- GCC output declined due to maintenance and operational adjustments

- Overall output strengthened due to consistent smelter performance

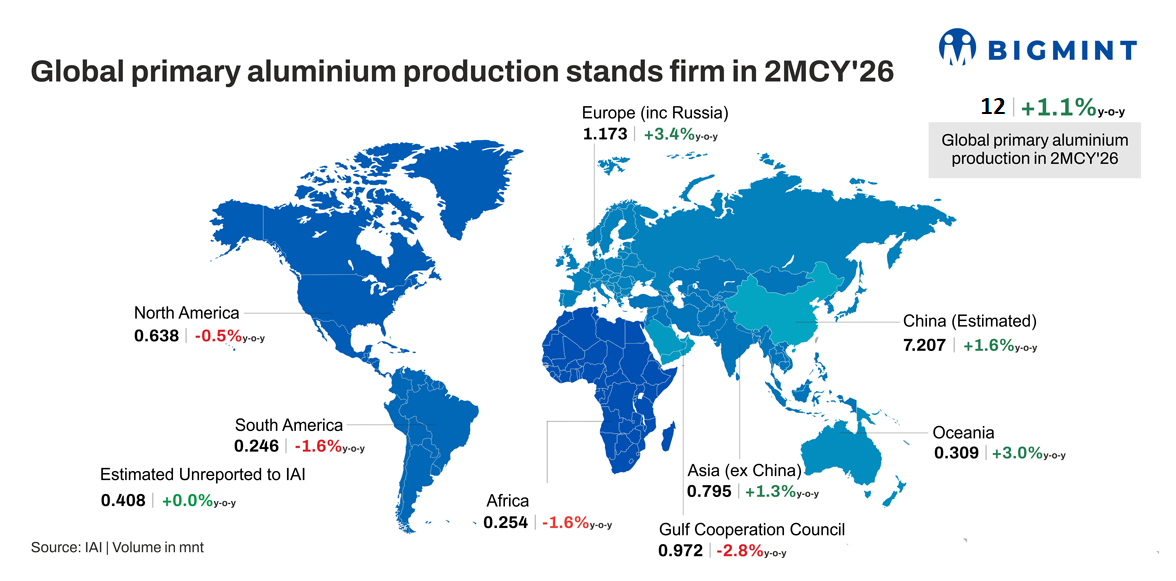

Global primary aluminium production stood at 12 million tonnes in 2MCY’26, marking a 1.1% year-on-year increase from 11.87 million tonnes in 2MCY’25. The modest growth reflects stable operating conditions across major smelting regions, supported by firm market fundamentals. Continued strength in aluminium prices and relatively tight supply dynamics have helped sustain a positive production outlook.

Regional drivers shaping global primary aluminium output in 2MCY’26

Global primary aluminium production in 2MCY’26 exhibited varied regional trends, reflecting a mix of structural challenges and growth drivers across the world.

China, the world’s largest aluminium producer, increased output by 1.6% amid policy-controlled capacity caps around 45 million tonnes. Government support for efficient operations and strong domestic demand have helped maintain steady production, despite a decline in net exports.

In Africa, production declined by 1.6% year-on-year, primarily due to power supply instability and aging smelting infrastructure. According to the International Aluminium Institute, inconsistent electricity availability and higher production costs have constrained growth in African smelters.

North America experienced a marginal decrease of 0.5%, as high electricity and labor costs continue to pressure smelter profitability. The US Geological Survey notes that several North American smelters are operating below capacity amid stiff competition from lower-cost producers abroad.

South America’s output also contracted by 1.6%, mainly because of power shortages and cost inefficiencies, particularly in countries like Brazil and Venezuela where electricity disruptions and aging plants limit capacity utilization.

Conversely, Asia excluding China saw a 1.3% increase in production, driven by capacity expansions in India and Southeast Asia. This growth is supported by improved regulatory environments and access to relatively cheaper energy, with new smelters coming online and existing facilities ramping up output.

Europe, including Russia, posted a strong 3.4% year-on-year growth. This rebound follows partial recovery from previous curtailments related to high energy prices. Several European smelters have resumed or increased production as electricity costs stabilize, while Russia maintains steady output due to integrated supply chains and robust domestic demand.

Oceania’s aluminium production rose by 3.0%, buoyed by stable hydropower-based smelting operations in Australia and New Zealand. These operations benefit from relatively low and consistent energy costs, along with efficiency improvements and steady demand.

In the Gulf Cooperation Council (GCC) region, production declined 2.8%, primarily due to maintenance shutdowns and temporary operational adjustments after a period of strong output. Despite access to low-cost energy, these short-term factors have weighed on production levels.

Finally, the estimated unreported production to the International Aluminium Institute remained unchanged, representing stable output from regions or producers not formally reporting.

Impact of pricing

On a 2MCY basis, LME aluminium prices averaged $3,122/t in 2MCY’26, marking a strong increase from $2,615/t in 2MCY’25. Meanwhile, LME inventories declined by around 18% y-o-y, easing to an average of 490,000 tonnes from 581,700 tonnes over the same period.

In Jan’26, prices were supported by ongoing concerns over tight physical availability and supply constraints, with global reported stocks trending lower as physical premiums, particularly in Asia, remained firm amid strong industrial demand. In Feb’26, Chinese and Asian domestic aluminium markets also saw sustained price support, as limited warehouse stocks and robust demand from manufacturing and energy transition sectors kept inventory draws visible and underpinned LME pricing, helping sustain elevated average price levels and contributing to the year‑on‑year reduction in reported inventory levels.

Moreover, ongoing geopolitical tensions, particularly disruptions in the Middle East affecting key production and shipping routes, have amplified supply concerns, keeping inventories tight and supporting price levels.

Outlook

Global primary aluminium production is likely to experience minor corrections or slower growth in the near term due to significant disruptions in key producing regions. In the Middle East, the ongoing US-Israeli conflict in Iran has led to output curtailments, with Aluminium Bahrain (Alba) halting shipments and shutting down some reduction lines, and Qatalum in Qatar initiating a controlled production shutdown amid gas supply issues. Shipping risks through the Strait of Hormuz further threaten continuity of Gulf output, tightening supply.

Additionally, the Mozal smelter in Mozambique is set to enter care and maintenance from March 2026 due to unresolved power supply issues, removing a significant source of primary aluminium. These closures, combined with the slow restart times typical of energy-intensive smelters, are expected to keep inventories tight, elevate physical premiums, and sustain volatility in global aluminium markets, making minor output corrections likely in the coming months.

Leave a Reply