- Prices rebound above $3,050/t

- Sustained stock decline supports prices

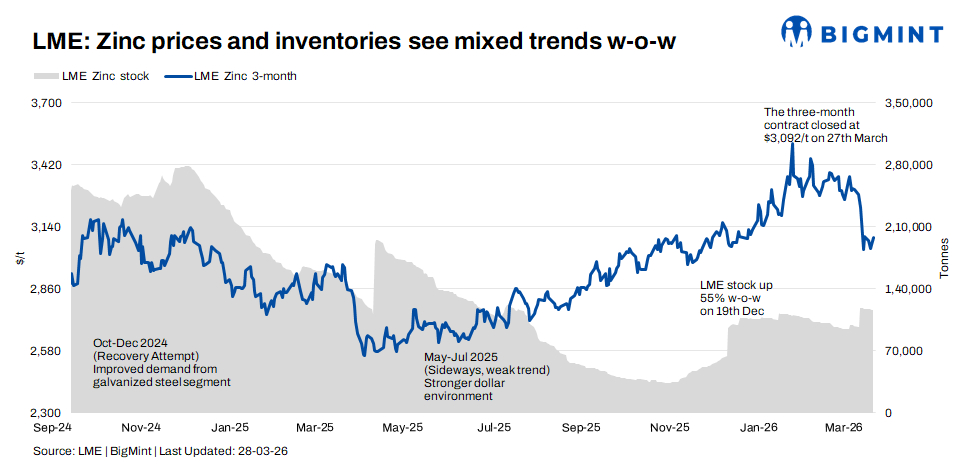

London Metal Exchange (LME) zinc prices showed a mild recovery in the week ended 27 March, supported by a gradual drawdown in exchange inventories and improved sentiment mid-week. Prices traded within a narrow range but managed to hold above the $3,050/t level, as easing stock levels provided some support despite cautious buying activity.

Price trends

LME zinc cash prices opened at $3,040/t on 23 March and remained largely rangebound during the initial sessions. Prices dipped slightly to $3,037/t on 24 March before gaining momentum, rising to a weekly high of $3,077/t on 26 March. The contract closed the week on a firmer note, reflecting a modest recovery trend.

On a w-o-w basis, cash prices increased by around 0.8-1%, compared with the previous week’s close of $3,065.5/t, indicating a stabilisation after the sharp correction observed earlier.

The three-month contract followed a similar trajectory. Prices opened at $3,077.5/t and slipped to $3,042/t early in the week, before rebounding to $3,092/t by 26 March. The forward curve reflected mild strength, supported by improving near-term sentiment and inventory drawdowns.

Inventory analysis

LME zinc inventories declined steadily throughout the week, offering support to market sentiment. Stocks fell from 117,675 t on 23 March to 115,650 t by 26 March, marking a consistent drawdown across sessions.

On a w-o-w basis, inventories registered a decline of around 1.7%, indicating a modest tightening in visible supply. The absence of fresh inflows and continued stock withdrawals helped stabilise prices after the previous week’s sharp build-up. However, overall inventory levels remain relatively elevated, limiting the scope for a stronger upside.

MCX zinc trends (23-27 March)

On the Multi Commodity Exchange (MCX), zinc futures traded in a narrow range, reflecting mixed global cues. The March contract opened at INR 306,250/t on 23 March and witnessed volatile movement during the week, reaching a high of INR 318,000/t before easing.

Prices declined mid-week to a low of INR 307,000/t and eventually closed at INR 310,900/t on 27 March, registering a marginal w-o-w gain.

Open interest declined significantly from 650 lots at the start of the week to 89 lots by Friday, indicating long liquidation ahead of contract expiry. Trading volumes also tapered towards the end of the week.

Domestic demand conditions remained stable, with buying largely need-based as participants avoided aggressive positioning amid uncertain price direction.

SHFE zinc trend

On the Shanghai Futures Exchange (SHFE), zinc prices exhibited a mixed trend during the week. Prices declined from $3,292/t on 23 March to $3,270/t by mid-week, before recovering to $3,296/t on 26 March.

The movement mirrored global cues, with initial weakness followed by a mild rebound. Chinese market sentiment remained cautious, with limited buying support amid unclear demand signals.

Outlook

In the near term, zinc prices are likely to trade in a narrow range, with steady inventory drawdowns offering support while elevated stock levels continue to cap sharp upside.

Prices may find support in the $3,020-3,050/t range, while resistance is expected around $3,100-3,150/t. Market participants are likely to remain cautious, with further price direction dependent on inventory trends and demand recovery signals.

Leave a Reply