- Asian prices stable on firm bookings and rising costs

- Middle East disruptions elevate logistics risks and pricing

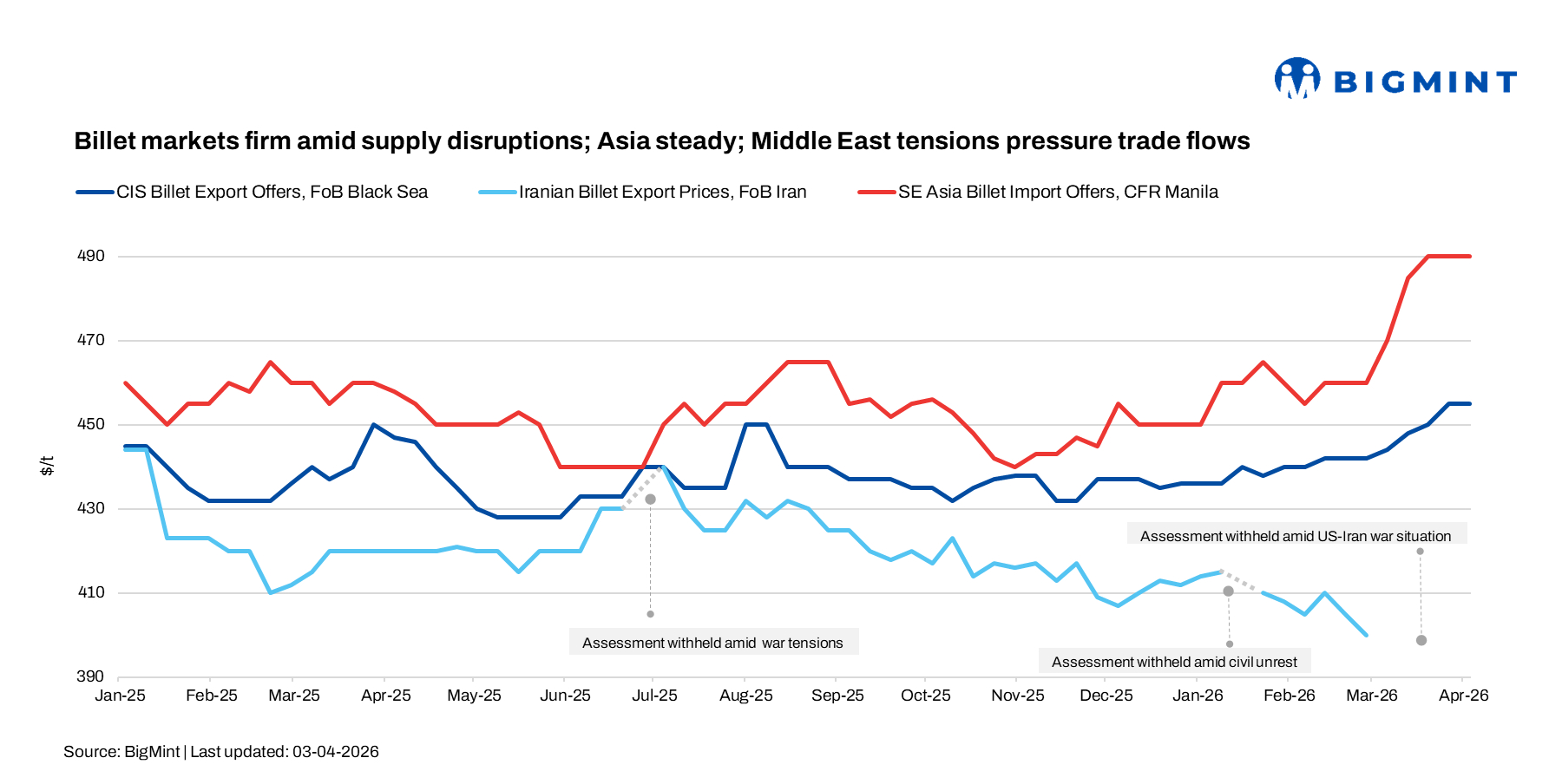

The global billet market remained mixed in the past week, with Asian markets showing relative stability, while CIS/Black Sea and GCC regions experienced upward pressure driven by supply disruptions, geopolitical tensions, and rising logistics costs. The ongoing escalation in the Middle East, particularly involving Iran, has emerged as a key factor influencing supply chains, freight dynamics, and pricing trends across regions.

In Turkiye, deep-sea scrap prices strengthened over the week, with US-origin HMS 80:20 rising from around $398/t to $403-405/t CFR, supported by robust bookings earlier and tight supply. Mills actively secured April-May cargoes, while offers remained firm above $400/t, keeping sellers in control. The uptrend was driven by higher freight and energy costs, along with rising billet prices, while rebar export offers stayed at around $600/t FOB and above, allowing mills to pass on some cost pressure.

