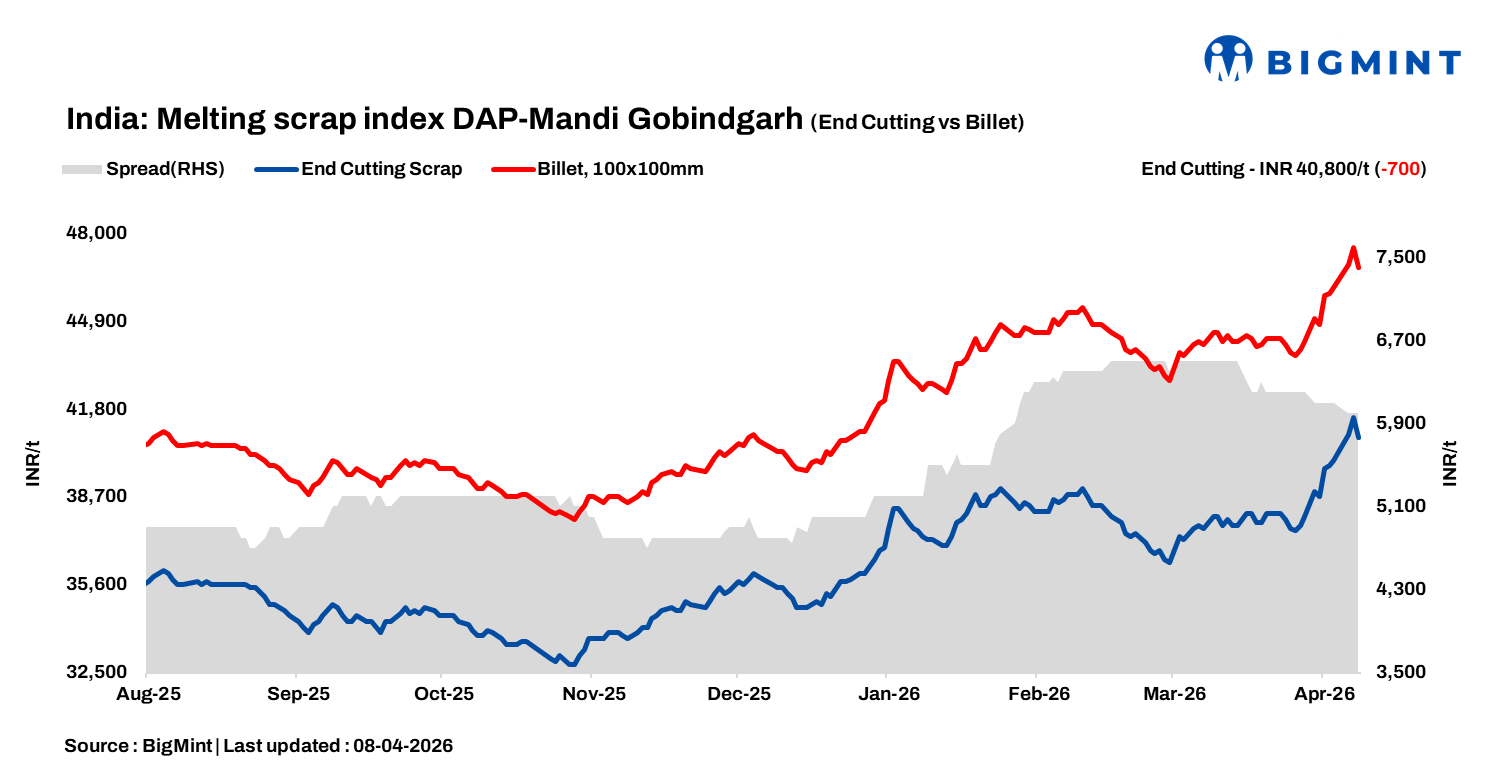

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, declined by INR 700/tonne (t) d-o-d to INR 40,800/t DAP on 8 April 2026. Market activity remained largely subdued, as sentiment turned cautious following the sharp price increases observed in recent sessions. Scrap prices fell by INR 700-1,200/t d-o-d amid weak buying interest.

Improved inflows pressure scrap prices

Scrap inflows from neighbouring regions, including Uttar Pradesh, Delhi, and Haryana, resumed after recent disruptions, leading to improved material availability. Suppliers, aligning with lower bids from Mandi-based mills, offered material at compressed margins. However, mills largely refrained from aggressive bookings, maintaining a conservative procurement strategy amid uncertain near-term market direction.

A mill owner informed BigMint, “Buyers have largely adopted a wait-and-watch approach, anticipating a potential correction of around INR 1,000-1,500/t following the recent ceasefire announcement. Meanwhile, most sellers have already liquidated inventories and are not under pressure to offload material, keeping overall trading activity limited.”

Raw material prices

In the key hub of Mandi Gobindgarh, sponge iron prices declined by INR 700/t d-o-d to INR 34,600/t DAP. Similarly, steel-grade pig iron prices in Ludhiana dropped by INR 800/t to INR 43,200/t DAP, reflecting weaker sentiment across the metallics segment.

Steel market dynamics

Ingot prices in Mandi Gobindgarh declined by INR 700/t d-o-d to INR 46,800/t DAP, weighed down by reduced transaction volumes and cautious buying activity. Across other key production centres, ingot prices also softened by INR 400-1,200/t d-o-d, reflecting a broader correction in the semi-finished steel segment.

Rebar (Fe500) prices in Mandi eased by INR 300/t to INR 53,000/t, amid moderate to weak trade conditions and limited buying interest.

Overview of Jalna market

In the western India-based Jalna market, HMS (80:20) scrap prices declined by INR 1,000/t d-o-d to INR 34,000/t, while billet prices fell by INR 500/t to INR 47,000/t. Meanwhile, rebar prices remained stable at INR 54,300/t. The recent US-Iran ceasefire announcement has triggered a sharp shift in market sentiment. Scrap suppliers, who were earlier holding material in anticipation of further price increases, have now entered panic selling mode, releasing material into the market. This has led to improved scrap availability and increased bookings, resulting in a sharp correction in scrap prices during today’s trading session.

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 5,800-6,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $382-$384/t, approximately INR 37,744/t (inclusive of freight). HMS (80:20) prices in Mumbai fell by INR 400/t to INR 36,100/t DAP. Indicative prices of shredded from Europe stood at $402-$405/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 15,900/t.

Leave a Reply