- HRC trade prices hit 3-year high as supply tightens

- Mills hike BF rebar prices on fast inventory drawdown

- Maintenance closures, NMDC hike to support steel prices

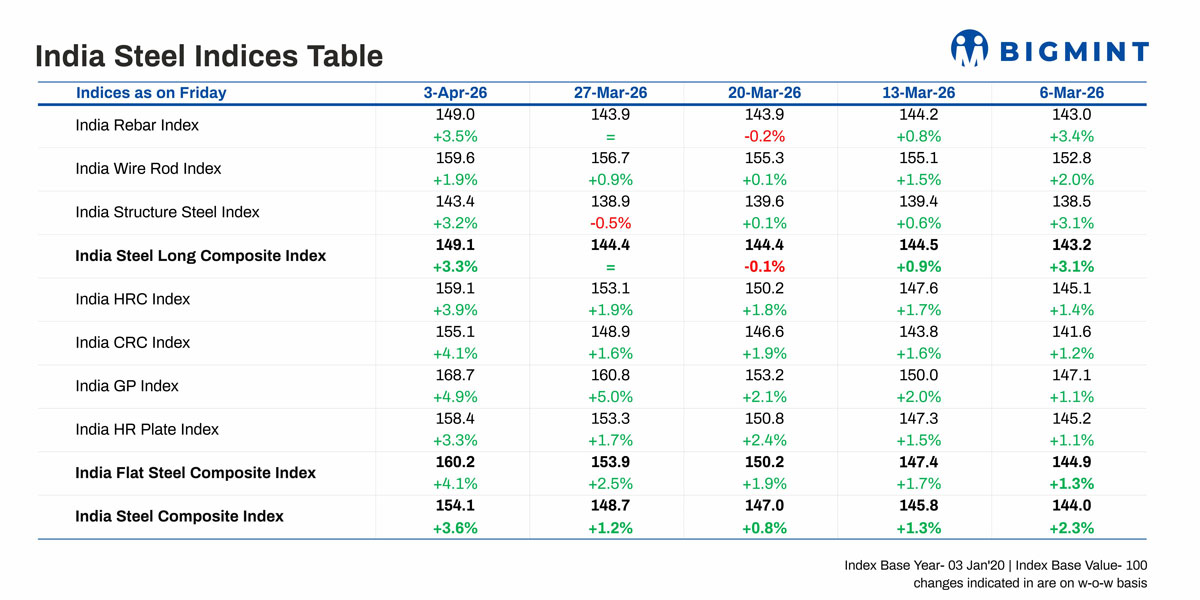

Morning Brief: BigMint’s India steel index, a barometer of the domestic market, edged up sharply w-o-w, as assessed on 3 April 2026, rising by 3.4% – the steepest weekly surge in recent times. Steel prices rose on raw material shortages such as that of ferrous scrap and natural gas amid geopolitical conflict in the Middle East, shortage of material in trade markets, and fast inventory drawdown. Downstream tightness due to production disruptions supported prices.

The flats composite index rose sharply by 4.1% w-o-w, while the longs index surged 3.3%, as the integrated mills raised prices across segments amid shrinking supply and strong demand.

Highlights of price movements

HRC trade prices hit 3-year high: Trade-level prices of hot-rolled coils (HRC) strengthened across regions, touching a three-year peak. BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) rose by INR 2,000/t ($21/t) w-o-w to INR 59,500/t ($634/t) as of 31 March compared to 24 March. CRC (IS513, Gr O, 0.9 mm/CTL) prices were assessed at INR 67,000/t ($713/t) on 31 March, increasing w-o-w by INR 2,000/t ($21/t.

HRC trade sentiment remained positive, supported by mill price hikes and supply constraints. Sentiment strengthened further toward the end of the week due to material shortages reported across regions. Additionally, a major producer increased prices for flat products, scheduled for late March deliveries, by INR 1,500/t ($16/t).

In April, several mills are considering maintenance shutdowns. At the same time, restocking activity has picked up, driven by expectations of further price increases and continued supply tightness.

Coated steel, plate prices surge: Coated flat steel prices recorded a sharp w-o-w increase, with the GP index recording a rise of 4.9% w-o-w on supply-side constraints and rising cost pressure. Producers hiked galvanised plain (GP) prices by INR 3,250/t ($35/t) and pre-painted galvanised iron (PPGI) by INR 2,500/t ($27/t) on escalating logistics costs and geopolitical uncertainties impacting input prices.

Likewise, BigMint’s weekly benchmark assessment for HR plate (20-40 mm, Gr E250 Br.) rose by INR 1,400/t w-o-w to INR 62,800/t as of 1 April against INR 61,400/t ($/t) as on 25 March. The increase was driven by resilient demand and growing uncertainty surrounding geopolitical tensions.

Bulk HRC imports decline: Flats prices received support from weakening flat steel imports. Bulk HRC imports fell to around 183,000 t (as of 27 March) compared to over 360,000 t in February due to the safeguard duty impact and the imported-domestic HRC price differential.

Mills hike BF rebar prices: The primary steelmakers again increased rebar list prices by up to INR 2,000/t ($22/t) for early April from end-March levels, sources informed BigMint. Trade-level BF-rebar prices (distributor to dealer) rose by INR 600/t ($6/t) w-o-w to INR 60,600/t ($654/t) exy-Mumbai, as per BigMint’s assessment on 3 April.

Rebar inventories at primary mills dropped by 20-25% m-o-m in early-April due to strong lifting of previously booked material last month. Mills reported healthy order bookings in March and continue to focus on fulfilling pending project-linked orders.

IF rebar market strengthens: IF rebar prices rose across major markets, with manufacturers revising gauge parity amid shortage of raw materials, particularly scrap and sponge iron, due to geopolitical reasons. Strong order bookings further supported the uptrend. Mills prioritised dispatches, maintaining low inventory levels of around 5-8 days. Induction furnace (IF) rebar trade prices in Mumbai rose by INR 3,000/t ($32/t) w-o-w to INR 53,400/t ($576/t) exw as on 3 April.

Outlook

Apart from these factors, it deserves mention that coking coal prices increased, too, providing support to steel prices. BigMint’s premium hard coking coal (PHCC) prices rose by $8/t w-o-w to $258/t CNF Paradip last week. Again, NMDC increased iron ore prices from Chhattisgarh by $5-6/t (INR 450-550/t) which is expected to keep steel prices elevated going forward.

Scrap and gas shortages due to geopolitical disruptions, supply tightness due to mill maintenances announced in April and cost push from the raw materials segments are expected to keep steel prices elevated. However, the cost factor seems to be propelling prices more than any dramatic resurgence in demand. But as recent price hikes have been absorbed by the market, it is logical to expect that mills will be looking to hike prices further in April, although this could hurt downstream sectors such as auto and construction.

Leave a Reply