- Carmakers rush to secure aluminium supplies

- Production risks rise amid energy shortages

The ongoing West Asia conflict has created a significant disruption across the global automotive industry, with aluminium emerging as a key pressure point. Carmakers across Europe, the US, and Japan are rushing to secure supplies, fearing shortages as Gulf production and shipping routes remain unstable. The region accounts for nearly 8% of global refined aluminium supply, with Europe relying on it for about 19% of demand and Japan as much as 25%.

Producers such as Aluminium Bahrain and Emirates Global Aluminium have scaled back output due to energy disruptions and shipping bottlenecks. This has forced automakers and suppliers to build emergency inventories, with some companies relying on existing stocks expected to last only a few months. In extreme cases, firms are exploring alternative sourcing, including Russian aluminium, despite geopolitical sensitivities.

The situation has triggered panic buying, with industry executives warning that shortages could intensify if the conflict continues. Certain specialised aluminium products used in automotive applications, such as alloys for wheels and engine blocks, are already in acute shortage.

Shipping disruptions and rising costs intensify pressure

The disruption of key maritime routes, particularly the Strait of Hormuz, has significantly impacted global trade flows. A large share of aluminium shipments passes through this corridor, and delays have increased freight costs, insurance premiums, and transit times.

Ships are being rerouted via the Cape of Good Hope, extending delivery timelines by several weeks and increasing logistics costs by 20-40%. At the same time, rising natural gas prices have further reduced aluminium production in the Gulf, compounding supply tightness.

On the pricing front, aluminium prices on the LME surged by up to 12% following the conflict, while regional premiums in the US, Europe, and Japan rose even more sharply, reflecting physical scarcity.

India faces a dual challenge of fuel and supply constraints

India is among the most impacted markets, facing both global supply disruptions and domestic fuel shortages. Around 60% of India’s LPG demand is met through imports, with nearly 90% of these imports routed through the Strait of Hormuz, making the country highly vulnerable to disruptions.

In response, the government has prioritised domestic LPG consumption, diverting fuel away from industrial use. This has led to widespread shortages affecting multiple sectors, including automotive manufacturing.

Energy intensive processes such as casting, forging, and paint shops are facing constraints due to limited gas availability. Aluminium extrusion units, which are highly dependent on LPG, have been hit the hardest, with several plants shut and others operating at reduced capacity. Output in this segment has dropped significantly, in some cases by as much as 50%.

The crisis has also disrupted petrochemical supply chains. With crude being diverted toward LPG production, key inputs such as propylene have become scarce. Companies like Andhra Petrochemicals have halted operations after supply cuts, while Tamil Nadu Petroproducts has declared force majeure at its facilities. These disruptions are affecting the availability of essential materials used in automotive components, including plastics, foams, and coatings.

Additionally, Kirloskar Ferrous has halted operations at a moulding line due to LPG shortages, highlighting the broader impact on the supplier ecosystem. The shortage of materials such as polyethylene, synthetic rubber, carbon black, and aluminium scrap is further tightening the supply chain.

Cost pressures push carmakers toward price hikes

Rising input costs across metals such as aluminium, along with increased logistics and energy expenses, are forcing carmakers to pass on costs to consumers. Companies like Tata Motors have announced price increases of around 0.5%, while BMW Group India plans hikes of up to 2%. Other players including Maruti Suzuki, Mercedes-Benz India, and Audi India are also reviewing or implementing price adjustments.

These increases come at a time when commodity prices have already been rising since mid 2025, reaching record highs in early 2026. Materials linked to crude oil, such as plastics and synthetic rubber, have also seen cost increases, adding further pressure on vehicle pricing.

Despite these measures, profitability remains under strain. EBITDA margins for companies using industrial gas could decline by 80-100 basis points, while manufacturing costs may rise by 15-25% due to fuel and logistics pressures.

