- Global copper output edges up, in spite Indonesia and DRC disruptions

- Refined copper surplus narrows, even as exchange stocks hit 23-year high

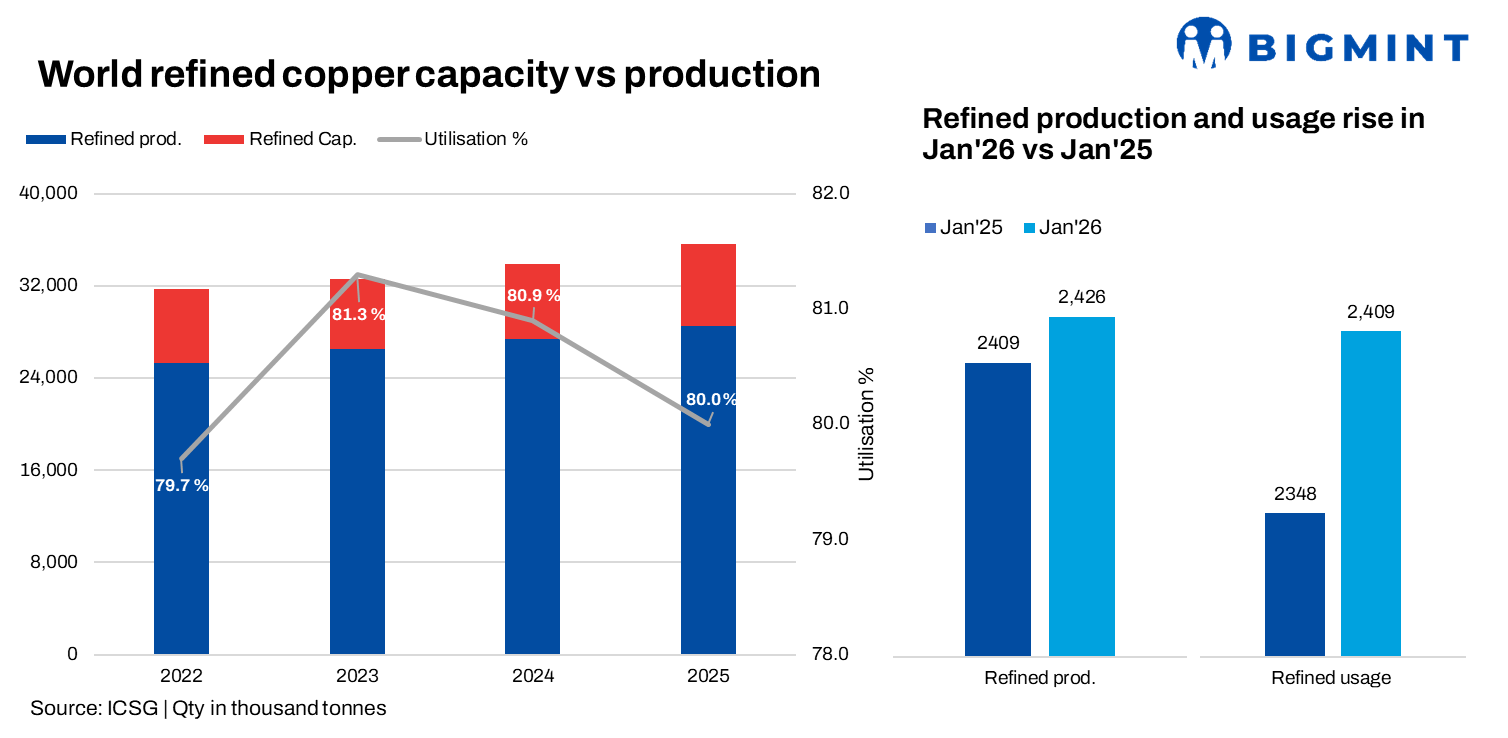

Global copper mine production rose about 2.2% y-o-y in January 2026, while refined copper output grew by just 1%, as a 1.4% drop in primary production was partly offset by an 11% rise in secondary output, the International Copper Study Group reported.

Regional trends in copper mine production

Global copper mine output rose 2.2% year-on-year in January 2026, supported by a 2% increase in concentrate production and a stronger 2.8% rise in SX-EW output. Concentrate output, however, remained constrained by the lingering impact of two major accidents in 2025, which continued to weigh on production in Indonesia and the Democratic Republic of Congo (DRC). This was partly offset by stronger performance in other regions. Peru, for instance, recorded a 3% year-on-year increase in mine production, driven by higher output at Antamina, Las Bambas, Antapaccay and Toromocho.

In contrast, Chile’s output declined by 3%, as production cuts at Spence, El Teniente and Los Pelambres more than offset gains at Centinela, Collahuasi and Quebrada Blanca. Meanwhile, Mongolia saw a sharp increase of around 35% in copper concentrate production, reflecting the continued ramp-up of the Oyu Tolgoi underground project.

Refined copper production shows only modest growth

Preliminary data shows global refined copper production rose just 1% in January 2026, as a 1.4% decline in primary output was offset by an 11% surge in secondary production. China and the DRC, which together account for approximately 59% of global refined copper production, recorded a combined increase of 5%. Excluding them, world refined copper output declined by 4.5%.

Chile had a particularly bad month, with refined output down 25% overall as its smelter-based electrolytic production collapsed 63% due to maintenance shutdowns. India continued its upward trajectory, recorded a 10% increase, supported by improved operating capacity rates and the ongoing ramp-up of the Adani refinery.

In Asia (excluding China), output declined by 8.5%, mainly due to lower production in Japan, Indonesia and the Philippines. Global secondary refined production increased by 10%, largely driven by growth in China.

Refined copper usage grows

The world refined copper usage rose by ~2.5% in January 2026. China’s apparent demand grew only modestly (1%), with imports fell sharply by 44%, reflecting higher domestic supply. Demand outside China rose by around 4%, driven by Asian and MENA countries, offsetting weaker demand from EU.

Market surplus narrows but warehouses are overflowing

The monthly refined copper surplus was just 17,000 tonnes in January 2026, a significant drop from the 60,000-tonne surplus of January 2025. However, copper inventories held at the three major metal exchanges (LME, COMEX, and SHFE) hit the highest level since March 2003. That’s a 61% jump from end-December 2025 levels, with Shanghai accounting for most of the build (+246,000 tonnes).

Prices softened slightly

The average LME copper price dipped marginally in February to $12,968 per tonne, down by 1% from the January average of US$13,088.88/t. The 2026 year-to-date average of $12,907 remains about 30% above the 2025 annual average, suggesting markets still hold a constructive long-term view on copper despite the near-term oversupply.

Market Outlook

The global copper surplus narrowed in January, supported by recovering mine supply and improving demand outside China. However, excess supply from 2025 persists, with exchange inventories rising to a 23-year high, indicating material has shifted into storage. In the near term, prices may remain range-bound until stronger industrial demand absorbs these elevated stocks.

Leave a Reply