- Freight, energy costs impacting global sentiment

- Improved scrap flows post-winter in Europe

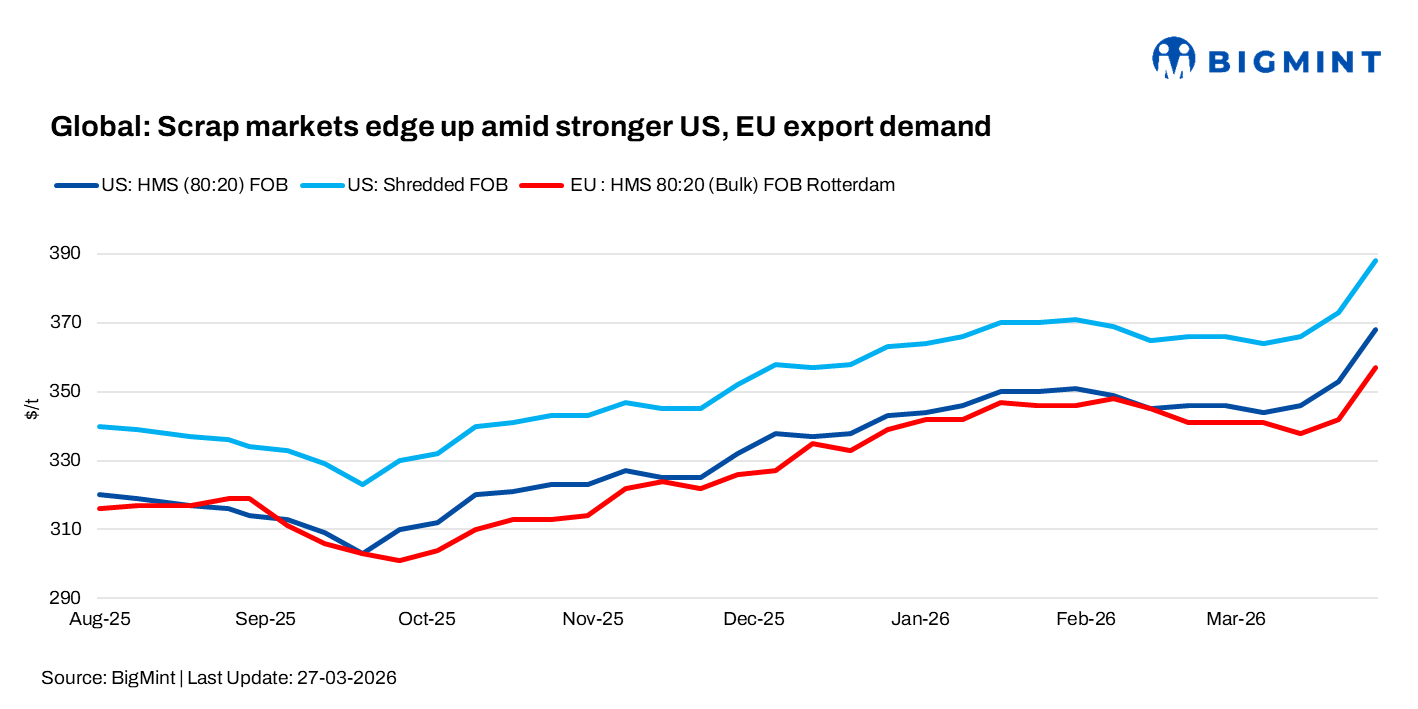

Global ferrous scrap export markets showed mixed but largely stable-to-firm trends this week. Strength in export markets, particularly driven by Turkish restocking, supported sentiment in the US and Europe, while other regions like Brazil and Mexico remained steady amid cost pressures and regional imbalances.

Improved scrap flows post-winter in Europe and stable domestic demand in key markets helped maintain price stability, despite ongoing macro uncertainties and freight cost volatility.

US

Ferrous scrap sentiment remained stable-to-firm during the week, with prices expected to stay largely flat m-o-m for April despite stronger export markets. Busheling held at $445/t delivered Midwest and $450/t Southeast, while shredded remained at $450/t and HMS at $400/t.

Support came from a rise in export prices, with Turkish import HMS 80:20 reaching $398-400/t CFR, driven by active restocking and improved rebar prices. This reduced downside pressure on domestic markets.

However, abundant supply in the US is likely to cap further gains, keeping domestic prices stable even as global indicators trend upward.

Europe

The EU/UK scrap market remained firm this week, with domestic prices rising by euro 5-10/t ($6-12/t) to euro 285-295/t ($328-340/t), supported by steady mill demand. Scrap collection also improved following the winter period, aiding supply conditions.

Export sentiment strengthened as import demand from Turkiye picked up after Eid, providing additional support to the market.

At dock levels, around 1,000 t of HMS were sold at euro 295/t ($340/t), with corresponding FOB levels indicated at euro 310/t ($357/t), reflecting firm pricing in the export segment. According to market insiders, scrap inflows to yards have improved.

Brazil

Ferrous scrap market remained stable in the week ended 27 March, though rising diesel costs and PIS/Cofins tax changes created mixed sentiment. Steelmakers adopted varied strategies, while recyclers pushed for higher prices due to increased costs.

Domestic prices held steady, with HMS 80:20 at Real 848-850/t ($161-162/t) and clean scrap at Real 925-930/t ($177-178/t). Export sentiment remained weak, with HMS at $285-290/t FOB and shredded scrap at $305-310/t FOB amid high freight rates.

Mexico

Ferrous scrap market sentiment remained largely stable during the week ended 27 March, despite regional price pressures. Busheling was assessed at MXN 7,800/t ($430/t) and HMS 1 at MXN 7,100-7,200/t ($392-397/t) FOT Northeast, with overall levels unchanged.

However, downward pressure was noted across regions, particularly in the Central market, where prices declined in phases during the week. In the Northeast, adjustments varied by mill, with some reporting declines of MXN 200-400/t ($11-22/t), while others indicated stable HMS levels.

Market participants stated that steady scrap demand helped limit sharper declines. Overall, sentiment leaned slightly bearish, but prices are expected to remain stable in the near term, with clearer direction likely after the Easter period.

Outlook

In the upcoming days, scrap export markets are expected to remain stable to firm. Continued Turkish demand and elevated freight and energy costs may support export-linked regions, while abundant supply in the US could cap upside. In Europe, improved inflows and steady mill demand should keep prices supported. Meanwhile, Latin American markets may see limited movement, with cost pressures and cautious demand shaping a stable outlook, with clearer trends likely emerging post-Easter.

Leave a Reply