- Refined output weak, secondary surge offsets primary decline

- Chile disruptions and Asia slowdown tighten supply outlook

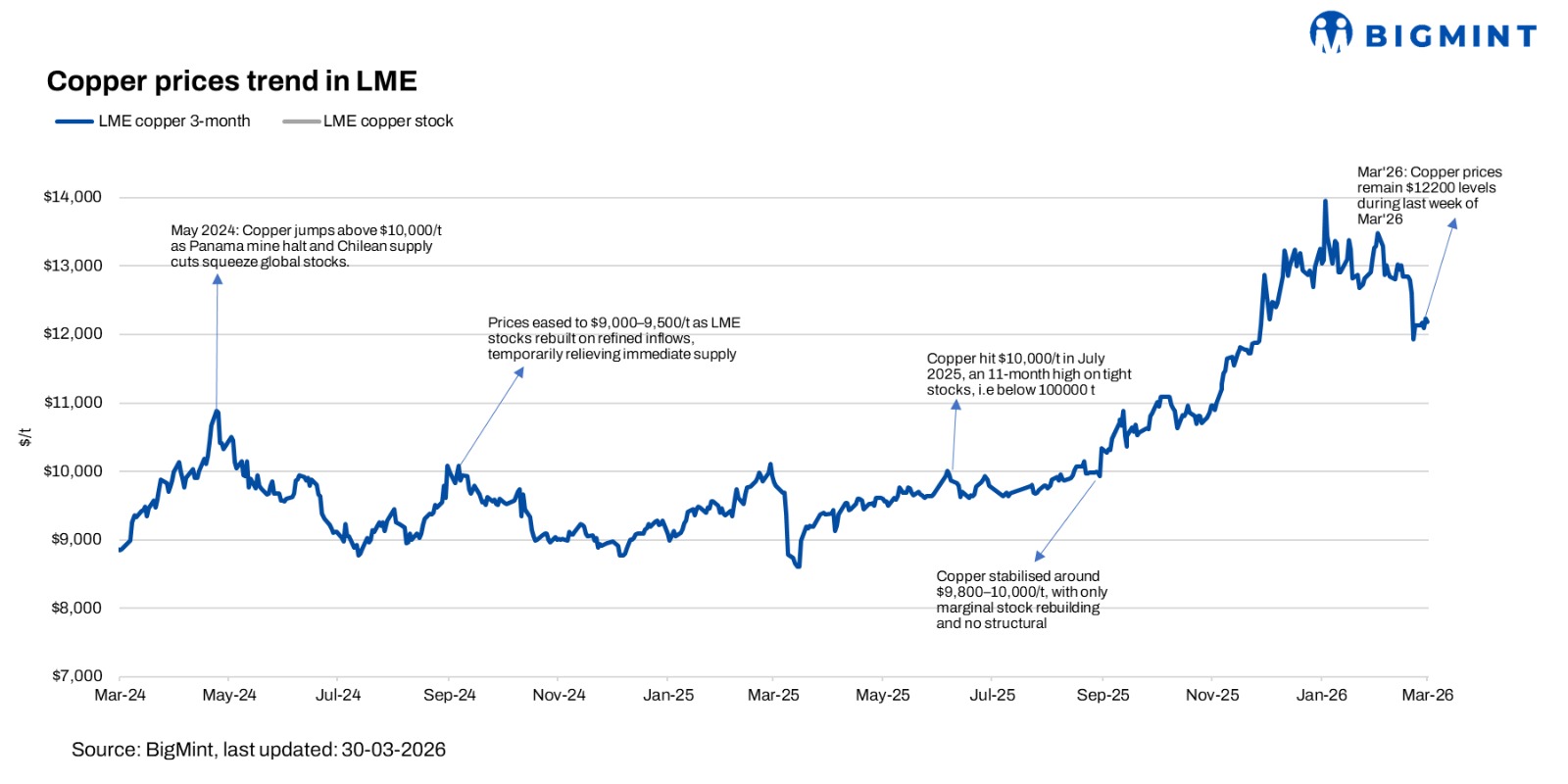

LME copper prices edged higher to $12,220/t, up 0.17% w-o-w, indicating a tight but capped market where supply constraints persist but demand remains measured.

Regional trends in copper mine production

Global copper mine output rose 2.2% year-on-year in January 2026, supported by a 2% increase in concentrate production and a stronger 2.8% rise in SX-EW output. Concentrate output, however, remained constrained by the lingering impact of two major accidents in 2025, which continued to weigh on production in Indonesia and the Democratic Republic of Congo (DRC). This was partly offset by stronger performance in other regions. Peru, for instance, recorded a 3% year-on-year increase in mine production, driven by higher output at Antamina, Las Bambas, Antapaccay and Toromocho.

In contrast, Chile’s output declined by 3%, as production cuts at Spence, El Teniente and Los Pelambres more than offset gains at Centinela, Collahuasi and Quebrada Blanca. Meanwhile, Mongolia saw a sharp increase of around 35% in copper concentrate production, reflecting the continued ramp-up of the Oyu Tolgoi underground project.

Refined copper production shows modest growth

Preliminary data shows global refined copper production rose just 1% in January 2026, as a 1.4% decline in primary output was offset by an 11% surge in secondary production. China and the DRC, which together account for approximately 59% of global refined copper production, recorded a combined increase of 5%. Excluding them, world refined copper output declined by 4.5%.

Chile had a particularly bad month, with refined output down 25% overall as its smelter-based electrolytic production collapsed 63% due to maintenance shutdowns. India continued its upward trajectory, recording a 10% increase, supported by improved operating capacity rates and the ongoing ramp-up of the Adani refinery.

An important structural development is downstream expansion. Precision Wires India has approved multiple expansion and modernization projects at its Silvassa facilities, including additional copper rod and winding wire capacity, with 4,400 t/year incremental capacity expected by FY27, taking total installed capacity to ~65,400 t/year. This indicates steady growth in domestic copper consumption, especially from electrical and industrial segments.

However, on the demand side, buying remains cautious. Chinese consumers continue to procure on a need basis, while stable LME inventories have reduced urgency. In the scrap market, tight availability persists due to material being held back, supporting localized premiums.

Overall, the marginal weekly gain reflects a structurally tight market with weak production growth and ongoing downstream expansion, but near-term price movement remains rangebound due to cautious demand and macro uncertainties.

Leave a Reply