- Benchmark HRC prices rise by INR 2,000/t ($21)

- Mill hikes and restocking lift market sentiment

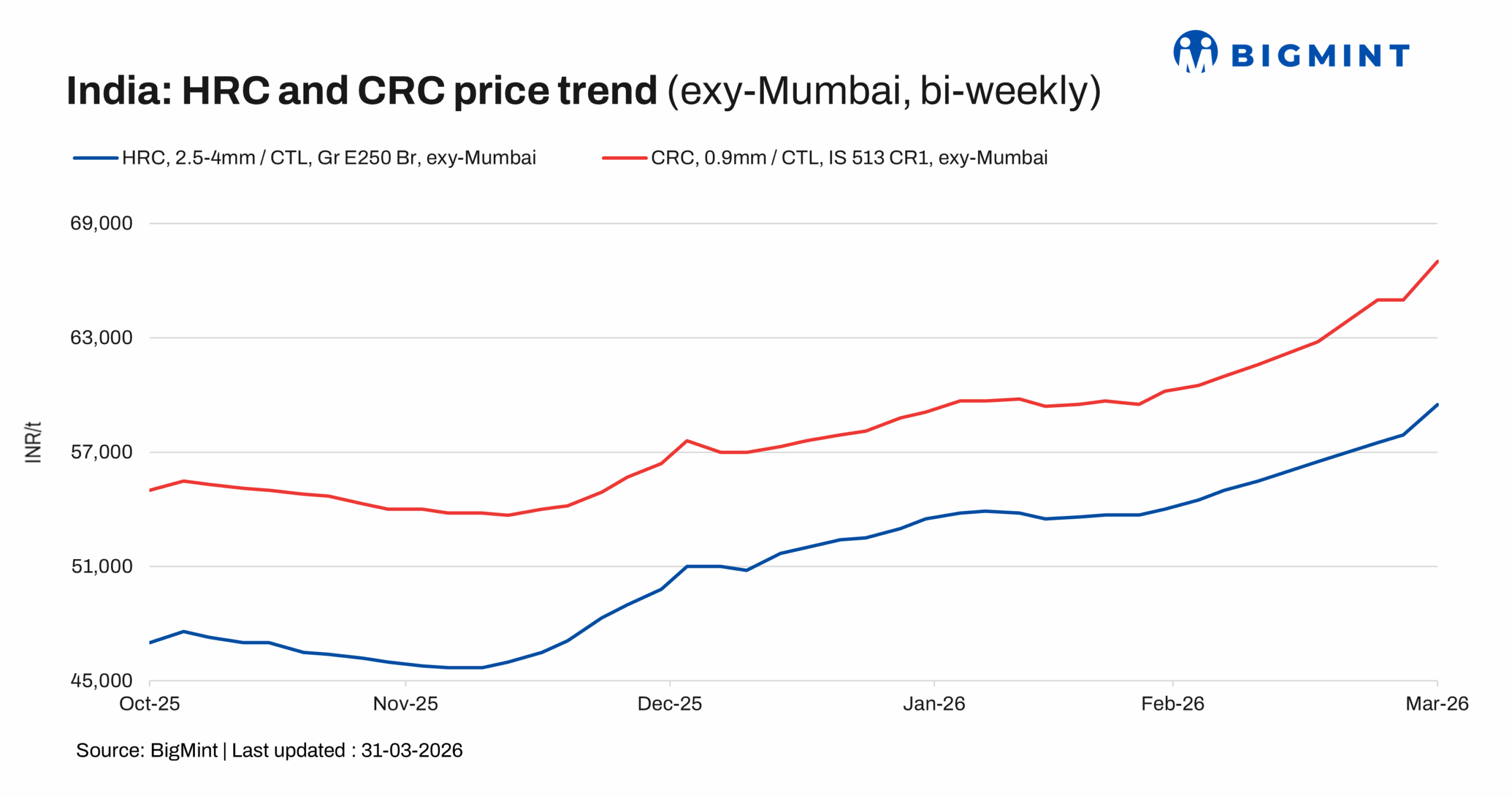

Trade-level prices of hot-rolled coils (HRC) in India strengthened across regions, touching a 3-year peak, with HRC prices assessed in the range of INR 55,500-59,600/t ($591-635/t) and cold-rolled coil (CRC) prices assessed at INR 59,800-67,000/t ($637-714/t).

BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) rose by INR 2,000/t ($21/t) w-o-w to INR 59,500/t ($634/t) as of 31 March, compared to INR 57,500/t ($613/t) on 24 March.

Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) prices were assessed at INR 67,000/t ($713/t) on 31 March 2026, marking a w-o-w increase of INR 2,000/t ($21/t) from INR 65,000/t ($692/t) on 24 March. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market Update

Indian trade-level HRC sentiment remained positive, supported by mill price hikes and ongoing supply constraints. Market sentiment strengthened further toward the end of the week, with material shortages reported across multiple regions.

However, as this week marks the end of the fiscal year, participants noted that trading activity has been sluggish. Adding to this, sellers are currently refraining from offering material, anticipating further price increases and aiming to maximise margins.

Additionally, a major Indian steel producer has increased prices for flat products scheduled for late March deliveries. HRC and CRC prices have been raised by INR 1,500/t ($16/t).

Looking ahead to the coming month, several mills are considering maintenance shutdowns, which are likely to play a key role in shaping market dynamics. At the same time, sources informed Bigmint, “restocking activity has picked up, driven by expectations of further price increases and continued tightness on the supply side”.

In the downstream segment, operations are facing pressure due to an intensifying LPG shortage. Additionally, market chatter highlighted that “uncertainty surrounding ongoing geopolitical tensions continues to weigh on sentiment”.

Additional updates

Import volumes: India’s bulk imports of HRCs touched 183,326 t as on 27 March. Around 2,08,601 t of additional cargoes are expected.

Export volumes: India’s bulk exports of HRCs touched 156,394 t as on 27 March. Around 15,500 t of additional cargoes are expected.

Outlook

Despite these challenges, the overall outlook remains positive. Market participants anticipate that prices will continue to trend upward in the near term, with current levels being largely absorbed across the market. The HRC market is expected to retain an upward bias, supported by tight supply and expected mill price increases, even as cautious restocking continues amid demand-side constraints and ongoing geopolitical uncertainty.

Leave a Reply