- India: weak sentiment, imports unviable, activity stalled

- Turkiye: prices firm, supported by costs and supply tightness

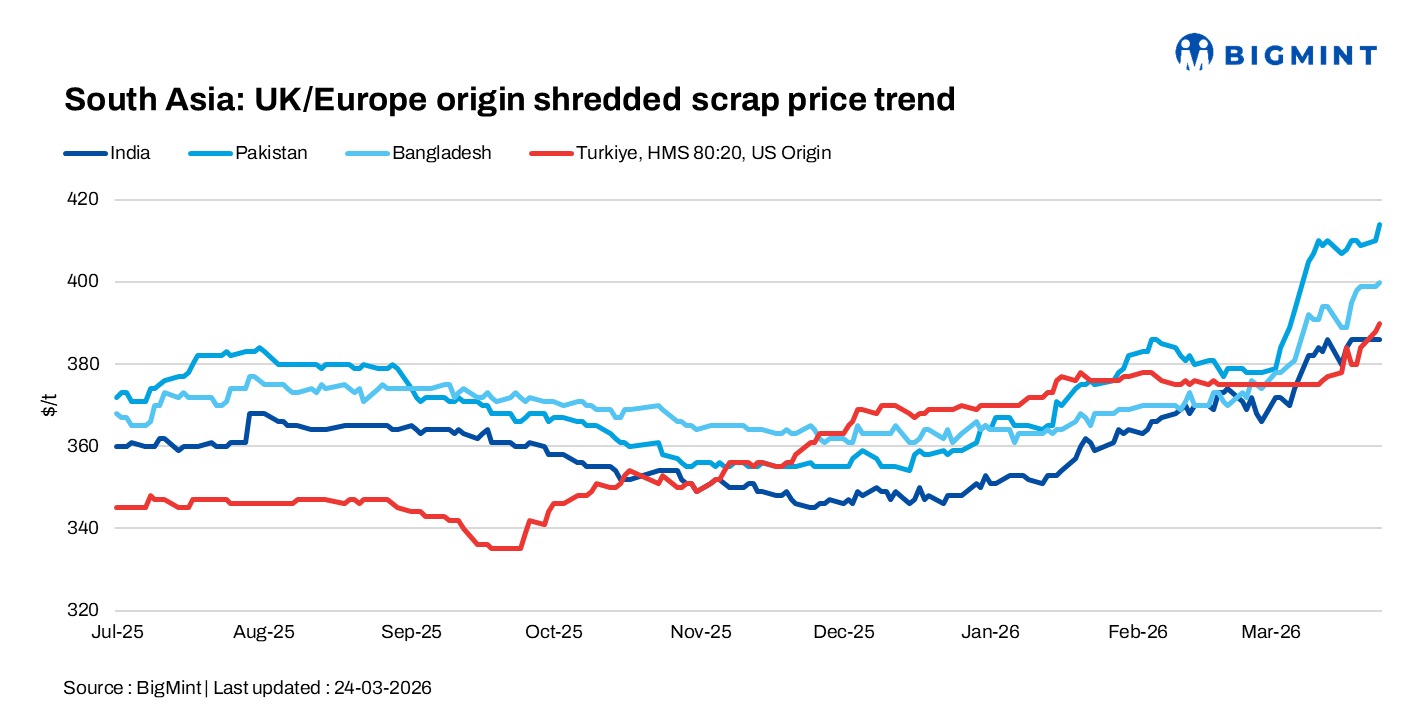

South Asia scrap markets remained weak on 24 March, with India under pressure from currency and demand, while Pakistan and Bangladesh saw limited activity due to holidays and cautious buying. Turkiye stayed firm, supported by higher costs and tight supply.

India: India market has crashed, with sentiment weak amid a struggling rupee and subdued downstream demand, limiting import activity. Higher freight costs have further pressured buying interest, keeping market participation minimal.

Indicative CFR levels (24 Mar) for Oceania-origin scrap stood at $365-370/t for HMS 80:20, $378-380/t for HMS 1, $385-390/t for shredded, and around $400/t for PNS. No firm bids, offers, or trades were reported, with UK-origin prices also aligning at similar levels.

Pakistan: Pakistan market remained largely inactive, with most trading paused due to Eid al-Fitr holidays. Containerized shredded scrap offers were heard at $410-420/t CFR Qasim, but buying interest stayed limited amid market closure.

On the supply side, the UK scrap market remained firm and largely out of reach for traders, with shredded prices around $408/t. Rising dock inventories indicate controlled supply flows, keeping availability tight and offers elevated.

Bangladesh: Bangladesh market remained cautious, with import prices holding firm amid higher offers from Oceania and East Asia. Indicative levels were heard at $380/t for HMS 80:20, $390/t for HMS 1, $400/t for shredded, and $410-415/t for PNS CFR Chattogram. However, no fresh trades from Australia to Bangladesh or India were confirmed.

Buying interest remained selective, with mills evaluating domestic finished steel price trends before committing to higher-priced cargoes. A UK-origin shredded deal was reported at $400/t CFR Chattogram (1,000 t) ahead of Eid, while Bangladesh buyers continued to pay a premium to secure material from alternative origins.

Turkiye: Deep-sea scrap import prices moved up d-o-d on 24 March, supported by rising freight and energy costs. Limited deal activity was reported, but US suppliers were targeting higher levels of $395-400/t CFR, with tradable indications for premium HMS 80:20 heard around $390/t CFR.

Market participants noted that cost pressures, rather than supply-demand fundamentals, are driving the upward trend. However, both buyers and sellers remain cautious amid ongoing uncertainty linked to the Middle East conflict.

Leave a Reply