- Crude steel production up 10.5% y-o-y to 168 mnt

- Limited domestic supply sustains import dependence

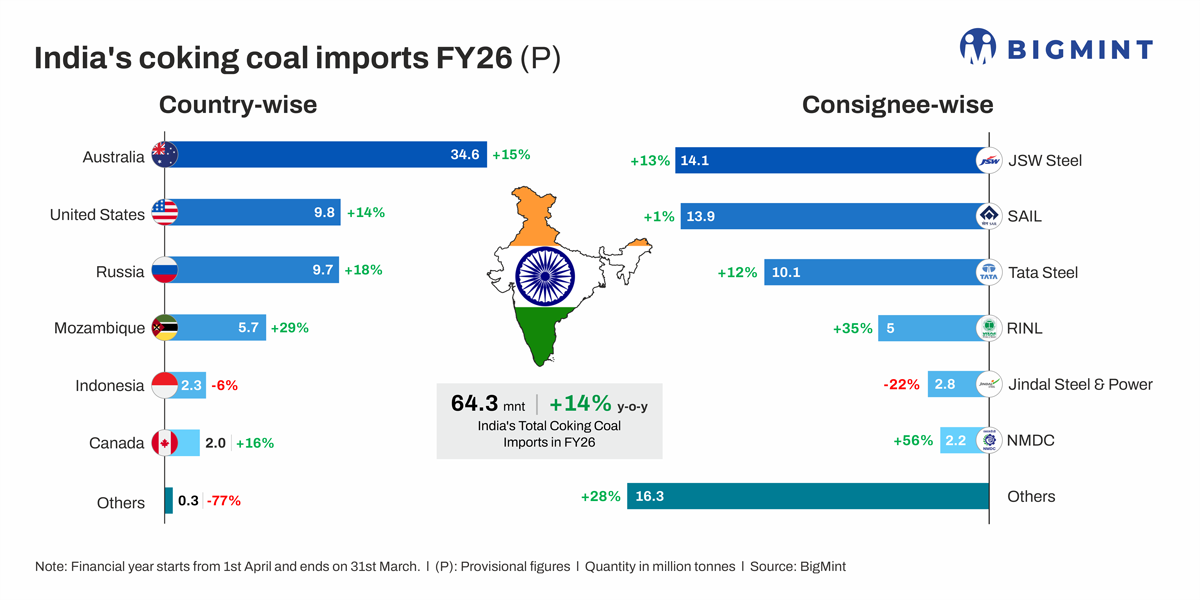

India’s coking coal imports increased to 64.31 million tonnes (mnt) in FY’26, registering a 13.5% y-o-y growth compared with 56.65 million tonnes (mnt) in FY’25. The rise in imports reflects strong domestic steel production, higher blast furnace utilisation, and limited availability of high-quality domestic coking coal.

Despite ongoing efforts to enhance domestic production, Indian steelmakers continue to depend heavily on imported coking coal to maintain the required coke quality for blast furnace operations.

Country-wise imports: Australia retains leadership

Australia retained its position as India’s largest coking coal supplier, with shipments rising to 34.65 mnt in FY’26 from 30.22 mnt in FY’25, registering a 14.6% y-o-y increase. The country accounted for over 50% of India’s total imports, supported by long-term supply contracts and the availability of premium hard coking coal suitable for blast furnace operations.

Other key suppliers also recorded notable growth:

- United States: Imports increased to 9.79 mnt in FY’26 from 8.58 mnt (+14.1% y-o-y).

- Russia: Shipments climbed to 9.7 mnt from 8.23 mnt (+17.9%), aided by competitive pricing and shorter shipping routes.

- Mozambique: Imports rose sharply to 5.65 mnt from 4.38 mnt (+29.2%).

- Canada: Shipments increased to 1.96 mnt from 1.69 mnt (+15.6%).

This trend highlights India’s increasing diversification of supply sources, although Australia continues to dominate the import basket.

JSW Steel top buyer

India’s coking coal imports in FY’26 were largely driven by large integrated steel producers, which depend heavily on imported premium metallurgical coal to support blast furnace operations. Among the major importers, JSW Steel emerged as the largest buyer, importing 14.11 mnt during the fiscal year, closely followed by SAIL with 13.87 mnt and Tata Steel with 10.11 mnt.

Other significant importers included RINL, which procured 4.99 mnt, Jindal Steel with 2.76 mnt, and NMDC with 2.2 mnt. Meanwhile, other smaller consumers and traders collectively accounted for around 16.27 mnt of imports.

The strong procurement by these companies reflects higher crude steel production, improved blast furnace utilisation rates, and sustained demand from infrastructure and manufacturing sectors, which continued to drive the need for imported high-grade coking coal.

Higher crude steel output – Crude steel production in India increased by 10.5% y-o-y to 168 mnt in FY’26, marking continued capacity-led growth, albeit at a more measured pace compared to the sharper expansion seen in the previous fiscal.

Domestic coking coal production remains limited – Domestic coking coal production declined marginally by 2.3% y-o-y to 65 mnt, while imports increased by 9.1% y-o-y to 84 mnt. The rise in imports reflects the need to support higher steel output amid limited domestic availability, reinforcing Indias structural dependence on imported coking coal.

Among the producing entities, BCCL remained the largest contributor, producing 29.48 mnt, although this was lower than 34.82 mnt in the same period last year. CCL registered an increase in output, reaching 17.88 mnt compared with 16.49 mnt in FY’25.

Production from ECL rose to 1.28 mnt in FY’26, up sharply from 0.02 mnt a year earlier, while SECL produced 0.21 mnt, largely stable y-o-y. Output from captive mines increased to 0.95 mnt from 0.41 mnt, while other sources collectively contributed around 6 mnt during the period.

Despite these contributions, a significant share of domestic coking coal remains medium- to low-grade, requiring blending with imported premium hard coking coal to maintain coke quality for blast furnace operations. As a result, India continues to rely heavily on imports to meet the quality requirements of its expanding steel sector.

Outlook

India’s coking coal imports are likely to remain strong, supported by rising steel capacity and infrastructure-led demand. However, growth may moderate if domestic production improves and coal beneficiation expands, while global prices, freight rates, and supply from Australia and Russia will continue to shape import trends. Overall, India is expected to remain a major coking coal importer due to limited domestic availability of high-grade coal.

Leave a Reply