- Strong dollar, geopolitical uncertainties limit imports

- Gas supply disruptions impact scrap cutting, processing

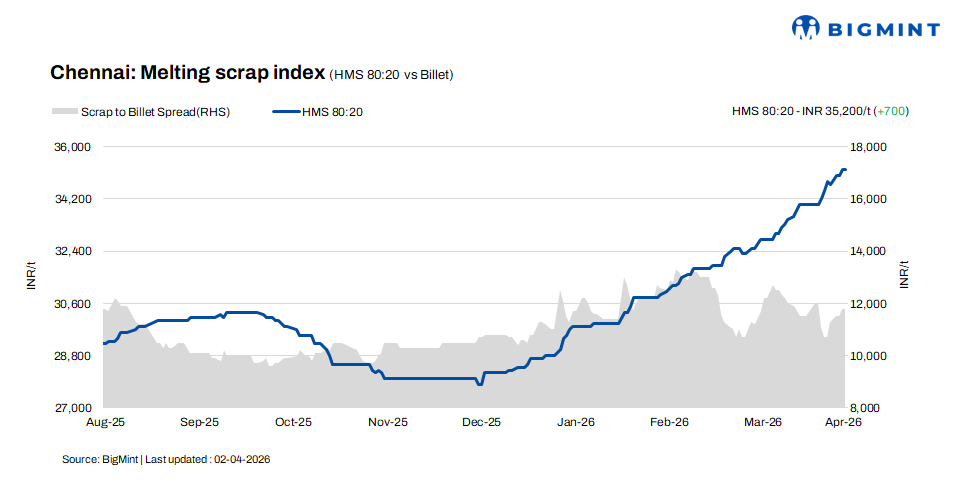

In the Chennai market, HMS (80:20) prices increased by INR 700/t w-o-w to INR 35,200/t on 2 April 2026 while remaining stable d-o-d, as per BigMint’s assessment. Meanwhile, billet prices rose by INR 2,300/t w-o-w and registered a daily increase of INR 500/t, settling at INR 47,500/t. Similarly, rebar prices climbed by INR 2,500/t w-o-w to INR 53,000/t while increase by INR 500/t d-o-d. Market sentiment strengthened, driven by improved steel trade and gas-related supply constraints.

Imported, domestic price trends

According to sources, imported shredded scrap from Australia was offered at $385-390/t CFR Chennai, while HMS (80:20) offers stood at $365-370/t CFR. Buyers were placing bids $5-10/t below these levels, resulting in limited deal activity. The firm dollar and ongoing geopolitical uncertainties pushed up import parity, leading to muted buying interest in the market.

In the domestic market, HMS (80:20) scrap prices were quoted at INR 35,000-35,500/t for spot deals with immediate payment, while transactions on extended credit terms were concluded at INR 35,500-36,000/t. Market activity remained largely confined to the INR 35,000-36,000/t range, highlighting stable demand-supply dynamics, with premiums observed for extended payment terms.

Buyer-supplier sentiments

A scrap supplier indicated that HMS (80:20) prices were within INR 35,000-36,000/t, with variations largely dependent on payment terms and mill-specific volume requirements. The ongoing commercial gas supply disruption continued to impact scrap cutting and processing activities across regions. With most processors relying on gas-based cutting, the recent surge in gas prices — which are now more than double the usual levels — has significantly increased operational costs.

At the same time, reduced import bookings amid a stronger dollar have further tightened supply conditions. This dual impact of cost pressure and supply constraints supported domestic scrap prices, with market participants expecting firm pricing trends in the coming sessions.

A mill representative noted that sponge iron prices increased by around INR 1,000/t w-o-w, primarily driven by the ongoing shortage of scrap in the market. Additionally, consistent price increases from neighbouring states have further supported the upward trend in sponge iron prices. Mills are currently operating with a 70:30 feedstock mix (scrap to sponge iron), reflecting high dependence on scrap despite supply constraints.

Billet demand improved in the Chennai market, along with increased buying interest from neighbouring states. Meanwhile, demand for rebar strengthened, particularly from the government and infrastructure project segment, providing a strong base for price support. Overall, improving steel demand and tight raw material availability kept market sentiment firm and positive.

Regional comparison

The Jalna market witnessed an upward trend d-o-d, with billet prices rising by INR 400/t to INR 46,300/t Meanwhile rebar and HMS 80:20 prices rose by INR 200/t d-o-d to INR 54,300/t and INR 34,200/t. Active trading was observed across the steel segment over the past couple of days, indicating improving market participation.

Outlook

The Chennai scrap market is expected to remain firm next week, supported by tight availability due to gas-related processing constraints and limited imported bookings. Improved billet and rebar prices are also providing support to overall sentiment.

Leave a Reply