- Shutdown of units in Morbi reduces Indonesian coal demand

- Higher logistics and ample domestic coal supply limit imports

Indian portside prices of Indonesian-origin thermal coal registered a marginal decline on 20 March 2026 after early firmness during the week, primarily due to subdued industrial demand and cautious buying activity.

According to market participants, demand for Indonesian coal has softened, particularly from key consumption hubs. Nearly 63 units in Morbi have reportedly shut operations amid weak tile demand and rising operational costs, marking a rare instance where traders in the region are facing financial losses.

Additionally, higher logistics and handling charges have increased the overall procurement cost for buyers, leading to resistance in fresh purchases. At the same time, improved availability of domestic coal has encouraged consumers to shift towards local supplies, further reducing reliance on imported Indonesian material.

Portside price movement across key grades

According to assessments by BigMint as of 20 March, prices of 5,000 GAR Indonesian coal remained stable w-o-w at around INR 9,400/t at Kandla Port and INR 9,300/t at Visakhapatnam Port.

Meanwhile, prices of 4,200 GAR coal also remained stable w-o-w to approximately INR 7,700/t at Kandla and INR 7,600/t at Visakhapatnam.

Similarly, lower-grade 3,400 GAR coal prices dropped by around INR 150/t w-o-w to about INR 5,700/t at Navlakhi Port. The slight correction reflects weaker industrial demand and cautious procurement by traders.

Portside thermal coal inventories decline

Portside thermal coal inventories across India recorded a notable decline during the week, largely due to limited fresh cargo arrivals and steady evacuation. Total stocks fell by around 9% w-o-w to approximately 12.15 million tonnes in the week ended 13 March, compared with 13.35 million tonnes in the previous week.

The decline was particularly visible across the west coast, led by ports such as Mundra Port and Kandla, where inventories corrected amid continued inland movement. On the east coast, inventories also declined despite selective stock build-ups at certain ports.

Power plant coal stocks remain comfortable

Coal inventories at Indian thermal power plants witnessed a slight dip but remain largely comfortable. As of 18 March 2026, coal stocks stood at around 57.6 million tonnes, equivalent to roughly 19 days of consumption.

Despite the adequate national stock position, supply concerns persist at certain facilities. Currently, around 21 thermal power plants are operating with critical coal inventory levels. Among these, eleven plants rely on domestic coal supply, seven are designed to use imported coal, and three operate on washery rejects, highlighting uneven coal distribution across the power sector.

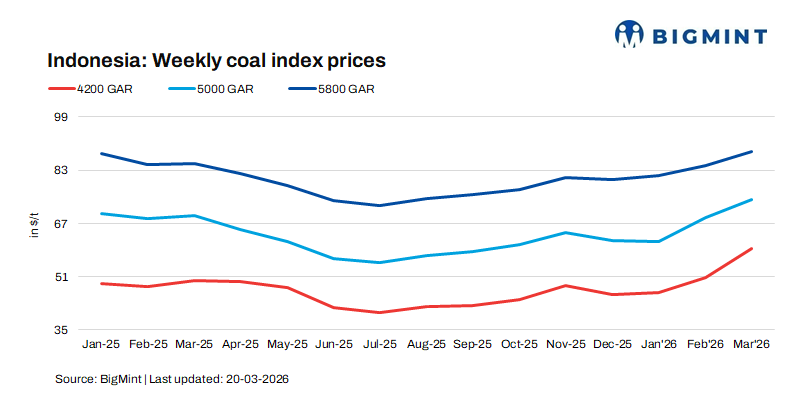

Softer Indonesian benchmarks and freight rates influence import parity

Indonesian benchmark coal prices also declined during the week, exerting mild downward pressure on international market sentiment. Prices of 5,800 GAR coal dropped by around $1.5-2/t w-o-w, while 4,200 GAR coal prices slipped marginally by about $0.1-0.3/t.

In contrast, prices of lower-grade 3,400 GAR coal remained largely stable, indicating relatively balanced demand for lower-calorific-value coal.

Freight rates for shipments to India also softened during the week. According to BigMint’s freight assessment, Supramax vessel freight from East Kalimantan to Navlakhi declined by around $4/t w-o-w to $19.2/t.

However, the depreciation of the Indian rupee – touching around INR 93.7 against the USD partially offset the benefit of lower freight rates, keeping import costs relatively elevated.

Market outlook

Indian portside thermal coal prices may remain under slight pressure due to weak industrial demand. However, lower portside inventories and steady power sector demand may offer some support, while price trends will depend on Indonesian benchmarks and rupee movement.

Leave a Reply