- Prices rise on high input costs, tight supply

- Good demand keeps inventories low, supports prices

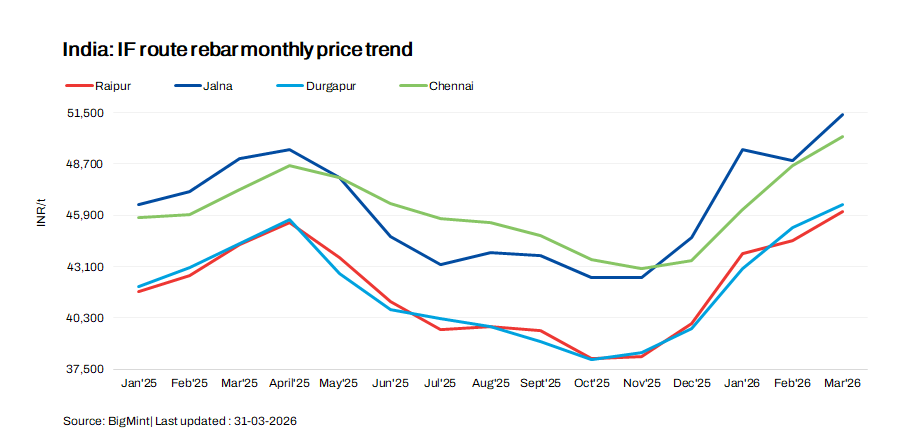

IF-route rebar prices maintained a firm upward trajectory in March 2026, increasing by INR 1,600-6,800/t m-o-m across regions, as per BigMint’s assessment. Buying activity stayed healthy to moderate throughout the month, with consistent participation from buyers. Sustained price gains were observed across markets, which strengthened sentiment and kept overall trading momentum active and engaging. The key driver behind this trend was the tight supply of raw materials, particularly scrap and sponge iron, further intensified by war-led uncertainties and geopolitical tensions, which kept input costs elevated and reinforced the overall upward momentum in rebar prices.

On the raw material front, sponge iron and billet prices witnessed a firm to upward trend during the month, supported by improved demand from the finished steel segment. Buying activity remained good to moderate, with market participants actively engaging in procurement. Tight availability of raw material such as scrap and sponge in select regions further supported prices, restricting any major corrections and keeping the overall sentiment positive.

Mill inventory levels remained around 8-10 days, indicating balanced buying activity and steady lifting in the market. However, towards the end of the month, transportation disruptions were observed in certain regions due to petroleum-related restrictions, which impacted material movement and affected overall lifting.

As per Joint Plant Committee (JPC) data, India’s rebar production through the IF and BF routes stood at 48.7 million tonnes (mnt) in April-February of FY’26, marking a significant 9.03% rise from around 44.3 mnt in the same period of FY’25.

Region-wise price movements

Raw material prices trend: In line with the volatility seen in the finished steel market, key raw materials such as billets and sponge iron also followed a mixed-to-firm trajectory during the month. Prices witnessed an initial uptrend driven by rising input costs particularly sponge iron and coal followed by a partial correction mid-month. Despite some fluctuations, elevated cost pressures, including concerns over imported coal and freight amid geopolitical tensions, prompted producers to keep offers firm, thereby sustaining a seller-driven market sentiment.

Considering Raipur as the benchmark, billet prices increased by INR 1,650/t m-o-m to INR 43,150/t ex-works, while sponge iron (PDRI FeM 80% ±1) prices witnessed a marginal decline of around INR 50/t m-o-m to INR 27,450/t ex-works. Despite the slight correction in sponge iron prices, overall market sentiment remained positive, as improved procurement at relatively lower levels supported buying activity. Post mid-month, sponge iron prices also began to show an upward trend, aligning with the broader firm sentiment in the market.

BF-rebar sentiment

Trade-level BF rebar prices rose by INR 1,100/t m-o-m to ~INR 59,800/t ex-Mumbai in March 2026, with higher prices dampening buying activity as participants turned cautious. In early April, primary steelmakers increased list prices by up to INR 2,000/t, pushing levels to between INR 60,000–61,000/t (landed), while trade prices edged up to about INR 60,600/t ex-Mumbai. The uptrend was supported by a sharp 20–25% decline in mill inventories amid strong dispatches and healthy order inflows, with project deals largely executed in the INR 59,500–60,000/t range.

Outlook

April–May marks the peak construction season, typically driving a strong uptick in steel demand, supported by pre-monsoon bookings as buyers secure material ahead of potential logistical disruptions. This seasonal momentum is likely to keep demand firm and support prices in the near term. However, ongoing geopolitical tensions and war-related developments remain a key watchpoint, with potential impacts on raw material availability, input costs, and overall steel price trends.

Leave a Reply