- Prices decline toward week-end after early gains; stocks continue gradual downtrend

- MCX lead edges higher; SHFE prices recover by week-end

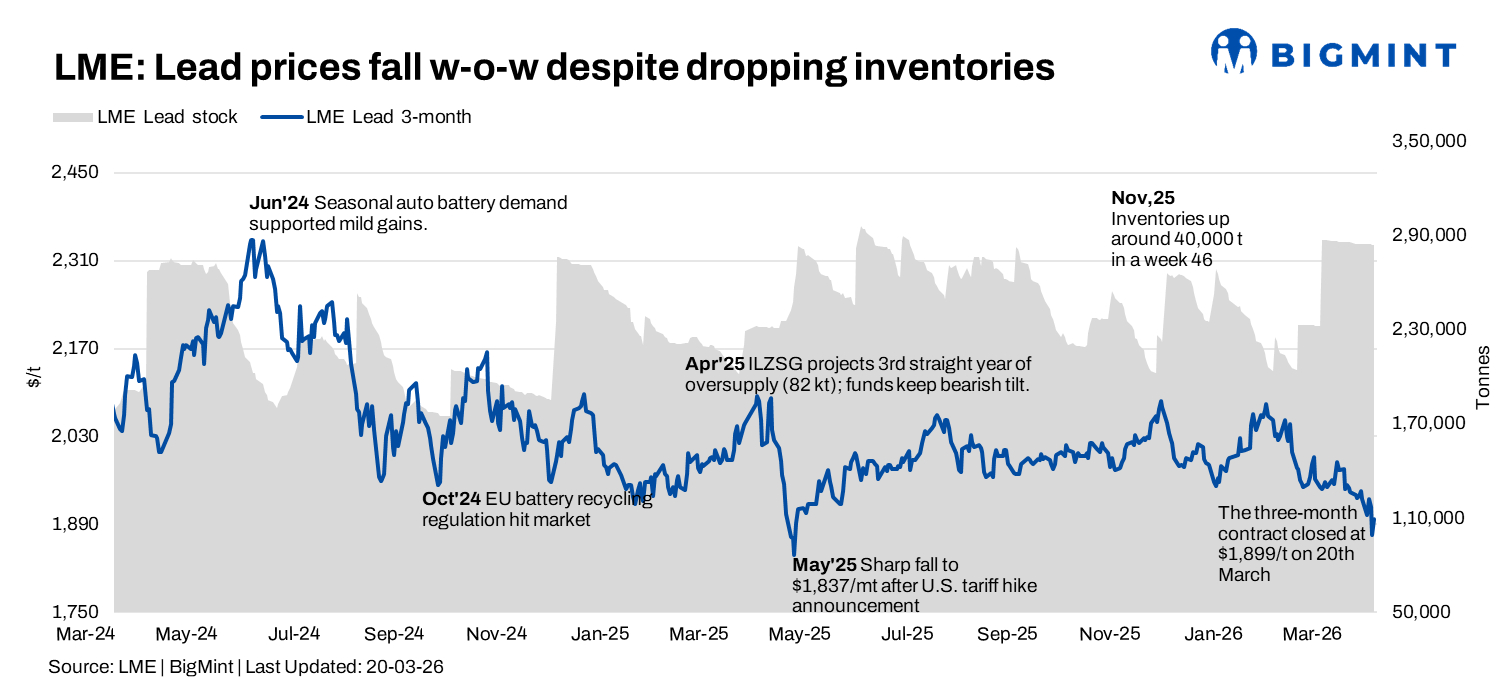

Lead prices on the London Metal Exchange (LME) moved lower in the week ended 20 March 2026, as early-week gains were offset by selling pressure in the latter half of the week. Prices briefly strengthened above the $1,920/t level but slipped sharply mid-week before recovering slightly by Friday, reflecting cautious market sentiment. The three-month contract showed a similar pattern, indicating limited directional momentum amid broadly stable supply conditions.

Price trends

The LME three-month lead contract opened at $1,905/t on 16 March and rose to a weekly high of $1,930/t on 17 March. However, prices failed to sustain gains and declined to a low of $1,873/t on 19 March before recovering to $1,899/t by 20 March.

On a w-o-w basis, prices edged lower by around 1.5%, compared with $1,930.5/t on 13 March, indicating mild downward pressure following last week’s relatively stable trend.

The overall price movement remained within a narrow band, with the inability to hold above the $1,920–1,930/t range signalling continued resistance at higher levels and cautious participation from market players.

Inventory analysis

LME lead inventories remained largely stable during the week, with a slight downward bias. Stocks declined gradually from 284,575 t on 16 March to 284,100 t by 20 March, marking a modest drawdown of 475 t over the week.

The limited movement in inventories suggests that supply-demand conditions remain balanced. While the gradual decline indicates steady consumption, the absence of any significant stock drawdown continues to cap stronger price recovery. Overall, stable inventory levels provided little directional support to the market, reinforcing the range-bound to slightly weaker price trend.

SHFE lead trends

On the Shanghai Futures Exchange (SHFE), lead prices showed mixed movement but recovered toward the end of the week. Prices declined from $2,376/t on 16 March to a low of $2,350/t on 18 March, before rebounding to $2,395/t by 20 March.

The late-week recovery suggests some improvement in Chinese market sentiment, although overall movement remained within a limited range, reflecting cautious demand conditions.

MCX price movements

On the Multi Commodity Exchange (MCX), lead futures traded slightly higher during the week, supported by mild domestic buying interest.

The April 2026 contract opened at INR 189,550/t on 16 March and closed at INR 191,000/t on 20 March, registering a modest w-o-w gain of around 0.7%.

Prices traded within a range of INR 187,250/t to INR 191,500/t during the week. Trading volumes improved toward the latter half of the week, while open interest increased from 14 lots at the start of the week to 109 lots by Friday, indicating fresh participation in the market.

Despite the overall subdued trend, domestic futures remained relatively resilient compared with global prices.

Outlook

Lead prices are expected to remain range-bound between $1,850-$1,950/t in the near term, as stable LME inventories and mixed price trends across exchanges indicate balanced market fundamentals, with no major supply disruptions or demand recovery signals emerging.

In the absence of significant changes in inventory levels or stronger cues from downstream sectors such as batteries, prices are likely to continue trading within the current range, with cautious buying on dips and resistance at higher levels.

Leave a Reply