- Producers push for increases due to rising coking coal costs

- Mills resist coke price hikes amid thin margins, ample stocks

Mysteel Global: China’s metallurgical coke market remained stable on 25 March, with the first round of price hikes initiated by some coke producers earlier this week yet to materialise, as their negotiations with major steelmakers are still underway.

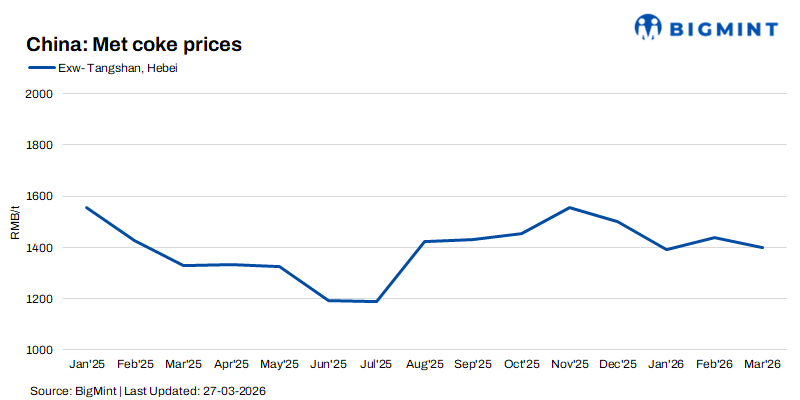

On Wednesday, Mysteel’s assessments for China’s quasi-first-grade met coke prices for wet- and dry-quenching types came in at RMB 1,381.7/tonne (t) ($200.5/t) and RMB 1,516/t, including 13% VAT, respectively, staying flat for more than a week.

Market fundamentals showed little improvement, with supply and demand largely stable. However, sentiment shifted as Dalian’s main coke futures declined by 1.8% in Wednesday’s daytime trading. This prompted some traders engaged in arbitrage to liquidate part of their positions, leading to a moderation in previously bullish expectations.

While Tangshan, the country’s top steelmaking hub and also a key coke-producing centre, yesterday launched a Level II emergency response to heavy pollution, local hot metal production has yet to be affected, and the impact on coke producers is limited as most of them are largely maintaining earlier production curbs, sources noted.

At ports, trading activity remained moderate, and port inbound shipments were also broadly steady. As of Wednesday, stocks at Rizhao port stood at 460,000 t, flat from a day ago, while Qingdao port held 810,000 t in stock, up 10,000 t on day. The combined inventory, 1.27 million tonnes (mnt), was only 120,000 t higher than a week ago.

Market participants noted that the implementation of the first round of coke price hikes has been postponed, as mainstream steel mills have yet to respond, leaving the market in a negotiation phase.

Steel mills’ hesitation is mainly driven by profitability and demand concerns. Blast furnace margins for rebar are currently thin — only RMB 57/t as of Wednesday, according to Mysteel’s monitoring on the 247 BF mills across the nation, down from a recent high of RMB 81/t two weeks ago — leaving limited room to absorb higher coke costs.

At the same time, coke inventories at mills remain at reasonable levels now, allowing them to maintain essential procurements without urgent restocking pressure. In addition, uncertainty around downstream steel demand has made mills cautious about passing on higher costs. The recent pullback in coke futures has further reinforced mills’ wait-and-see stance.

On the other hand, coke producers were pushing for higher prices, primarily due to cost pressures. Coking coal has seen sustained price increases recently, significantly squeezing their profit margins and pushing some producers into losses.

Meanwhile, demand-side support remains, as steel mills have accelerated blast furnace operations during the traditional peak season. The latest Mysteel survey showed that the 247 BF hot metal output averaged 2.38 mnt/day over 13-19 March, logging a 3.14% rise on week.

Overall, market consensus suggests that the first round of coke price increases is likely to be implemented in the last few days of this month or early April, although the pace has been much slower than initially expected.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply