- Steel scrap generation projection revised downward by 31 mnt

- China, developed markets see declining contribution

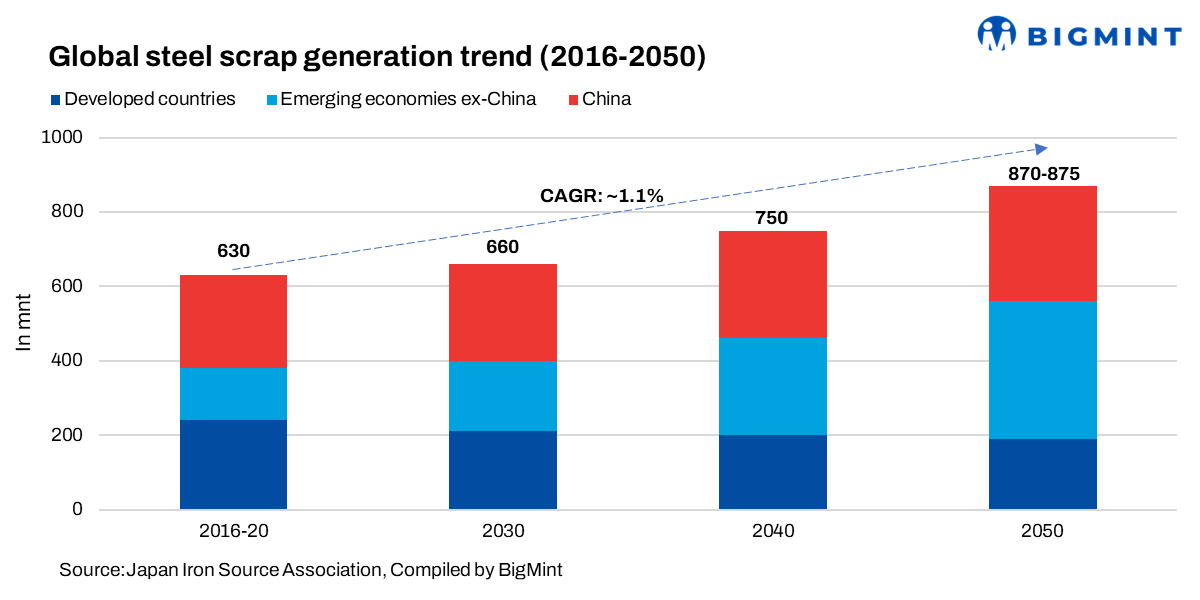

Japan Metal Daily: Global steel scrap generation is projected to reach 873 million tonnes (mnt) by 2050, revised downward by 31 mnt from the previous forecast, according to the Japan Iron Source Association’s latest Global Steel Scrap Supply and Demand Trends (26th edition). Despite the downward revision, global scrap generation is still expected to increase by 36% (232 mnt) compared to 2020 levels, indicating steady long-term growth.

Regional divergence

The revised outlook shows a clear regional shift. Scrap generation in emerging markets (excluding China) is projected at 370 mnt, revised upward by 16 mnt, with a stronger long-term steel demand. In contrast, China’s scrap generation is forecast at 311 mnt, down 26 mnt, while developed economies are expected to generate 193 mnt, down 20 mnt, showing a slowdown as these markets mature.

Steel consumption revisions, outlook changes

The changes in scrap generation are primarily driven by updated steel consumption forecasts over the next 50 years. Steel consumption in emerging markets has been revised upward to 923 mnt (an increase of 143 mnt), with growth expectations raised by 2% (from 1.5%). Meanwhile, China’s consumption is now projected at 621 mnt (down 48 mnt) with a decline rate of 1.2%, and that of developed markets is expected at 257 mnt (down 69 mnt) with a similar 1.2% downtrend, reflecting structural slowdown.

Circulation rate indicates recovery in generation efficiency

Scrap generation estimates are derived using the steel circulation rate — the ratio of scrap generation to apparent steel consumption. By 2050, this rate is expected to be 40% in emerging markets (down from 45.4%), 50% in China (slightly down from 50.4%), and 75% in developed markets (up from 65.3%). This highlights higher recycling efficiency and mature scrap recovery systems in developed economies, while emerging markets continue to build capacity.

While scrap consumption may fluctuate with short-term steel demand, in the medium to long term, scrap availability is closely linked to steel stock accumulation and recovery infrastructure. As economies develop, circulation rates typically improve, supporting higher scrap generation over time.

Outlook

Global scrap supply is expected to grow steadily through 2050, with BigMint estimating total generation at around 830-850 mnt. However, the geographical centre of supply is gradually shifting away from China and developed markets towards emerging economies, supported by stronger steel demand and improving scrap recovery systems.

Of the total scrap pool, approximately 720-730 mnt (over 85%) is expected to be consumed by the steel sector. Within this, the electric arc furnace (EAF) route is likely to account for around 620-650 mnt (85-88% of steel sector consumption), while the remaining volumes will be consumed through other BF-BOF route steelmaking routes, in foundry and allied industries.

This article is being published in accordance with an article sharing agreement between Japan Metals Daily and BigMint

Leave a Reply