- Energy prices to ease as ceasefire removes immediate supply disruption risk

- Coal prices to stay supported due to tight supply, strong market price floors

The overnight news of a two-week US-Iran ceasefire and the reopening of the Strait of Hormuz is the most consequential energy market development since the escalation began. It removes the immediate “armageddon” scenario that had thrown oil, gas, and freight markets into turmoil.

However, it does not resolve the underlying drivers of higher coal prices: collapsing Russian production, depleted European inventories, and a Chinese market that is seasonally soft but structurally dependent on seaborne imports for any demand recovery.

Immediate impact of ceasefire

Cheaper oil

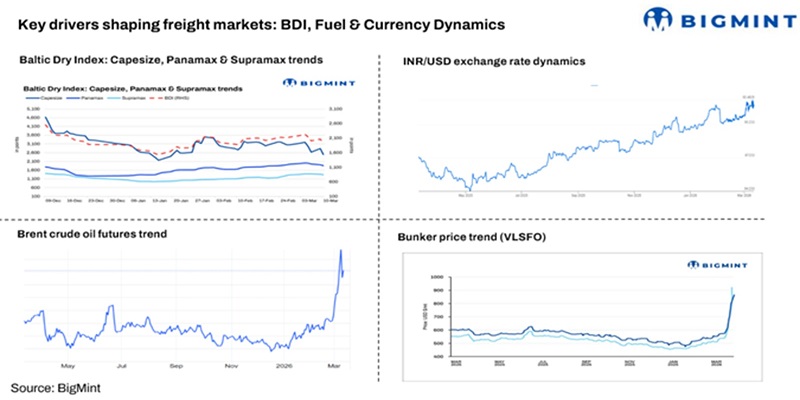

Pre-ceasefire data showed Brent at $110/barrel (bbl), within $2/bbl of its 19 March peak of $112.10/bbl. That $110/bbl price included a significant risk premium tied specifically to Hormuz. Oil traders were pricing in a non-trivial probability of a supply shock — either through a direct closure of the Strait or through Iranian retaliation against Gulf infrastructure. With the Strait reopening, that premium unwinds. Not entirely — the ceasefire is only two weeks, and the conflict remains unresolved — but the immediate, acute risk is gone.

Brent falls $10-12/bbl in the first 48 hours, trading into the $95-100/bbl range. A return to $80-90/bbl would require evidence that the ceasefire will extend or that Iranian exports resume fully.

Cheaper gas (TTF and LNG)

The gas market impact is more layered. Pre-ceasefire data already showed contradictions: Title Transfer Facility (TTF) — the leading European benchmark for wholesale natural gas — was at EUR 53.50/MWh (up 4.5%) despite warm weather and EU gas storage at just 28.4% of capacity, well below last year’s 35%. The only explanation was the Hormuz risk premium embedded in LNG supply expectations. Over the past five days, Persian Gulf LNG exports had fallen to just 30,000 tonnes (t) per day, down from 60,000 t a week ago and a staggering 88% below the 2025 daily average of 250,000 t.

That number is likely to normalise towards the 250,000-t daily average over the coming week as vessels resume normal routing. Qatari and UAE LNG will once again compete directly with US and Nigerian cargoes into both Europe and Northeast Asia.

The TTF May contract will fall EUR 3-5/MWh to EUR 48-50/MWh. Northeast Asia LNG spot falls $1.50-2.50/MMBtu to $16-17/MMBtu. The May LNG contract to Northwestern Europe, stable at $16.50 pre-ceasefire, will likely test $15 in the coming days.

Cheaper freights

Pre-ceasefire data show that rates on most international freight routes dropped. That trend will accelerate. However, the key variable is not published freight rates – it is war risk insurance premiums.

Every vessel transiting the Strait of Hormuz, Gulf of Oman, or Arabian Sea was carrying elevated marine insurance costs. These are embedded in freights for oil tankers, LNG carriers, and dry bulk ships. The ceasefire removes those premiums for its duration. Gulf-to-Asia routes will see the largest decline (5-10%). Dry bulk coal routes from South Africa and Indonesia will see a smaller but meaningful reduction, as regional risk assessments improve.

The coal market: Why the impact is muted

Here is the crucial insight. While oil and gas fall meaningfully, coal prices change far less. The pre-ceasefire data explains why.

First, Russian supply is physically constrained, not geopolitically. Russian coal production was at 34.4 million tonnes (mnt) in February, down 5% y-o-y. Over January-February, thermal coal production plunged 11% to 31.4 mnt. Anthracite — a speciality product with few substitutes — collapsed 20%. A two-week ceasefire does not fix broken mining equipment, Western sanctions on spare parts, or the slow deterioration of Russia’s rail network.

