- Tighter supply from maintenance may lift coke prices

- Rising hot metal output to support demand growth

Mysteel Global: The prospect for China’s metallurgical coke market in April turns optimistic, with potential supply disruptions offering new support after a short-lived pessimism developed due to steelmakers boycott of higher coke prices, Mysteel predicts in its latest monthly report.

Mysteel has learned from sources that several coke plants in North China’s Shanxi province have scheduled facility maintenance this month, which could tighten supplies of this feed material to Tangshan city, the country’s top steelmaking hub in North China’s Hebei province.

The actual implementation of the maintenance plan, however, will also depend on the profitability of local coke producers going forward. They may postpone the maintenance plan and keep steady operations if their profit margins improve, the report points out.

Mysteel’s historical data over 2022-24 indicate that April typically recorded the lowest coke output of the year, but the low point for 2025 occurred earlier in mid-March, which coincided with the severe losses most coke producers suffered after 11 consecutive rounds of price cuts, totalling Yuan 505-605/tonne ($73-88/t), took effect.

Sources disclosed that many coke producers are still suffering heavy financial burdens due to the elevated coking coal prices as well as other operational costs. The profitability situation is particularly challenging for those without coke oven byproduct plants, as other producers could still offset some losses with rising revenue from chemical byproducts.

For this month, tailwinds seem ready for pushing met coke prices higher. China’s hot metal production has gathered pace this week, signaling that mills’ demand for coke may continue to improve in April. The daily hot metal output of the 247 Chinese blast-furnace steel mills that Mysteel surveys increased for the third consecutive week to average 2.37 million tonnes/day over March 27-April 2.

In mid – or late April, the daily hot metal output level is expected to climb above 2.4 million t/d, a key threshold widely deemed by participants to effectively boost demand for raw materials, according to the report.

In parallel, support from the cost side could largely stay steady for the coke market this month, despite possible fluctuations in coking coal prices and an erratic outlook for the Middle East conflicts. It’s noteworthy that global oil prices soared again yesterday amid more signs of escalating tensions between the United States and Iran.

Coke production hasn’t registered notable rises in March, mainly due to constant production restrictions amid tightened environmental regulations as well as meagre profits. The daily met coke output of the 230 independent coke firms surveyed by Mysteel averaged 5.08 million t/d in March, only higher by 0.9% on month and 0.6% on year.

The constrained production pace will likely keep a healthy fundament for the met coke market in April, favoring in further price hikes, according to the report.

However, the report warns of a major risk from uncertain coking coal prices going forward, impacted mainly by the developing geopolitical situations. The sentiment for coking coal could steer a responding shift in the steel market, passing the impact further to coke prices as well.

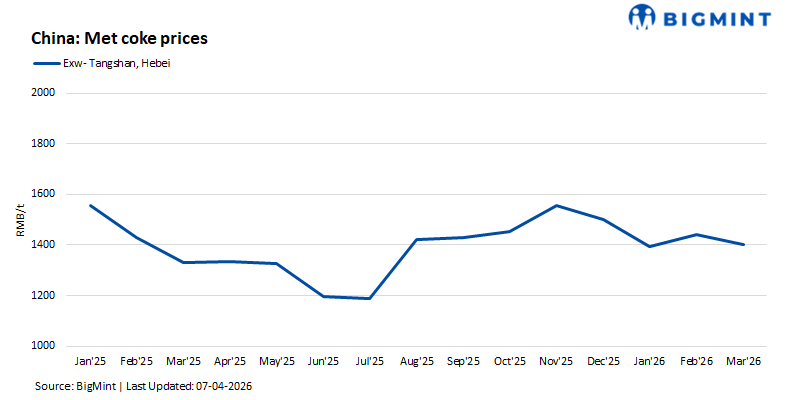

As of April 2, Mysteel’s assessment of the national quasi-first-grade met coke prices for wet- and dry-quenching types stood at Yuan 1,425.5/t and Yuan 1,569.8/t, including the 13% VAT, respectively, with the former staying flat and the latter shedding Yuan 2.4/t on month.

Note: This article has been written in accordance with a content exchange agreement between Mysteel and BigMint.

Leave a Reply