Asian billet market

Asian billet markets remained largely stable w-o-w, with market participants indicated that there was no significant change in pricing, with offers largely in line with last week’s levels.

A Southeast Asian billet trader noted that Chinese billet deals were heard around $490/t CFR Philippines (5sp, 150mm), with the market showing little movement w-o-w. “We haven’t seen any major change in Asia-offers are largely at the same levels as last week,” he said.

FOB offers from China were reported at $465-470/t for May-June shipment, compared to $460-470/t FOB in the middle of the previous week. The slight uptick was majorly due to rising raw material and freight costs, while several mills were heard to be out of the market due to sufficient forward bookings.

“Many China-based producers are not offering today. Some offers went up due to raw materials and freight cost increase,” an Asian trader noted showing tightening availability.

Market participants emphasised that mills are under no pressure to sell, with one source stating, “The producer is not in a hurry to sell,” indicating strong demand visibility and seller confidence.

In the domestic Chinese market, billet prices rose RMB 20/t ($3/t) w-o-w to RMB 2,980/t ($433/t) on 3 April, supported by improved sentiment, higher oil prices linked to Middle East tensions, and seasonal improvement in finished steel demand.

However, gains plateaued later amid moderate demand, holiday slowdown, and softer raw materials. Iron ore declined by RMB 25/t ($4/t) and coke prices weakened, reducing cost support, while SHFE rebar futures fell RMB 42/t ($6/t) to RMB 3,097/t ($450/t), reflecting cautious sentiment. Export offers remained stable, with mills showing some flexibility.

CIS & Black Sea market

In the Black Sea region, billet prices remained firm, with Russian-origin material was heard at above $450-455/t FOB, translating to $485-490/t CFR Turkiye. Market participants indicated that offers have strengthened, supported by supply tightness and rising cost pressures.

Another CIS trader source added that Russian billet offers were heard at $485-490/t CFR Turkiye, with FOB levels above $450-455/t from the Black Sea, indicating firm pricing across regions.

Turkiye continues to remain a key destination, with import parity supported by higher billet and scrap costs. However, buying interest remains cautious as mills face margin pressures, keeping transaction volumes relatively limited despite firm offer levels.

GCC steel market

Iran: Airstrikes on key steel plants, including KSC and MSC, have disrupted production, with KSC halting operations and MSC reducing output to nearly half due to power damage. Partial damage was also reported at Hormozgan Steel. Production remains uncertain amid risks of further attacks and ongoing energy shortages.

Export activity is largely stalled, with limited pellet offers at $95-100/t FOB. Meanwhile, tensions around the Strait of Hormuz have escalated logistics risks, with vessel delays, rising freight and insurance costs, and tighter maritime controls impacting trade flows.

Saudi Arabia: In Saudi Arabia, billet and scrap prices increased amid supply chain disruptions and limited access to imported raw materials. Domestic billet prices rose to $550-560/t exw, with delivered offers heard at around $555-560/t. Scrap prices increased by SAR 50/t ($13/t), reaching around $410-428/t, with higher levels reported in regions such as Jazan due to logistical constraints. Market participants noted aggressive buying by DRI-based mills, as they struggle to secure imported raw materials. “The situation is very unstable due to scrap, which is highly sought after now,” a market insider said.

UAE: In the UAE, logistical disruptions and supply chain inefficiencies continue to drive up costs. Alternative routes via Oman are adding $30-40/t to transportation costs, while local logistics expenses have also increased.

Market participants highlighted challenges in multi-modal logistics, with infrastructure limitations creating bottlenecks. “Even if alternatives like Fujairah port exist, they are not fully optimised for bulk cargo,” a source noted.

As a result, rebar prices increased by $40-55/t, with some offers exceeding AED 2,700/t ($735/t) delivered. Mills indicated that planning beyond April remains difficult due to uncertainty in supply chains. “It is hard to plan May and June. Logistics influence our ability to serve demand,” a market participant said.

Outlook: The billet market is likely to stay firm in the coming weeks mainly due to tight supply and rising freight and energy costs. While Asia is relatively stable, the Middle East is driving uncertainty, with disruptions in Iran and ongoing logistics issues across the GCC keeping the market on edge. Buyers and sellers are now factoring in higher risks, delays, and added costs, which is likely to keep trade cautious and pricing supported in the coming weeks.

Outlook: The billet market is likely to stay firm in the coming weeks mainly due to tight supply and rising freight and energy costs. While Asia is relatively stable, the Middle East is driving uncertainty, with disruptions in Iran and ongoing logistics issues across the GCC keeping the market on edge. Buyers and sellers are now factoring in higher risks, delays, and added costs, which is likely to keep trade cautious and pricing supported in the coming weeks.

Leave a Reply