- Limited scrap imports tighten supply, lift offers

- Improved rebar demand supports price uptrend

Steel prices in the southern market increased sharply by around INR 1,500-2,000/t w-o-w, primarily driven by rising input costs such as sponge iron and scrap. Additionally, strong finished steel demand supported higher price realisations, encouraging producers to raise their offers across markets.

Sponge iron

Sponge iron prices in the Bellary region surged by around 7% (INR 1,500/t), reaching approximately INR 29,000/t ex-Bellary as of 3rd April 2026. On a m-o-m basis, prices moved up by nearly 5%, reflecting a consistent upward trajectory.

The key driver behind this surge is the steep rise in raw material costs. Non-coking coal prices increased by around 20% m-o-m to INR 11,110/t ex-Gangavaram, significantly impacting production economics. Additionally, iron ore pellet (63% grade) prices hovered near INR 11,150/t ex-Bellary, further adding to cost pressures.

As a result, sponge iron producers revised their offers upward to protect margins. Overall market sentiment remained firm, supported by elevated input costs and stable demand conditions.

It is estimated that sponge iron manufacturers have already secured bookings for approximately 15-20 days of production in advance. This forward coverage has significantly improved their sales visibility.

As a result, producers are currently under minimal sales pressure, allowing them to maintain firm offers and avoid aggressive selling in the market.

Melting scrap

Melting scrap prices in south India also surged, particularly in Hyderabad, where prices increased by around 9-10% (INR 3,200/t w-o-w) for HMS 80:20 Gr to INR 36,000/t as on 03 April 2026. This sharp rise reflects tight supply conditions and strong demand from steelmakers.

In comparison, Chennai witnessed a relatively moderate increase of INR 300-500/t w-o-w, indicating regional variations in supply-demand dynamics. The primary factor influencing this trend is the limited availability of scrap in the domestic market.

Due to constrained supply, steel producers are increasingly shifting towards higher sponge iron consumption in their raw material mix. Furthermore, global scrap bookings remain subdued owing to high logistics costs, longer lead times, and a stronger dollar, making imports less attractive. Overall, the scrap market continues to remain firm under supply pressure.

MS billet

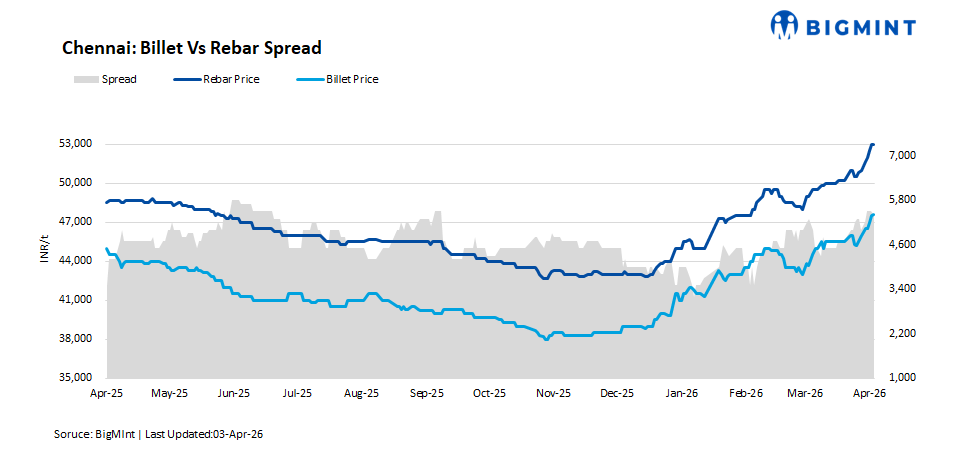

Mild steel (MS) billet prices in South India increased by around INR 1,500-2,000/t, driven largely by rising input costs, particularly sponge iron and melting scrap. Billet prices stood at around INR 44,500/t ex-Hyderabad.

At the same time, robust demand from re-rolling mills has supported price increases, allowing manufacturers to raise their offer levels. The combination of cost pressure and healthy downstream demand has strengthened the billet market.

Notably, conversion margins from melting scrap to billet have widened w-o-w. The spread for HMS 80:20 to MS billet has increased from around INR 10,800/t to INR 11,800/t in Chennai, as producers attempt to recover earlier losses and benefit from improved realisations.

Rebar

Rebar prices across South India continued their upward movement, particularly in the induction route segment, where prices have risen by around INR 1,500-2,000/t w-o-w. This increase was supported by strong domestic demand and higher input costs.

Currently, induction route rebar prices were at approximately INR 51,500/t ex-Hyderabad. Meanwhile, in the blast furnace (BF) route segment, prices have increased steadily, with 12-25 mm rebar priced at around INR 61,500/t ex-Chennai, up by about INR 1,500/t w-o-w.

The price gap between induction and BF route rebar stood at around INR 9,000/t, reflecting differences in cost structures and production processes. Overall, the rebar market remains firm, backed by strong demand and elevated raw material costs.

Leading steel manufacturers continue to offer induction route rebars in the local market at prevailing price levels, although selective discounts are being extended in offers to attract buying interest of customers :

Outlook

The near-term outlook for steel prices remains positive. The resumption of fresh bookings across markets is expected to improve trade activity and support price realisations.

Additionally, the onset of seasonal demand, particularly from construction and infrastructure sectors, is likely to provide further momentum. With demand strengthening and input costs remaining elevated, steel prices are expected to stay firm in the coming weeks.

Leave a Reply