- Fiscal year-end buying, too, supports price uptrend

- Firm raw material costs sustain producer realisations

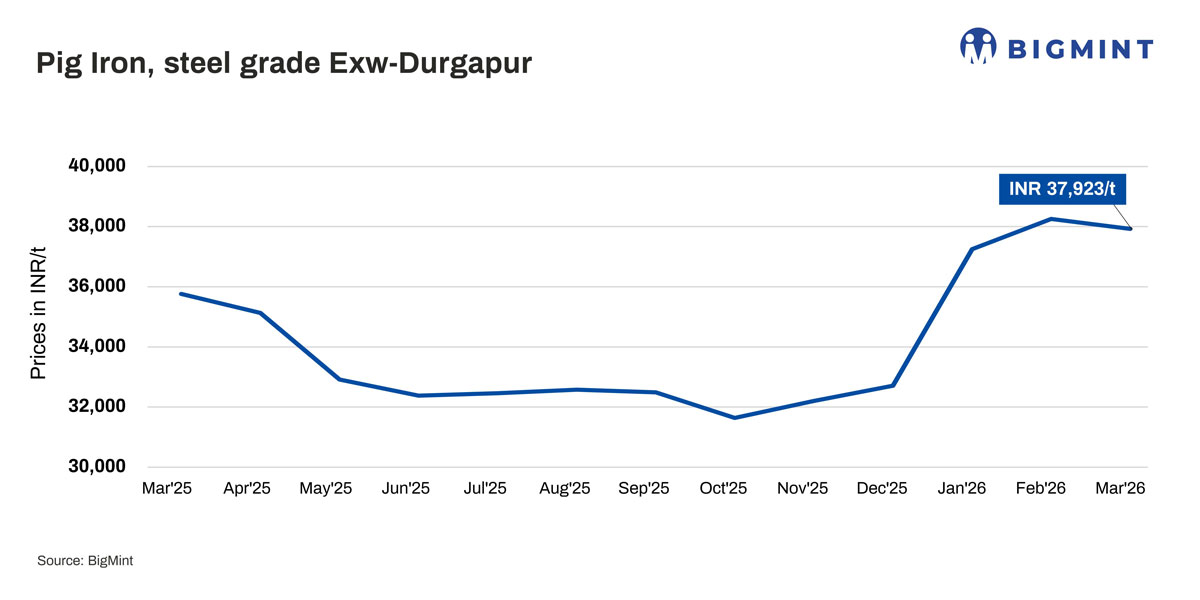

Pig iron prices recorded a moderately positive trend in March 2026, supported by firm raw material costs, improved sentiment, and financial year-end buying. Steel-grade pig iron prices in Durgapur increased from around INR 38,000/t to INR 39,400/t exw, marking a m-o-m rise of INR 1,400/t. Market activity remained largely need-based, though steady enquiries and stock replenishment supported price momentum.

Raw material cost pressure elevated

Input cost pressures persisted during the month, lending firm support to pig iron prices. Met coke prices increased by around INR 1,000/t m-o-m to INR 36,000/t, while coking coal prices rose to nearly $263/t from $250/t, up $13/t. Supply constraints, vessel delays, and elevated freight rates further tightened availability, keeping production costs elevated and supporting higher offer levels.

Auction trends reflect improving yet selective participation

Auction activity during March remained dynamic, with multiple auctions conducted by NMDC and SAIL. Early-month NMDC auctions witnessed strong bookings with full offtake at INR 36,150/t, while participation turned selective in mid-month, with lower volumes booked. However, sentiment improved toward month-end, with NMDC and SAIL-RSP auctions achieving higher realisations up to INR 39,850/t, indicating better buyer confidence and gradual market strengthening.

Substitute metallics and scrap dynamics support demand

Pig iron remained competitive against substitutes during the month. End-cutting scrap prices increased to around INR 38,200/t from INR 36,700/t, while PDRI rose to nearly INR 27,200/t from INR 25,600/t. The relatively narrow spread with scrap and firm sponge iron prices limited substitution, while tight scrap availability encouraged partial shift toward pig iron, supporting consumption levels.

Durgapur sees selective activity, exports gain traction

The Durgapur market witnessed selective but steady activity, with a prominent eastern region player procuring around 20,000 t of pig iron at INR 37,500-38,000/t, indicating continued bulk transactions. Capacity additions in the Kharagpur and Jamuria belts improved regional supply dynamics, although spot availability in Durgapur remained limited with only selective offers, while Kharagpur saw relatively active selling interest.

At the same time, export activity remained firm, providing additional support to the market. Around 1–2 cargoes of 50,000-60,000 t each were concluded to the US and Europe at $380-420/t FOB, reflecting competitive Indian pricing in the global market. Ongoing negotiations for fresh shipments indicate sustained overseas demand, which continues to complement domestic consumption and support overall market sentiment.

Production remains broadly stable y-o-y

Production trends remained largely stable over the past year, reflecting a balanced supply environment. Monthly output averaged nearly 0.70 mnt in 2025, with production ranging between 0.62 mnt (February) and a peak of 0.76 mnt (May), indicating moderate fluctuations aligned with demand cycles and operational adjustments at mills. Output remained largely steady in the second half of the year, hovering in the range of 0.65-0.70 mnt, suggesting controlled supply-side discipline.

In early 2026, production continued to follow a similar trend. Output stood at 0.69 mnt in January and eased slightly to 0.68 mnt in February (down ~1% m-o-m), indicating marginal moderation rather than any structural decline. On a y-o-y basis, February production showed an improvement compared with 0.62 mnt in February 2025, reflecting better utilisation levels. Overall, the data indicates stable production with no signs of oversupply, supporting price stability amid evolving demand conditions.

Market trends through Mar’26

The market witnessed strong activity in early March, supported by proactive buying and restocking. Mid-month, trading activity normalised amid cost pressures, while sentiment improved again toward month-end due to financial year closing and stabilising external factors. Overall, the market remained resilient with a cautiously positive undertone.

Outlook

Pig iron prices are expected to remain stable to slightly firm in the near term, supported by elevated raw material costs and improving export opportunities. Geopolitical developments may continue to influence global coal markets and freight, potentially sustaining input cost pressure. However, buying activity is likely to remain largely need-based, keeping price movements measured.

Leave a Reply