Second, Chinese demand is seasonally soft and does not need imports. Coal usage at China’s top 6 thermal power plants fell to 740,000 t on 7 April, down 6% w-o-w and 2.4% y-o-y. That is 1.5% below the seasonal average. Stocks at Bohai Sea fell to 18 mnt, down 4.5% y-o-y. The domestic Chinese market is stable at RMB 760/t ($111/t). There is no urgent import requirement.

Third, the arbitrage hierarchy preserves Russia’s advantage. Russian mid-CV coal remains the most competitive origin to China at a staggering $25.3/t discount to domestic Chinese coal. Indonesian mid-CV is second at a $3.4/t discount. Australia has moved from an $8/t premium in early March to parity. South African and Colombian are excluded at premiums of $27/t and $39/t, respectively.

Lower oil, gas, and freight reduce delivered costs for all origins equally. Russia’s relative advantage remains intact. The only second-order effect is if lower energy prices reduce Chinese domestic coal production costs (most Chinese mines are diesel-intensive), potentially lowering the RMB 760/t ($111/t) benchmark and making seaborne imports marginally less competitive.

Fourth, the Indian value-in-use band creates a floor. Indonesian 4200 GAR, Indonesian 5900 GAR, and Russian 5500 NAR are neck and neck in a range of INR 1,750-1,850 per Gkal, up INR 30/t w-o-w. That is a technical floor. Any material priced below this band finds immediate Indian offtake. Any material above it does not.

The counterintuitive winners: South Africa and ARA storage

Two anomalies emerge from the ceasefire analysis.

South Africa becomes more interesting, not less. South African thermal coal exports rose 12% y-o-y in February to 6.2 mnt, bang on forecast. Shipments to India jumped to 3.3 mnt in February, up from 1.9 mnt a year earlier. Exports to Pakistan more than doubled to 1.2 mnt over January-February.

South African coal does not transit Hormuz. It moves through the Indian Ocean on predictable routes. Pre-ceasefire, it was excluded from the Chinese arbitrage at a $27/t premium — too expensive when Russian coal was $25/t cheaper. But with the ceasefire pulling oil, gas, and freight lower, South Africa’s relative position improves. It remains a premium origin, but the premium narrows. And for buyers who cannot or will not take Russian coal, South Africa is now the most reliable alternative.

The forecast for South African exports has already been increased to 39.4 mnt for the first half of 2026, up from 35.7 mnt in the same period of 2025. The ceasefire does not change that forecast — it validates it.

ARA storage remains a problem that the ceasefire does not solve. Coal inventories at Europe’s Amsterdam, Rotterdam, Antwerp (ARA) terminals stood at 2.5 mnt as of 6 April, up 5% w-o-w but still 29.4% lower y-o-y. More strikingly, stocks are 44% below the April average since 2021. South African coal still does not price into ARA at current levels. Physical prices would need to rise significantly to see meaningful supply from anywhere except Kazakhstan heading to Europe.

The ceasefire does not refill those caverns. And with Western Europe facing unseasonably high temperatures (27-28°C) pointing to another dry, hot summer, the risk of a coal supply crunch in Europe later in 2025 remains entirely intact.

The two-week countdown: What to watch

The pre-ceasefire price forecast was “neutral short term, positive medium term” for both coal FOB and LNG Northeast Asia. The ceasefire does not change that forecast.

Short term (next 14 days): Oil and gas prices fall as the Hormuz risk premium unwinds. Freight rates drop further, particularly on Gulf-Asia routes. Coal prices are flat to marginally lower, but the $25.3/t Russian discount to China and the INR 1,750-1,850/Gkal Indian value-in-use band act as technical floors. BigMint expects FOB NEWC 6000 to test $135-137/t (from $140/t pre-ceasefire) and FOB RBay 6000 to test $104-106/t (from $108.50/t).

Medium term (post-ceasefire, regardless of outcome): The positive outlook remains. Russian coal production is in structural decline — down 11% for thermal coal in January-February. European ARA inventories are 44% below the 2021-2025 April average. Even with the Strait open, the physical supply deficit does not disappear. If the ceasefire holds beyond two weeks, the downward pressure on oil and gas continues, but coal finds a floor. If the ceasefire collapses, all pre-ceasefire risk premiums return instantly and likely overshoot, because the market will have just experienced a false reprieve.

Leave a Reply