Exports and supply chains come under strain

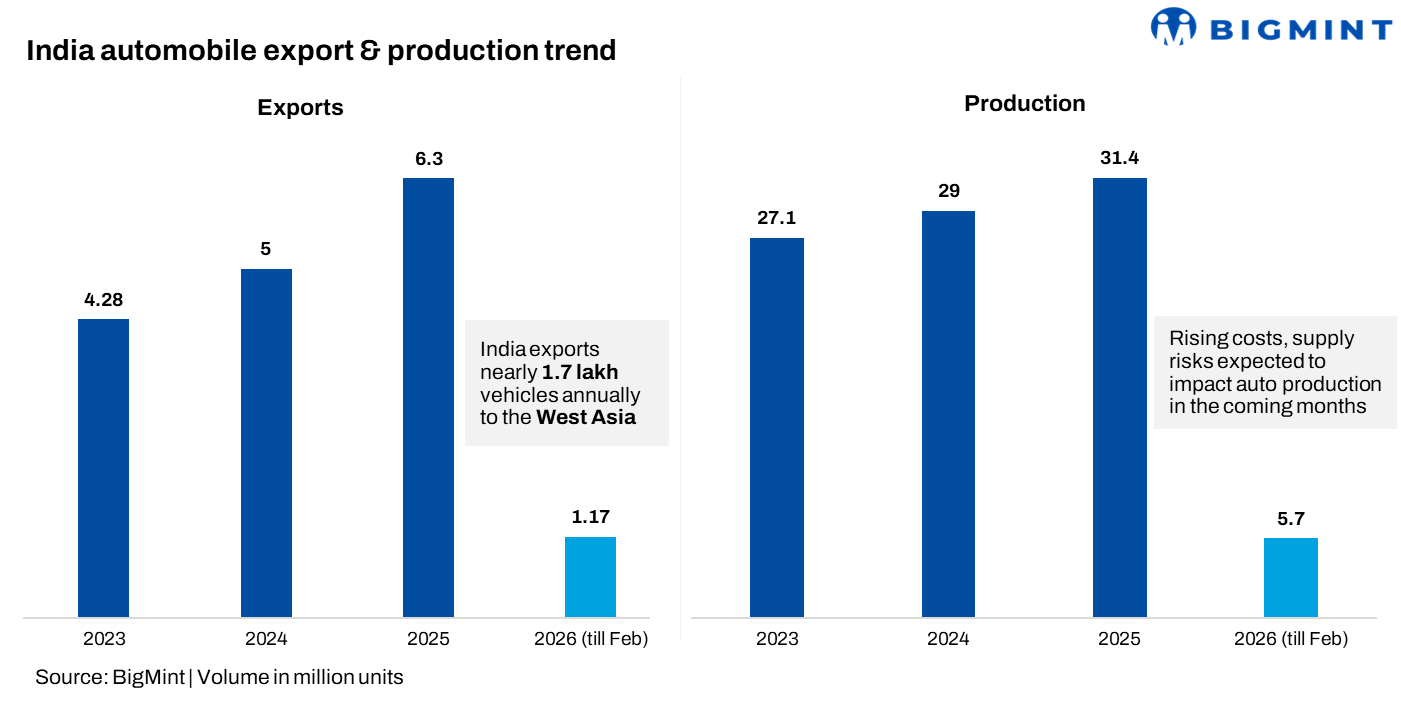

The conflict has also disrupted India’s export momentum. Auto component exports worth nearly 1 billion dollars to West Asia are effectively stalled, while shipments worth close to 7 billion dollars to Europe are facing delays due to rerouted shipping routes.

Transit times, which typically range between 20-25 days via the Suez Canal, have increased significantly as vessels now travel around Africa. This has raised working capital requirements and created delivery uncertainties.

India exports approximately 1.6 to 1.7 lakh vehicles annually to West Asia, volumes that are now at risk due to the ongoing disruptions. Companies such as Nissan, Hyundai, Maruti Suzuki, Honda, and Toyota Kirloskar are expected to be impacted, particularly those with higher export exposure to the region.

Additionally, a recent shipment of Hyundai vehicles to Jebel Ali had to return to India, highlighting the severity of logistics challenges.

Investor concerns and industry outlook

The financial impact is already visible, with the Nifty Auto Index declining by 15.8% year to date. Stocks such as Tata Motors have also come under pressure, reflecting investor concerns over rising costs and potential production disruptions.

Industry stakeholders have begun revising earnings expectations, with estimates suggesting potential cuts of 30-40% for the sector if disruptions persist.

Despite these challenges, some resilience remains. Carmakers with higher localisation levels, such as those highlighted by Skoda Auto India, are relatively insulated in the short term. However, given the global nature of supply chains, prolonged disruptions are likely to affect even the most localised operations.

In the near term, the industry faces a complex mix of rising costs, supply chain disruptions, and geopolitical risks. While demand remains relatively stable, especially during festive periods, sustained pressure on inputs and logistics could impact both production and profitability.

Outlook remains uncertain despite early resilience

Looking ahead, the automotive industry is entering a phase where supply security and resilience will become critical. The West Asia conflict has exposed vulnerabilities not only in energy dependence but also in tightly integrated global supply chains.

For India, the challenge is particularly acute, balancing domestic energy needs with industrial demand while managing disruptions in imports and exports.

Even if tensions ease, recovery is unlikely to be immediate. Production normalization, inventory rebuilding, and supply chain stabilization will take time. In the interim, the market is expected to remain volatile, with intermittent disruptions, elevated costs, and cautious sentiment shaping the outlook for carmakers across the globe.

Leave a Reply