- Longs segment supported by steady bookings

- Export market subdued amid elevated freights

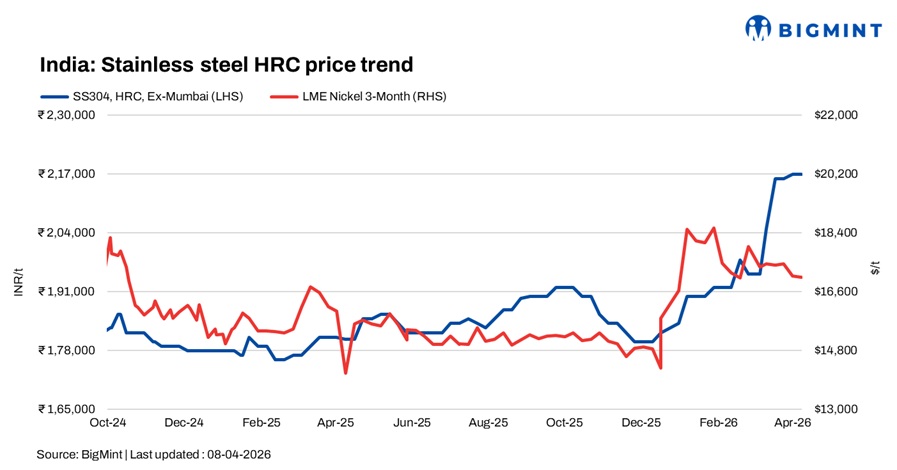

India’s stainless steel market showed a divergent trend in the week ended 8 April 2026, with the flats segment losing steam after a recent rally, while longs maintained firm momentum. Sentiment softened following the US-Iran ceasefire announcement, prompting cautious participation and triggering expectations of a near-term price correction, particularly in flats.

Flats segment faces demand resistance

The finished flats market remained largely stable, as subdued demand and buyer hesitation restricted fresh transactions. Market participants largely stayed on the sidelines, anticipating a correction after the recent uptrend. BigMint’s benchmark 304 HRC remained unchanged at INR 217,000/t ex-Mumbai, while 316 HRC remained stable at INR 375,000/t.

Policy developments added complexity to the market. The temporary BIS exemption for select stainless steel flat imports until September 2026 is expected to ease raw material availability for downstream players. Meanwhile, a leading domestic producer continues to rely on imported slabs, supported by strategic tie-ups with Indonesian players. The company is also shifting production dynamics by commissioning a blast furnace in Odisha to produce 200 and 400 series, reducing reliance on EAF-based output.

Longs segment outperforms on better demand

In contrast, the longs segment witnessed stronger traction, backed by consistent bookings and relatively healthy end-user demand. 304L black round bars surged by INR 7,000/t w-o-w to INR 185,000/t ex-Mumbai, while 316L prices held steady at INR 310,000/t. Mills reported improved sales volumes, indicating better consumption trends compared to flats.

Export market subdued amid elevated freights

India’s export market remained subdued due to elevated freight rates and geopolitical uncertainties, limiting overseas bookings. Meanwhile, fresh price hikes by major producers such as POSCO and Nippon Steel reflected sustained cost pressures from raw materials and currency fluctuations. Additionally, China’s stainless steel market continued to face volatility amid high production levels, elevated inventories, and weak real estate demand, capping global upside.

Raw material scenario

Outlook

The near-term outlook remains uncertain. While cost support and firm longs demand may prevent a sharp correction, weak flats demand and cautious buyer sentiment are likely to keep the market bound to a narrow range. Procurement is expected to remain need-based until clearer demand signals emerge.

Leave a Reply